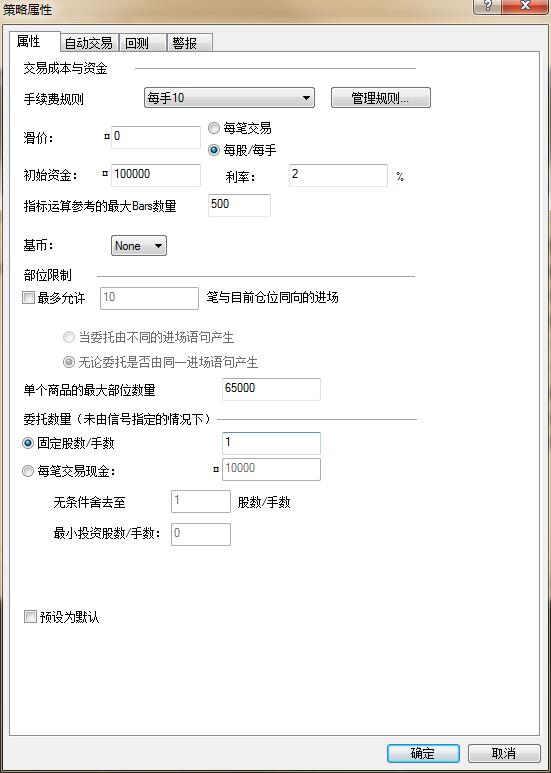

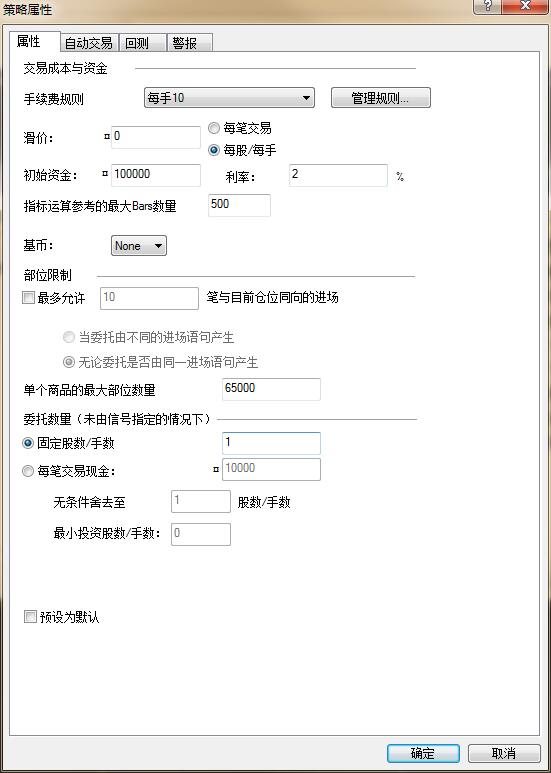

Some performance differences exist between MC and sq test reports

At the beginning of each test trade list, there will always be some differences, which have little impact on the overall performance. I regard these differences as normal and have not been considered.

However, after excluding some differences in the initial stage of the trade list, there are still some obvious bugs that lead to performance differences between MC and SQX.

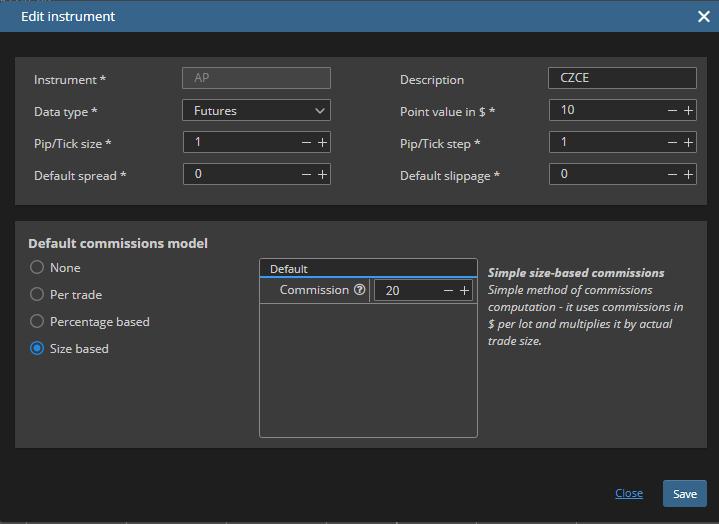

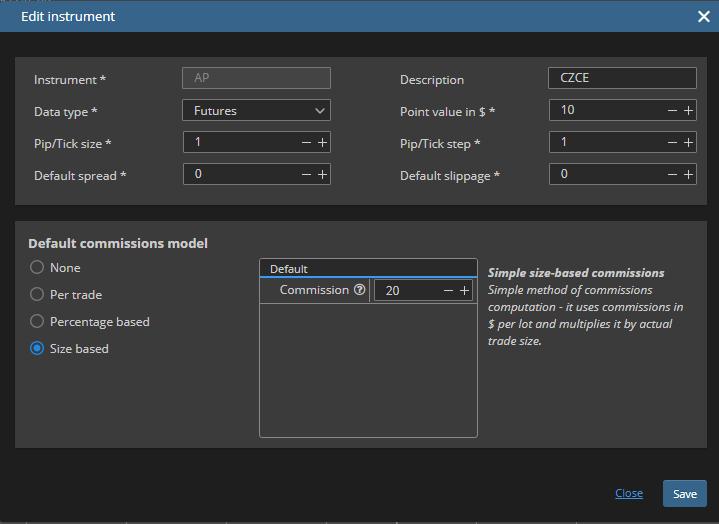

In order to find out the problem of blocks, we simplified the setting of some trade order. We only used the market order, not the stop and limit order. If we add these two orders, according to our previous test, there may be some other bugs.

In many tests, the problem is that the order is open at 9:01. MC adopts the open price of 9:01 in the historical data, but the trade price of SQ is not the opening price of 9:01. We don't find out what the price is, and sometimes the trade price shown in the SQ trade list will even exceed the range of the highest and lowest price of the current K line At a price that doesn't exist.

Sometimes trade in the morning last K line close price will also appear similar situation.

What I've just said is just two bugs that often recur, and there will be others.

I have listed five examples in the attachment. Each of them has a . sqx and a performance report of my Chinese version of MC. Because the Chinese version of MC does not support English display, I don't know whether your company's technical personnel can understand the Chinese report. If there is a problem that needs to be solved by me, the technician can send me an email directly.48566908@qq.com

-

Votes +1

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

4

TB

4

Jordan

11.12.2020 14:46

OK, thank you very much. I hope the MC engine of sqx can be more and more perfect.If the second problem you mentioned is solved, has it been fixed in version 130?

TB

Tomas Brynda

11.12.2020 15:02

Yes, we are making a new build because of that.

The final release of 130 will be available in the beginning of the next week

4

4

Votes: +1

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

thank you for reporting this.

I've made various backtests today and found out there were two problems:

We will try to investigate the exact way MC calculates indicators in the reserved bars area and hopefully solve the differences in the beginning of the backtest results.

For now try to set the reserved bars to a number equivalent to the highest period used in a strategy, it should help.

Best regards,

Tomas