SQX 130 Dev 2 and Jforex mismatch

Strategies attached.

Please check and fix.

Thanks

-

Votes +1

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

GRoundofInferno

02.12.2020 15:22Attachment JforexSQX07926.sqa added

Attachment Strategy 0792671 - Optimization 028914.sqx added

Attachment Strategy_0_792671_Optimization_0_28_914_02122020_122330.html added

1) I've downloaded and install patch to SQX 130 dev2

2) Yes, I've used QA to compare backtest. Merged sqa file attached. As well as sqx and HTML files of both backtests.

3)You can find Jforex backtest settings here in a short video https://www.screencast.com/t/ZMAsUSh9

4) I use both dukascopy data from Jforex and SQX as Duksacopy is my broker.

still something wrong

Tamas

03.12.2020 10:20Then the backtests almost match but there are still some differences. I will dig deeper .... and let you know.

GRoundofInferno

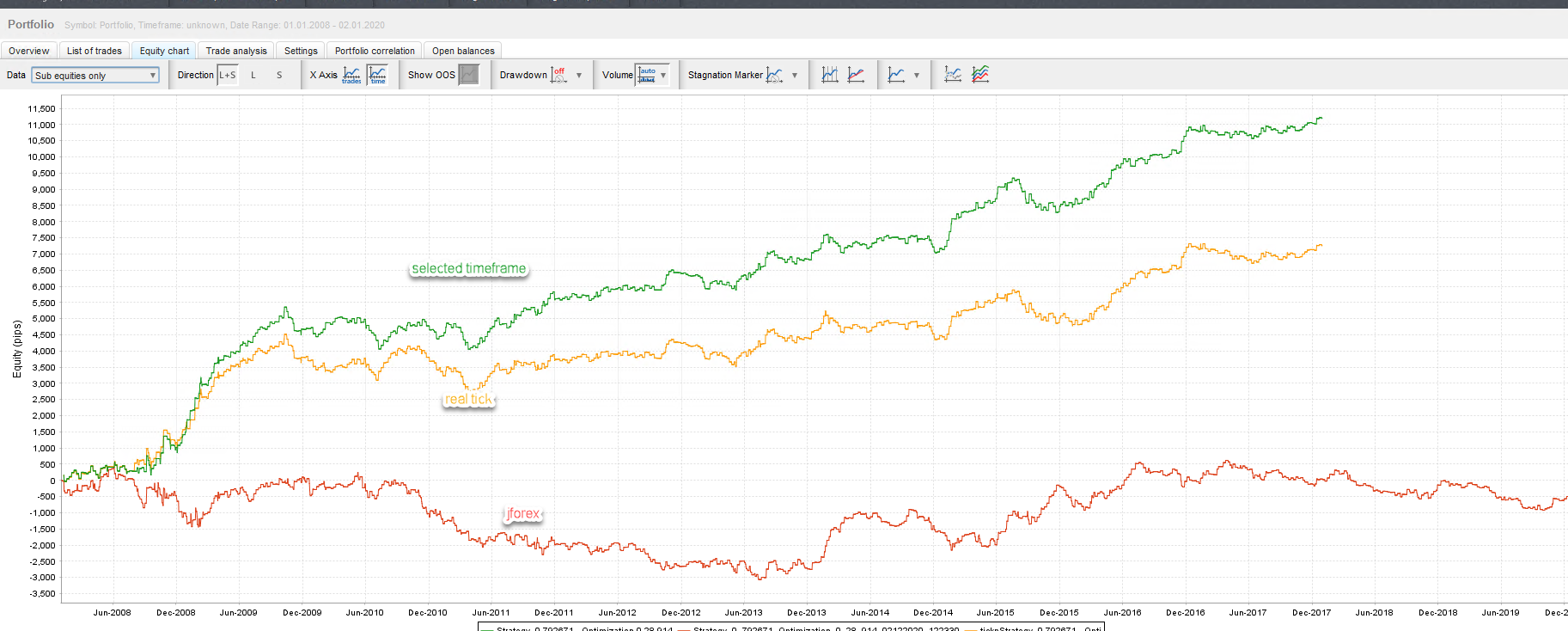

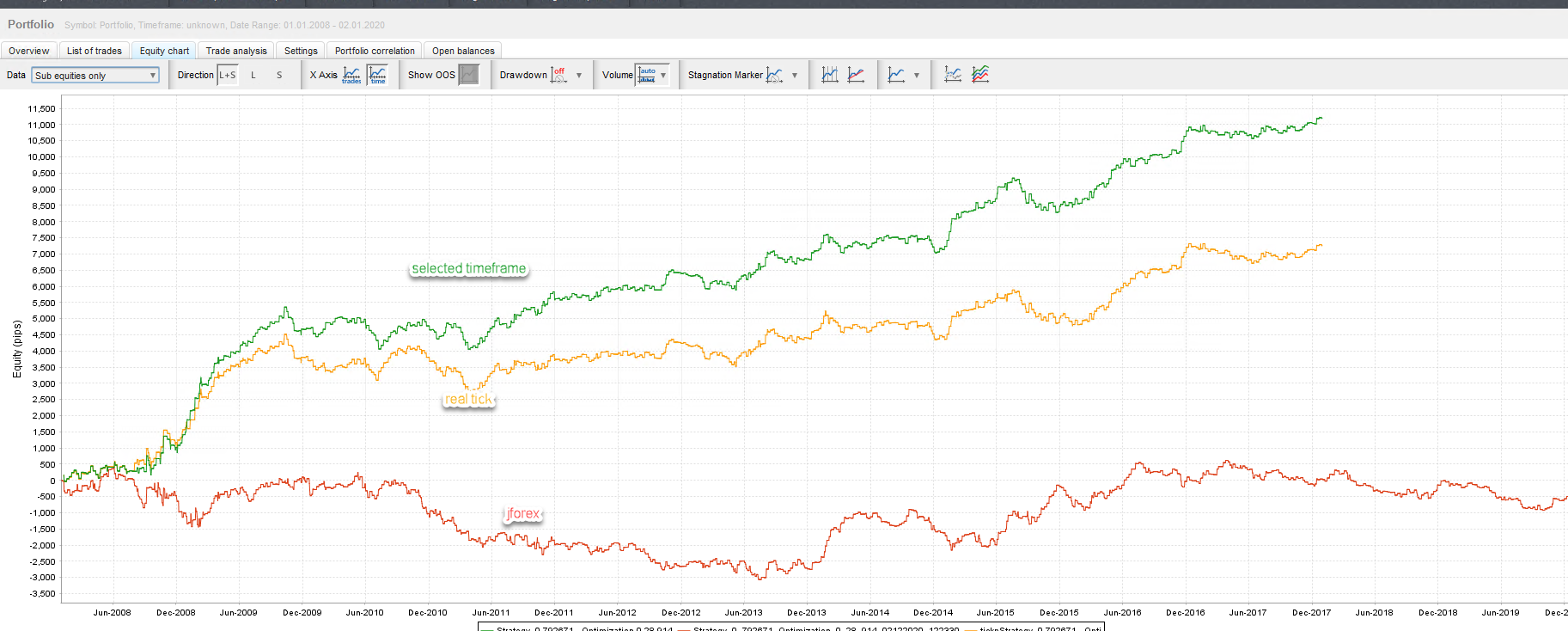

03.12.2020 12:02Attachment image-0.png added

Attachment tickpStrategy 0792671 - Opti.sqx added

my bad I've missed precision settings but....

I can not say that jforex matches sqx with Real tick. Moreover, I can say that difference between selected timeframe and real tick is not substantial BUT...

If we compare with Jforex it is.

I've attached screenshot with selected timeframe sqx, real tick sqx and jforex here.

For your convenience, I've also added tick precise sqx file.

Tamas

20.05.2021 13:29Status changed from New to Fixed

There can be still some differences in backtests. Please read post here https://strategyquant.com/doc/strategyquant/reliable-backtesting-in-jforex/

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

Please download the patch from the task below and test it out

https://roadmap.strategyquant.com/tasks/sq4_7357

Are you using QuantAnalyzer for comparing the backtests ?

If yes, can you please also attach a portfolio sqa (merged html jforex + sqx) file next time ?

Additionally can you provide more info about the backtest settings in JForex ? Would be great to have a printscreen of History Tester tab

Did you export historical data from jforex to SQX to get the same result?