Risk-Reward(SL vs PT) ratio can not restrain RR

I want to generate some strategy with Risk-Reward ratio from 1:2 to 1:3 (SL:PT).

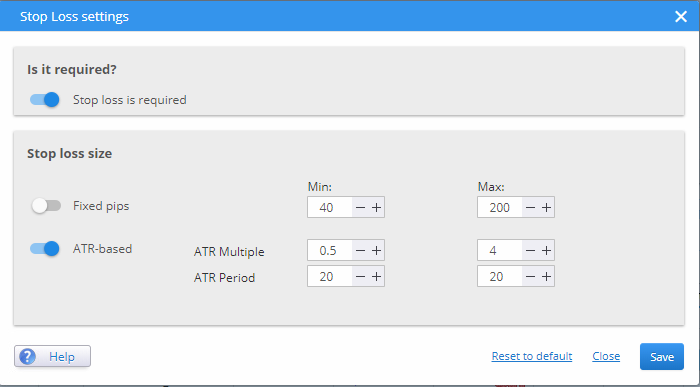

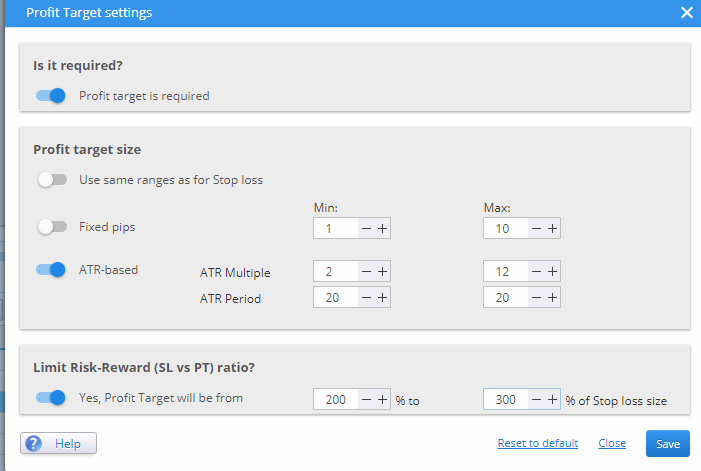

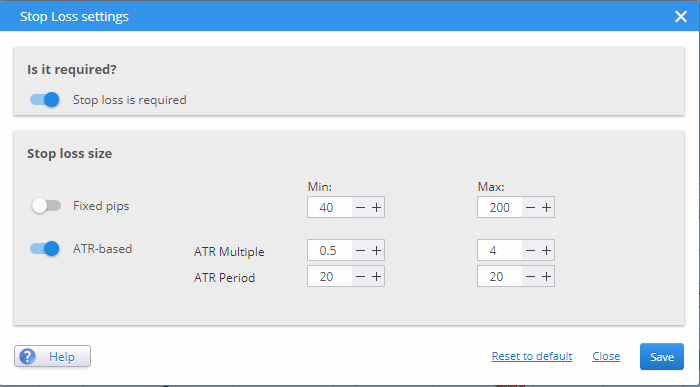

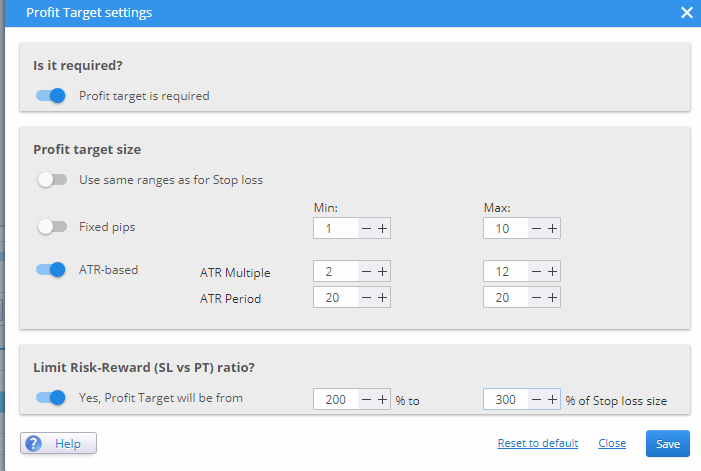

The sl and pt setting as below.

SL: based on ATR, atr multiple[0.5,4], atr period fixed number 20;

PT: based on ATR, multiple[2,12], atr period fixed number 20;

Limit Risk-Reward(SL vs PT) ratios is yes, 200,300.

But SQ X generate strategy with the RR ratio out the setting range. Some strategy's RR are like these:

SL, PT

1.3, 5.5

1.3, 12

I try to cancel the profit target size setting, keep the pt required and RR ratio set yet. Because when I give the SL range, and SL vs PT ratio range, the PT size does not need to be set again or directly. After that, strategy are generated more quickly, but without PT setting.

PT/SL is the key setting. most of trend following strategy have high PT:SL value, and short term swing strategy have narrow PT:SL ratio. It can filter the strategy or give some guide to the strategy style.

-

Votes +2

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

eastpeace

23.02.2019 02:56Description changed:

I want to generate some strategy with Risk-Reward ratio from 1:2 to 1:3 (SL:PT).

The sl and pt setting as below.

SL: based on ATR, atr multiple[0.5,4], atr period fixed number 20;

PT: based on ATR, multiple[2,12], atr period fixed number 20;

Limit Risk-Reward(SL vs PT) ratios is yes, 200,300.

But SQ X generate strategy with the RR ratio out the setting range. Some strategy's RR are like these:

SL, PT

1.3, 5.5

1.3, 12

I try to cancel the profit target size setting, keep the pt required and RR ratio set yet. Because when I give the SL range, and SL vs PT ratio range, the PT size does not need to be set again or directly. After that, strategy are generated more quickly, but without PT setting.

PT/SL is the key setting. most of trend following strategy have high PT:SL value, and short term swing strategy have narrow PT:SL ratio. It can filter the strategy or give some guide to the strategy style.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}