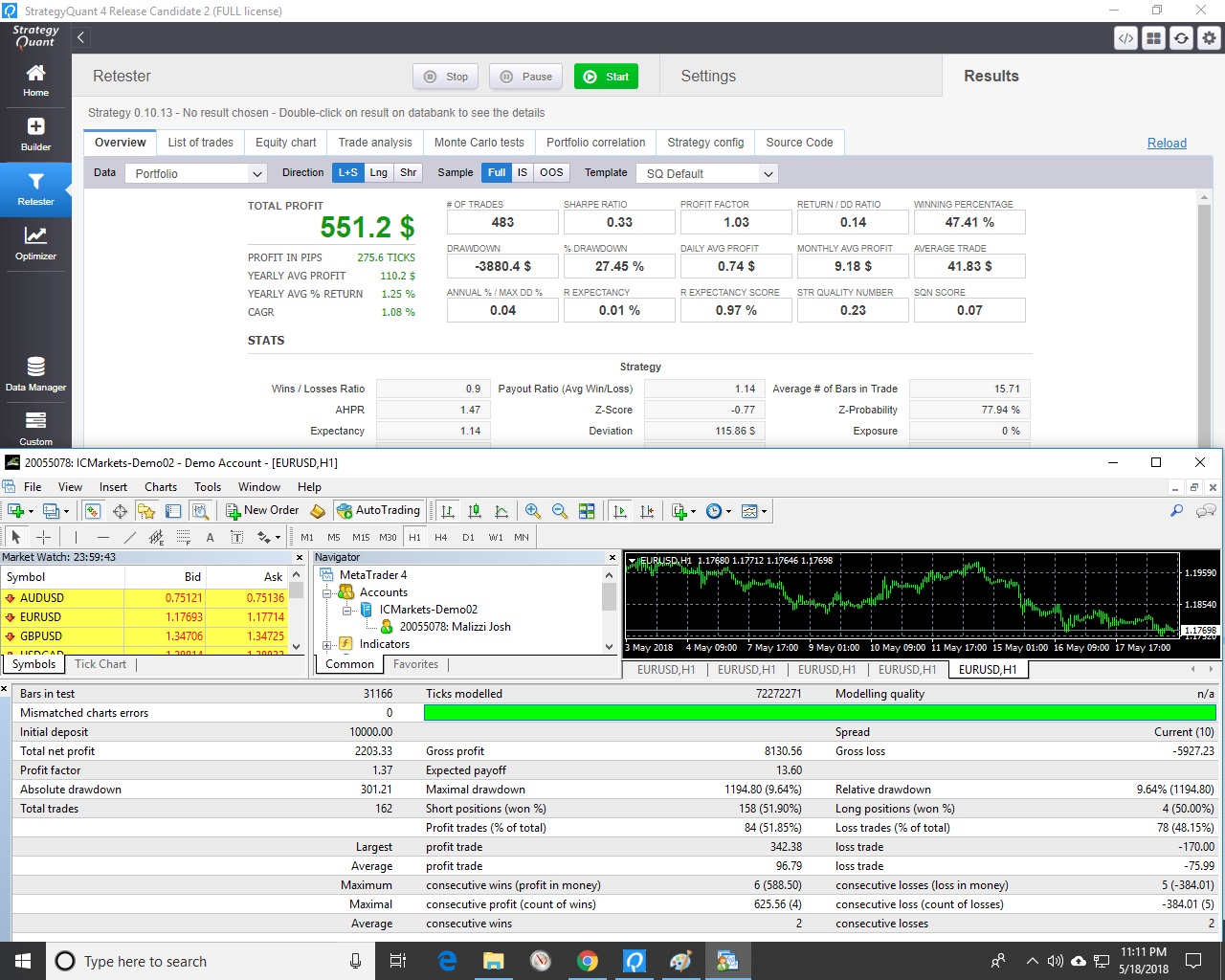

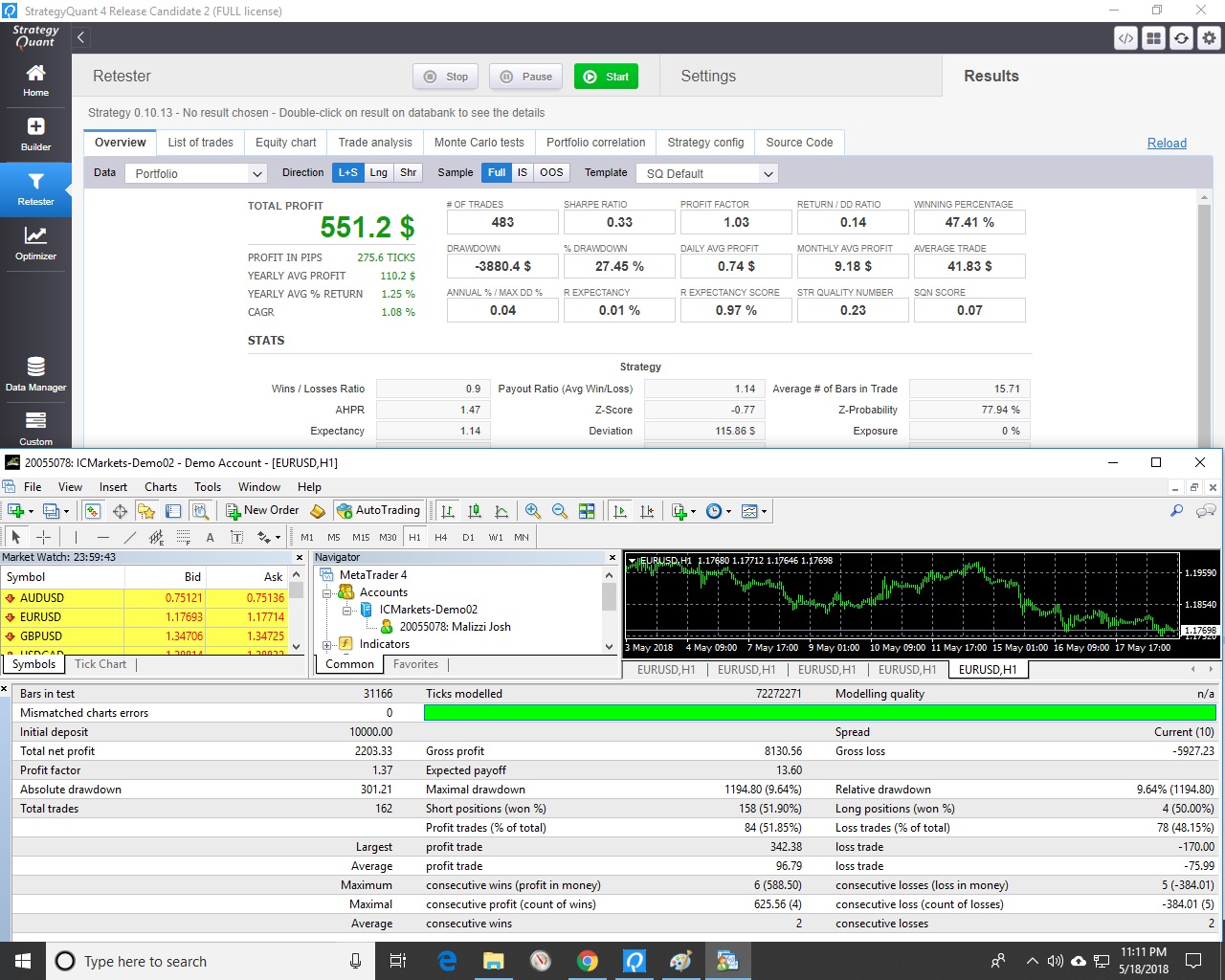

very different results between SQ and MT4

Mark - i see some very different results between SQ and MT4. This is a single time frame strategy. Take a look at the attached image which shows SQ and MT4.

I also attached the file.

SQ = 483 trades. MT4 = 162 trades.

Profit is very different.

Profit factor is very different.

-

Votes 0

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

Votes: 0

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

I tested the attached strategy and the results between SQ and MT4 were matching.

It is true that this strategy works on a single chart, but some conditions contain daily values. Moreover, they use a huge shift - please see the attached screenshot.

If you perform backtest on your own data in MT4, you must also import D1 timeframe values. Otherwise the daily values will be computed as 0, because MT4 is not able to compute higher timeframes automatically. At first I didn't realize that and I had very few trades in MT4.

Concerning the huge shift, please check if you have enough history data available before the start date of the test.