AW sqx137: Strategy template, Random Action Errors

Under AlgoWizard page of StrategyQuant in Linux, I am trying to create a Strategy Template with Long/Short symmetry.

- In the LONG ENTRY tab, I uncheck the last option "Allow Duplicate Trades" but it checks it back if I switch to SHORT ENTRY tab. Similarly, if I uncheck that option under SHORT ENTRY tab and switch to LONG ENTRY tab, it checks the option itself. Therefore, there is no way to really uncheck this option for LONG ENTRY and SHORT ENTRY

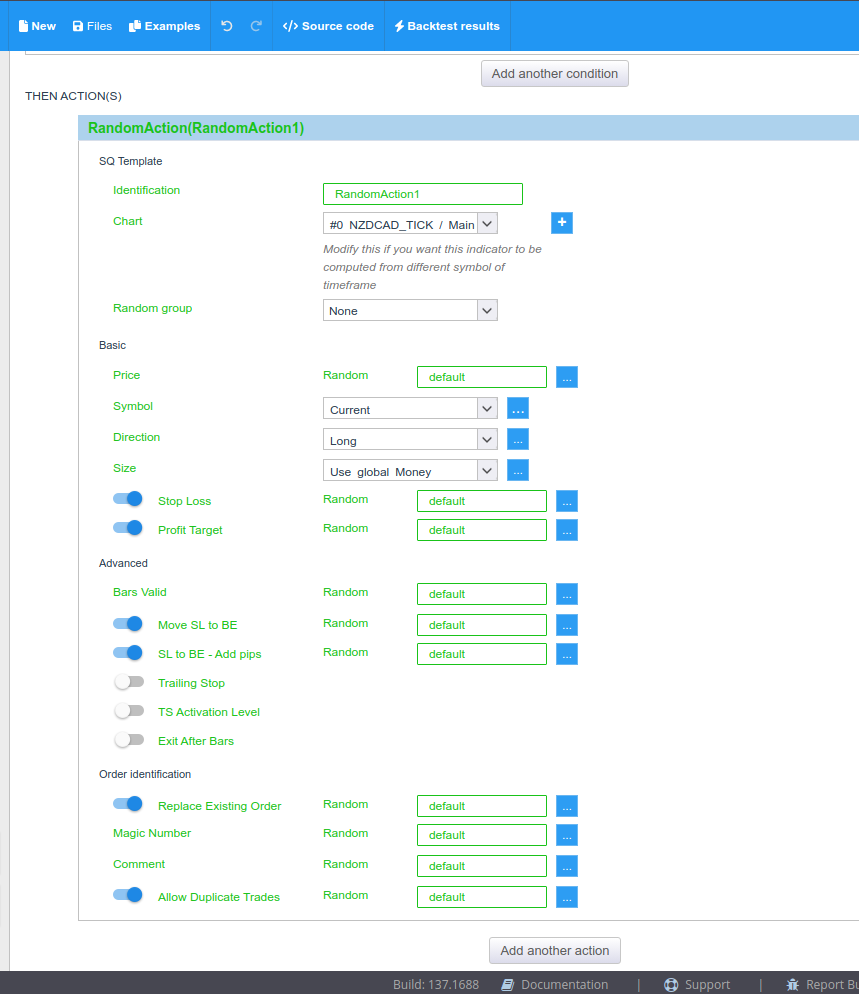

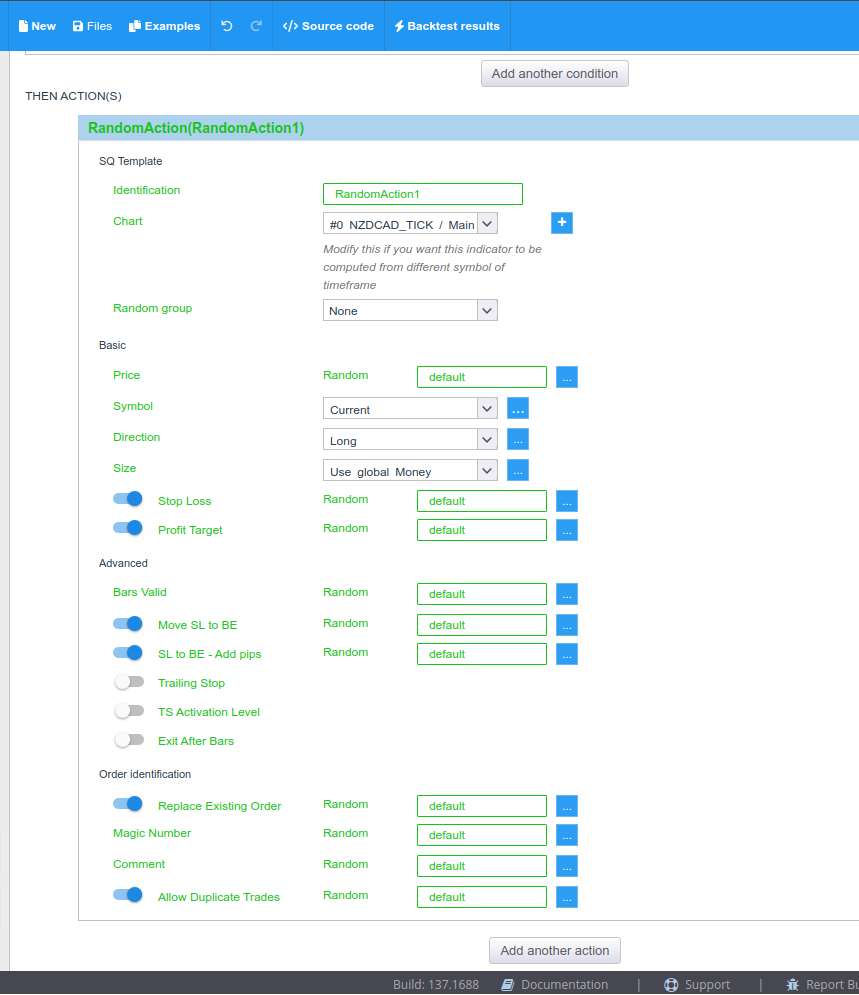

- If I try to Build strategies using the final Strategy template, it aborts with errors shown below. Eventhough I set "Symbol" correctly to "Current" in AlgoWizard page.

com.strategyquant.datalib.TradingException: Instrument info for symbol 'RandomAction1 doens't exist com.strategyquant.datalib.TradingException: java.lang.NullPointerException: Cannot read field "tickSize" because "<local8>" is null

Please see attached screenshot and the final Strategy template. To recreate the above errors, try to Build strategies for AUDUSD (Dukascopy data in GMT time zone) on Hourly bars using this Strategy template.

-

Votes +2

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

m

m

E

TT

Tamas

05.10.2023 10:20Subject changed from Linux 137rc4: Strategy template Errors to AW sqx137: Strategy template, Random Action Errors

VK

Votes: +2

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}