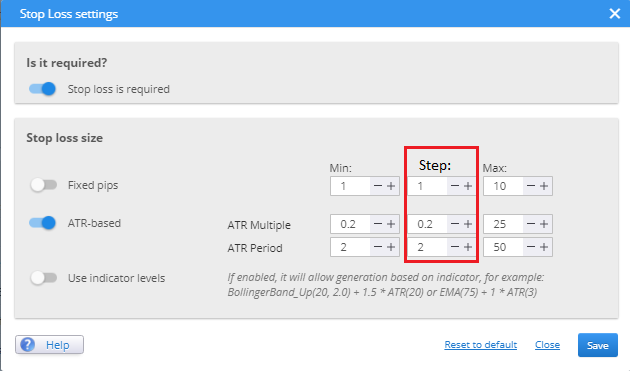

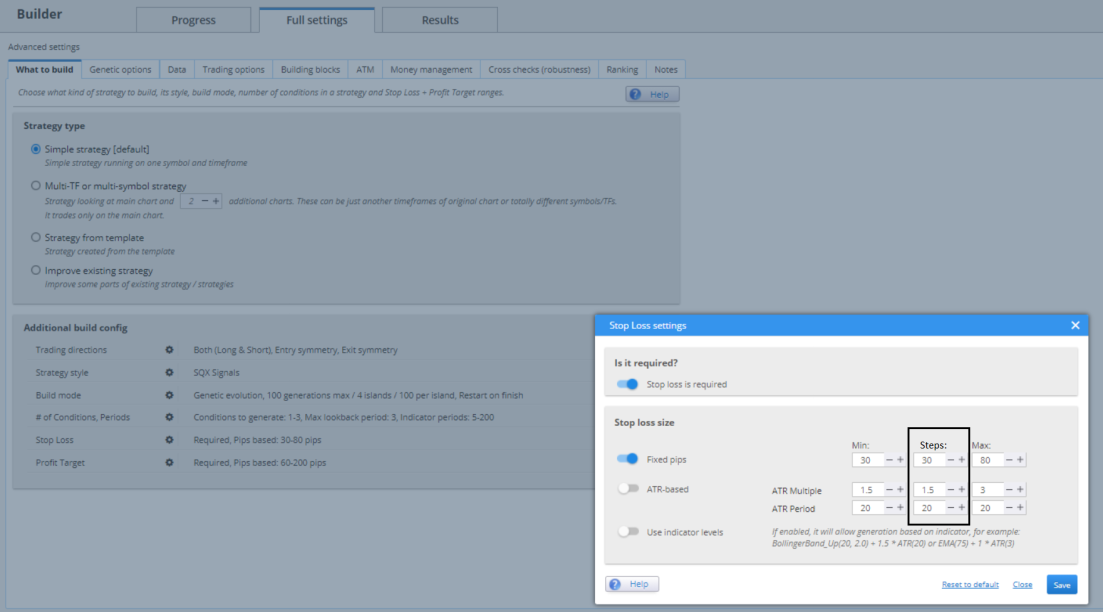

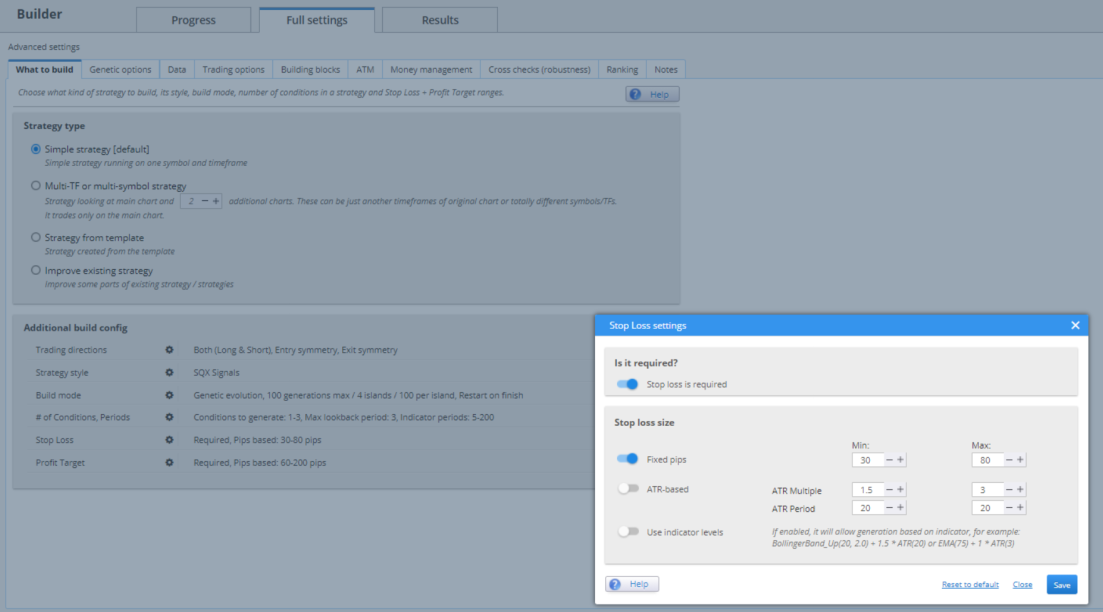

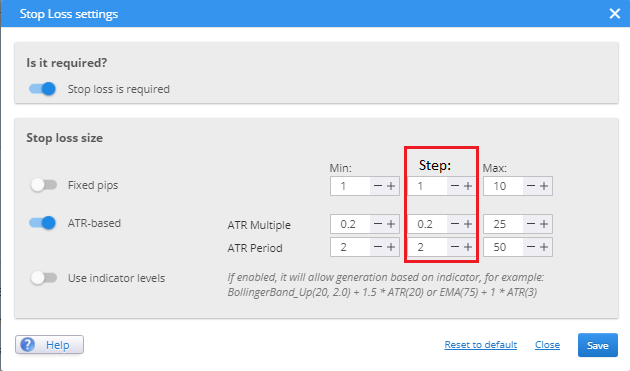

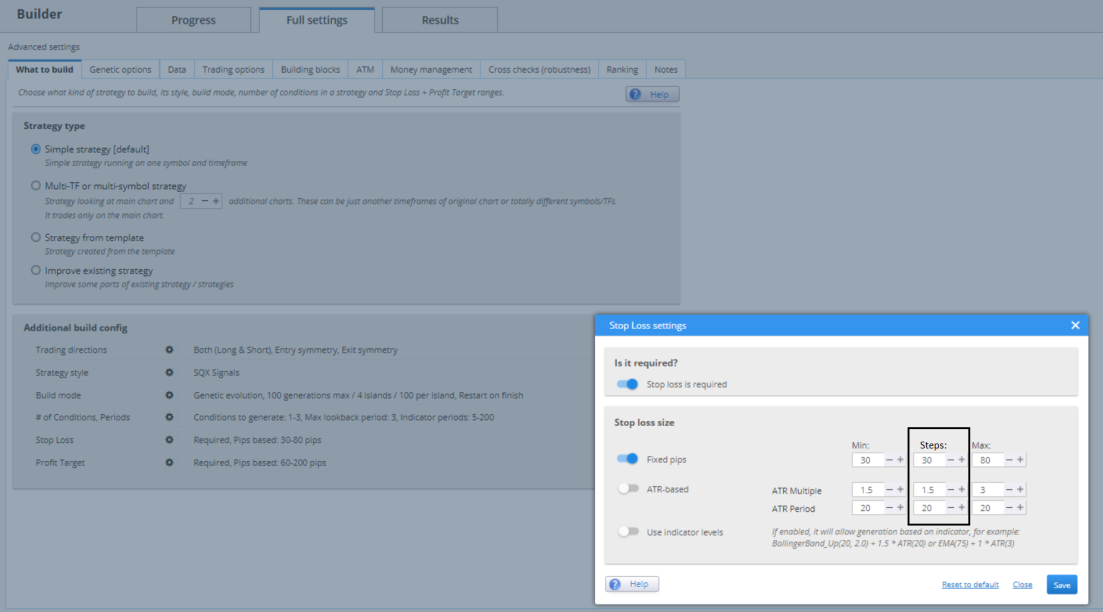

SL/TP Pips+ATR Steps parameters (Screenshot attached)

-

Votes +18

-

Project StrategyQuant X

-

Type Feature

-

Status New

-

Priority Normal

History

k

b

k

JH

MO

L

m

JK

DR

MF

g

b

l

k

Karish

19.03.2021 19:18

Re uploaded the screenshots for more accurate view of the feature request.

NS

b

bentra

06.01.2022 22:58

One example of why it's a good idea:

When searching for an h4 strategy we would want the steps of the period for the ATR reading to be 6 so that it is stepping in whole days (6x4=24) and not wind up having a period with fractions of a day. It's ideal to do this to avoid intraday fluctuations affecting the sample for ATR.

EDIT: applies to forex and other 24hour markets of course. If you trade a market with 5 h4 bars per trading day then you'd want your step to be 5 :)

When searching for an h4 strategy we would want the steps of the period for the ATR reading to be 6 so that it is stepping in whole days (6x4=24) and not wind up having a period with fractions of a day. It's ideal to do this to avoid intraday fluctuations affecting the sample for ATR.

EDIT: applies to forex and other 24hour markets of course. If you trade a market with 5 h4 bars per trading day then you'd want your step to be 5 :)

E

M

HH

b

bentra

13.02.2022 22:43

Not that I personally feel this is really all that critical but it is super weird to have steps for trailing stop and not the stop loss itself.

AA

k

Votes: +18

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}