Slippage calculating is not correct when MMmethod is applied to a strategy

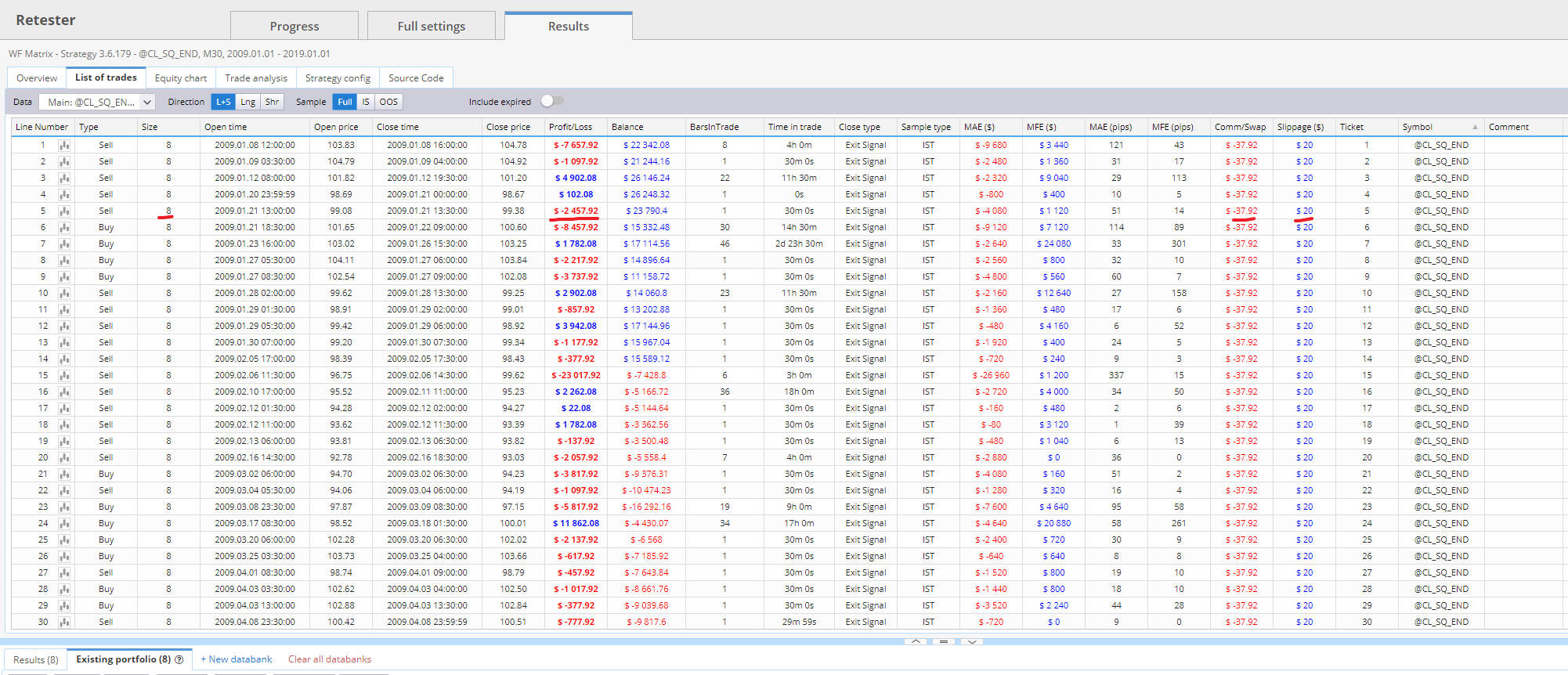

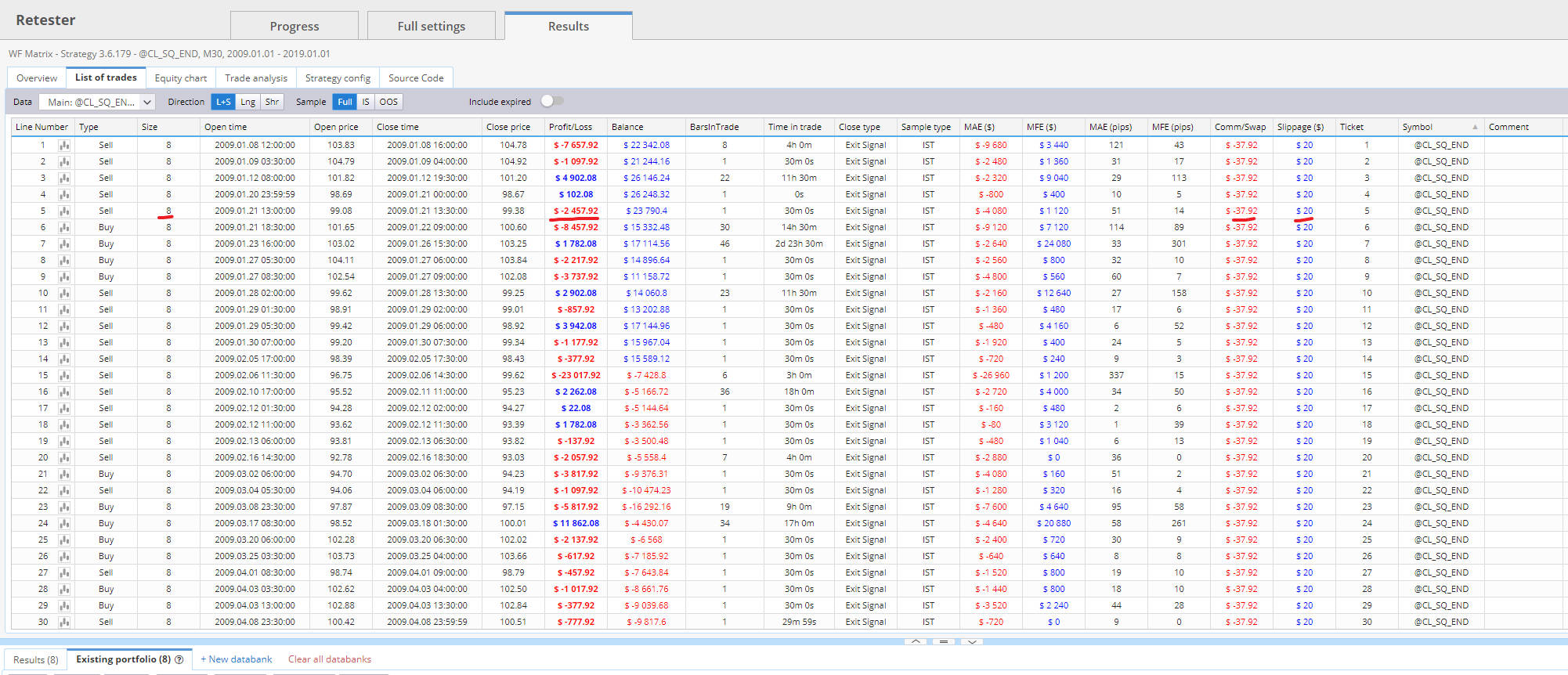

1. As you can see, slippage is obviously calculated based on $ per trade in SQX. But when the strategy is retested with MM method, in most cases, it is not reasonable to spend the same slippage on each trade.

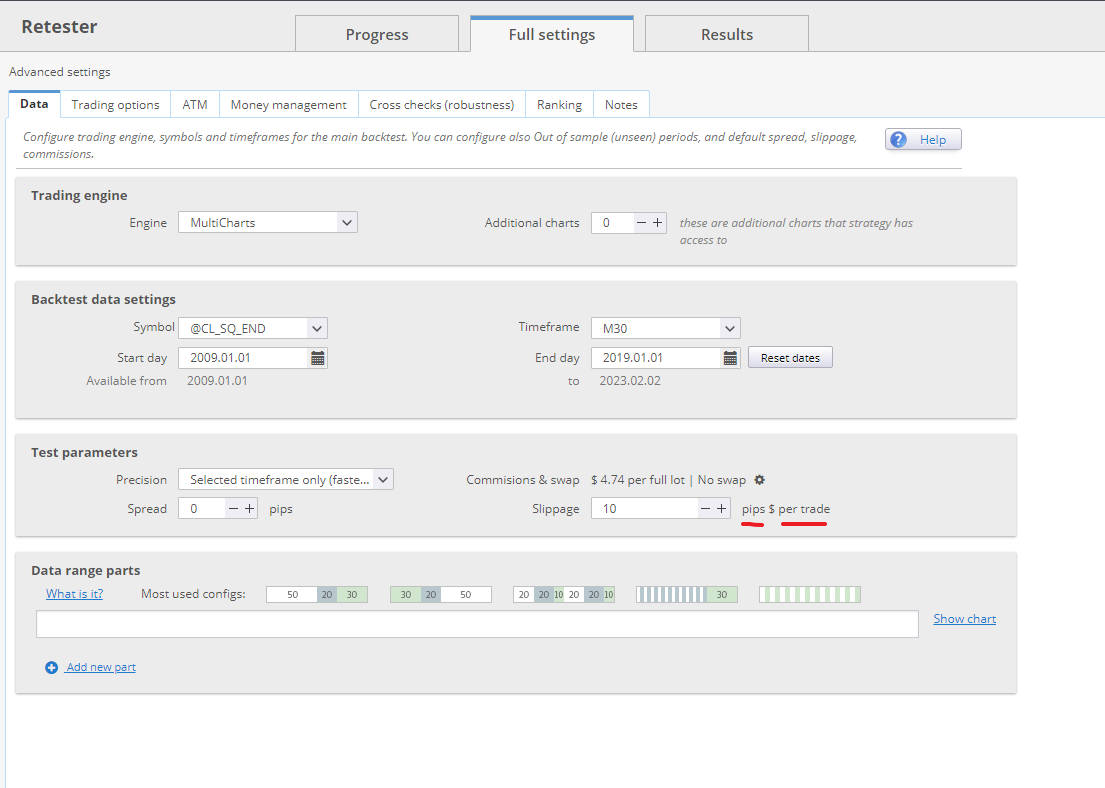

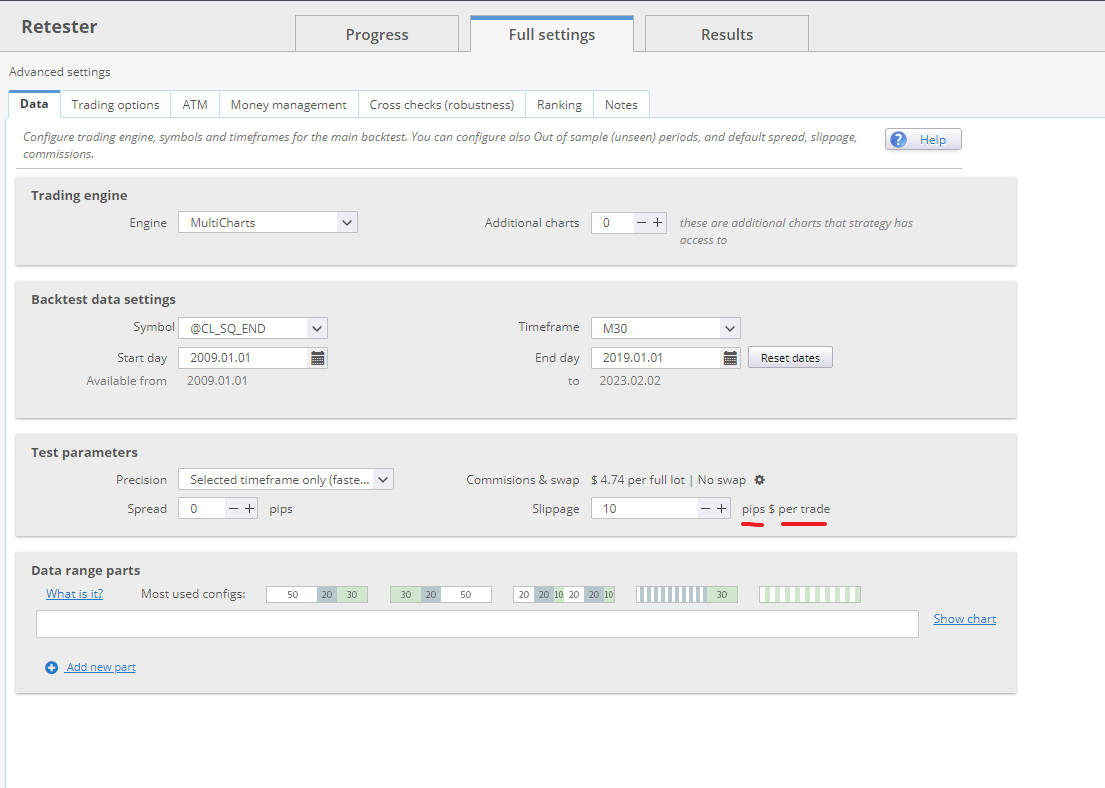

2. There is ambiguity about“pips $ per trade" in Test parameters of data setting.

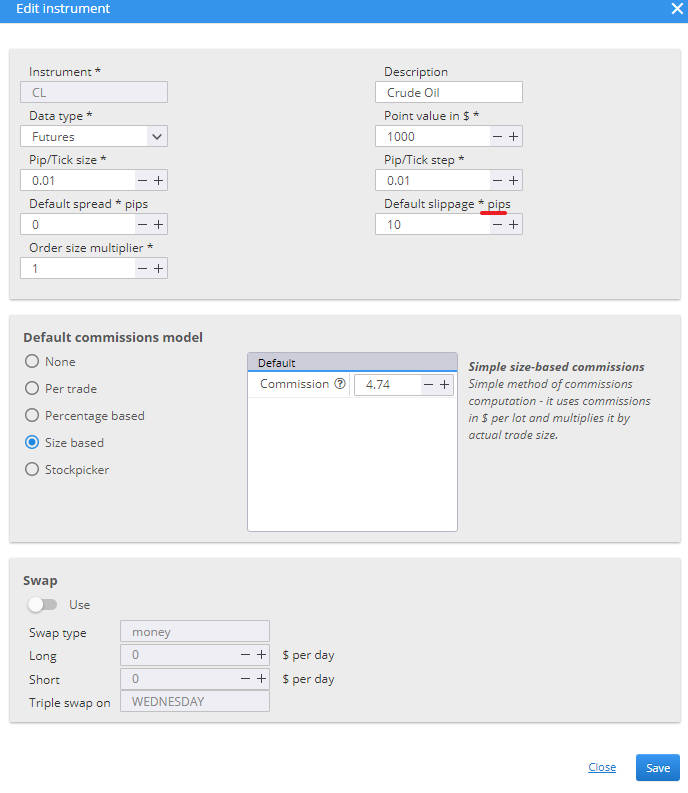

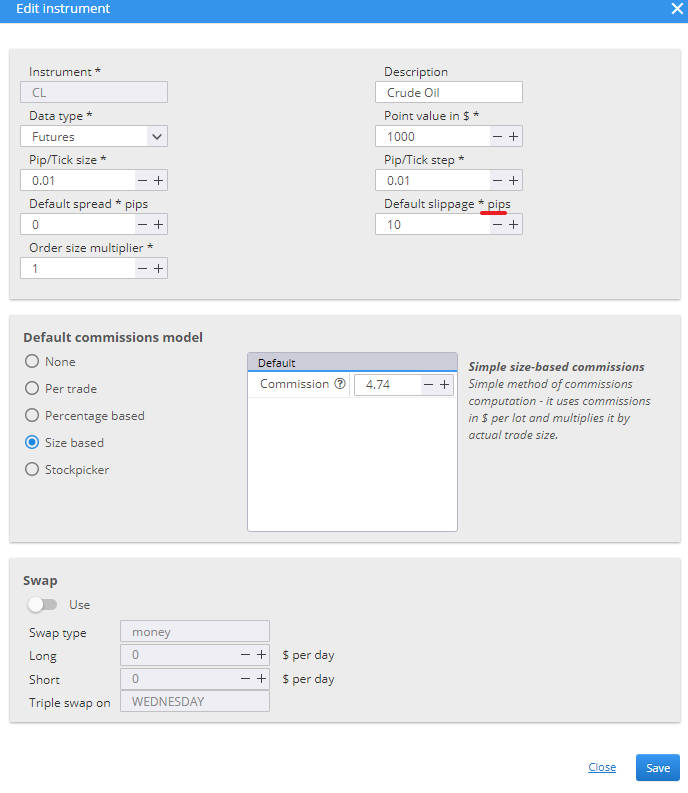

3. default slippage *pips in Datamanager is wrong, in fact it is calulated based on dollar per trade

4. Sometimes, When batch testing is required on different commodities, silppage setting "pips per contract" is more universal.

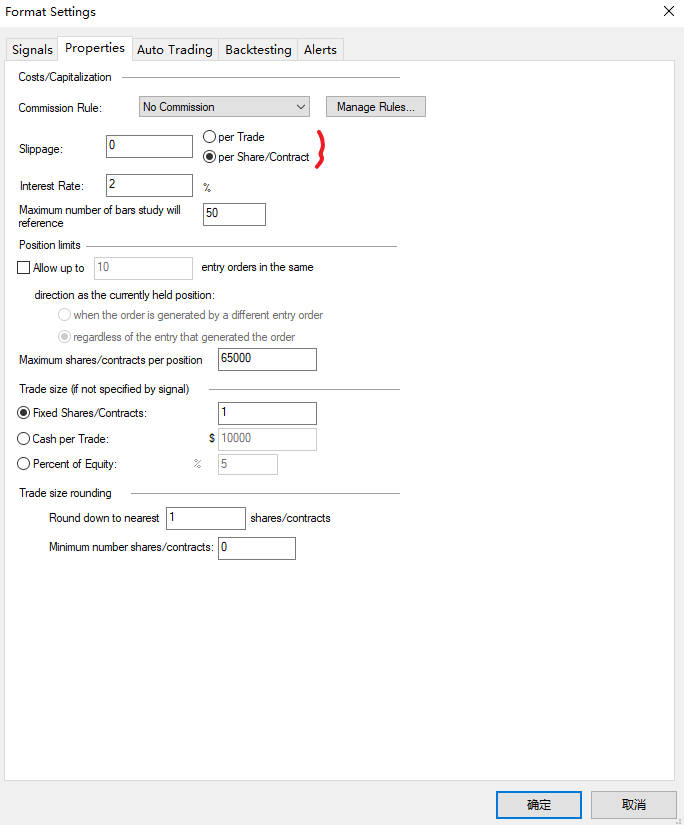

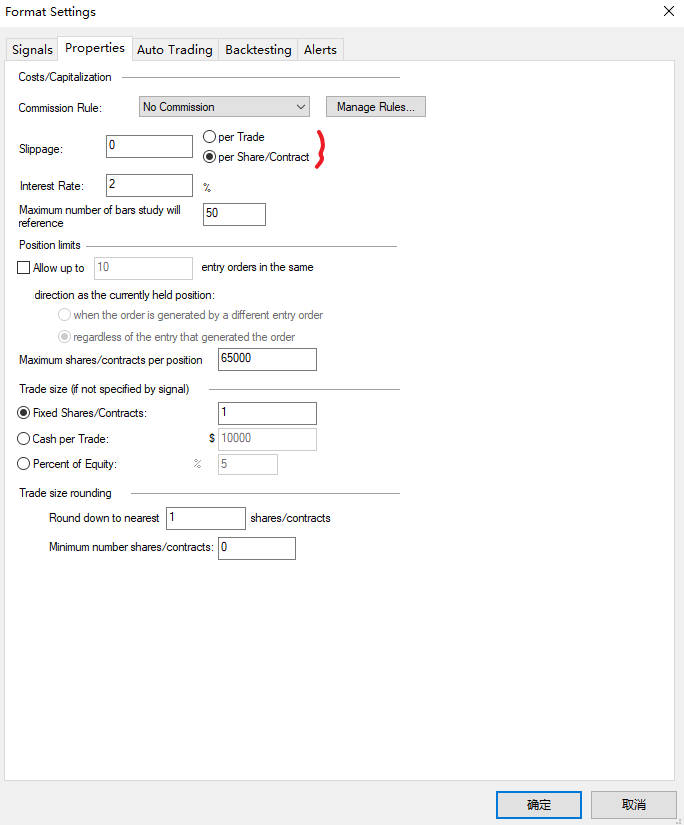

To sum up, it is recommended to support slippage setting option (per trade or per contract, pips per contract or dollar per contract)like Multicharts. Include in defaut slippage setting of Datamanger and slippage setting of Builder,Retester,Optimizer

-

Votes +2

-

Project StrategyQuant X

-

Type Bug

-

Status New

-

Priority Normal

History

binhsir

05.03.2023 05:03Description changed:

1. As you can see, slippage is obviously calculated based on $ per trade in SQX. But when the strategy is retested with MM method, in most cases, it is not reasonable to spend the same slippage on each trade.

2. There is ambiguity about“pips $ per trade" in Test parameters of data setting.

3. default slippage *pips in Datamanager is wrong, in fact it is calulated based on dollar per trade

4. Sometimes, When batch testing is required on different commodities, silppage setting "pips per contract" is more universal.

To sum up, it is recommended to support slippage setting option (per trade or per contract, pips per contract or dollar per contract)like Multicharts. Include in defaut slippage setting of Datamanger and slippage setting of Builder,Retester,Optimizer

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}