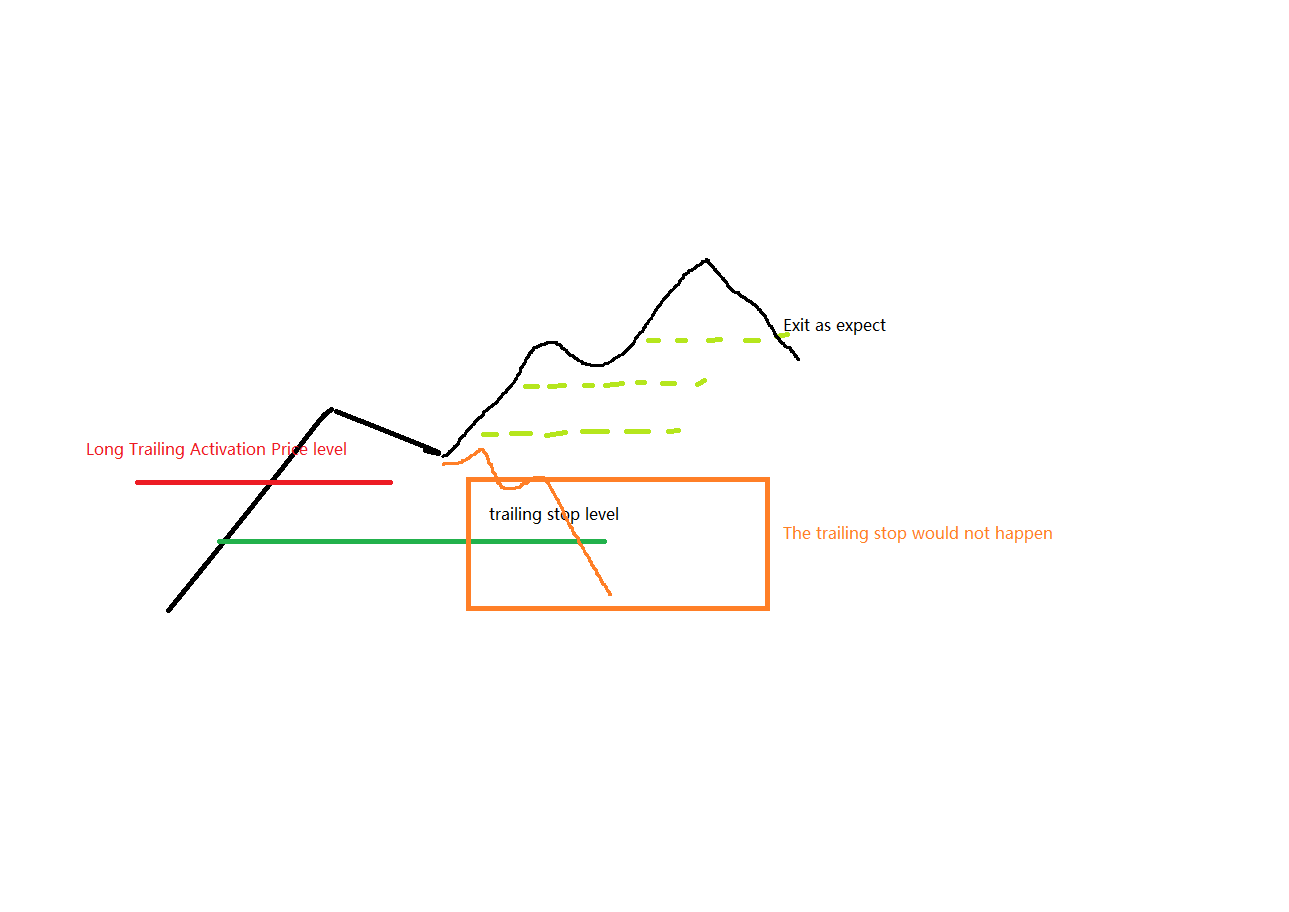

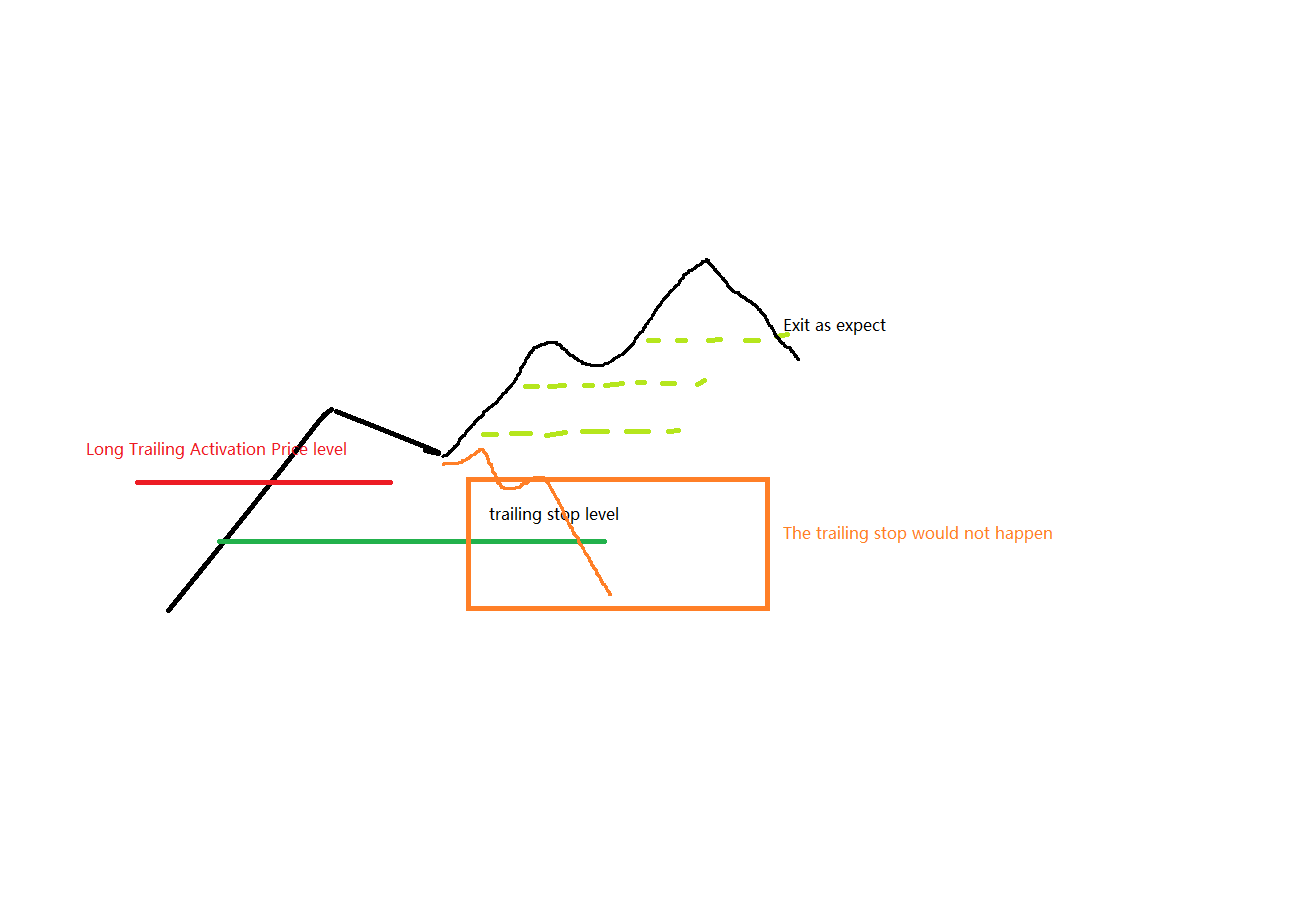

Trailing Activation must be wrong

b131 dev2

backtest engine : multicharts

if(MarketPosition > 0) then begin

...

// Trailing Stop

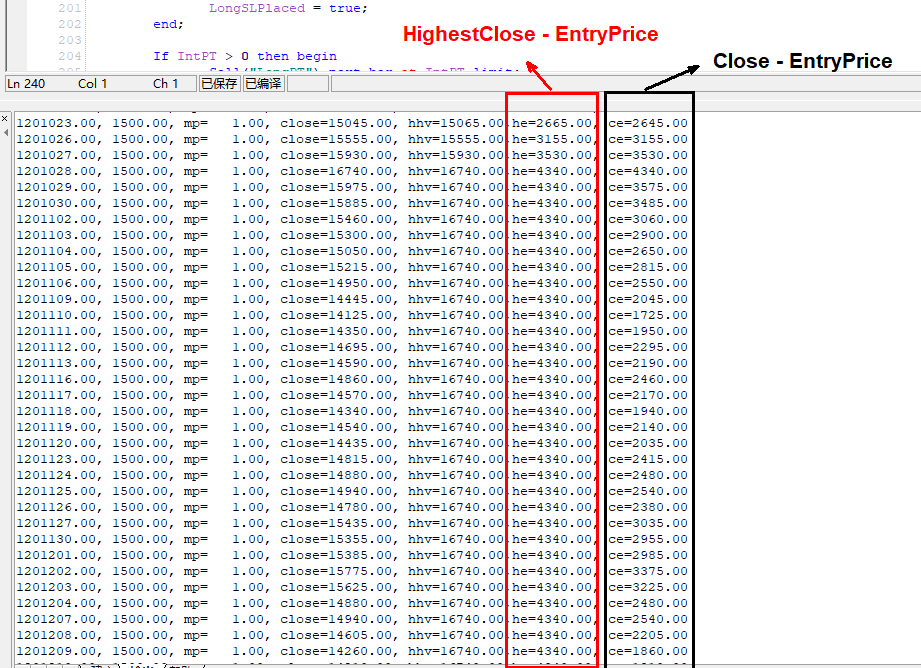

IntPriceLevel = SQ_Highest(WeightedClose, Period)[0] + (0.80 * SQ_BiggestRange(Period2)[2]);

If IntPriceLevel > 0 and Close - EntryPrice >= Round2Fraction(TrailingActCef * SQ_ATR(20)[1]) and (IntLongTS = 0 or Round2Fraction(IntPriceLevel) > IntLongTS) and Round2Fraction(IntPriceLevel) < CurrentBid then begin

IntLongTS = Round2Fraction(IntPriceLevel); // remember also trailing stop

end;

If IntLongTS > 0 and IntLongTS > IntLongSL then begin

Sell("LongTrailingStop") next bar at IntLongTS stop;

LongSLPlaced = true;

end;

We know here the trailing stop activation is up to Close - EntryPrice >= TrailingActCef * SQ_ATR(20)[1],

But the right way is, Highest price after entry - EntryPice > trailing activation trigger, example in long position

if(MarketPosition < 0) then begin

...

If BarsSinceEntry = 0 then begin

...

HighAfterEntry = Close;

end;

if Close > HighAfterEntry then

HighAfterEntry = Close;

// Trailing Stop

...

If IntPriceLevel > 0 and HighAfterEntry - EntryPrice >= Round2Fraction(TrailingActCef * SQ_ATR(20)[1])

and ... then begin

...

end;

-

Votes +3

-

Project StrategyQuant X

-

Type Bug

-

Status Refused

-

Priority Normal

History

e

k

HH

e

MF

Mark Fric

12.05.2021 09:45Status changed from New to Refused

you are right that this is one way how it could work - TS will be active once it has been activated.

Unfortunately, we don't have it like this - activation level is checked every time and modifying this would change results of all the existing strategies, so we cannot do it.

We'd have to make a second type of Trailing Stop that would behave like this.

In any case, I don't think one style or another causes that much difference in trading, we have bigger priorities with much bigger impact now.

Votes: +3

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}