signs of severe rounding issues in r-expectancy SCORE. Solution included.

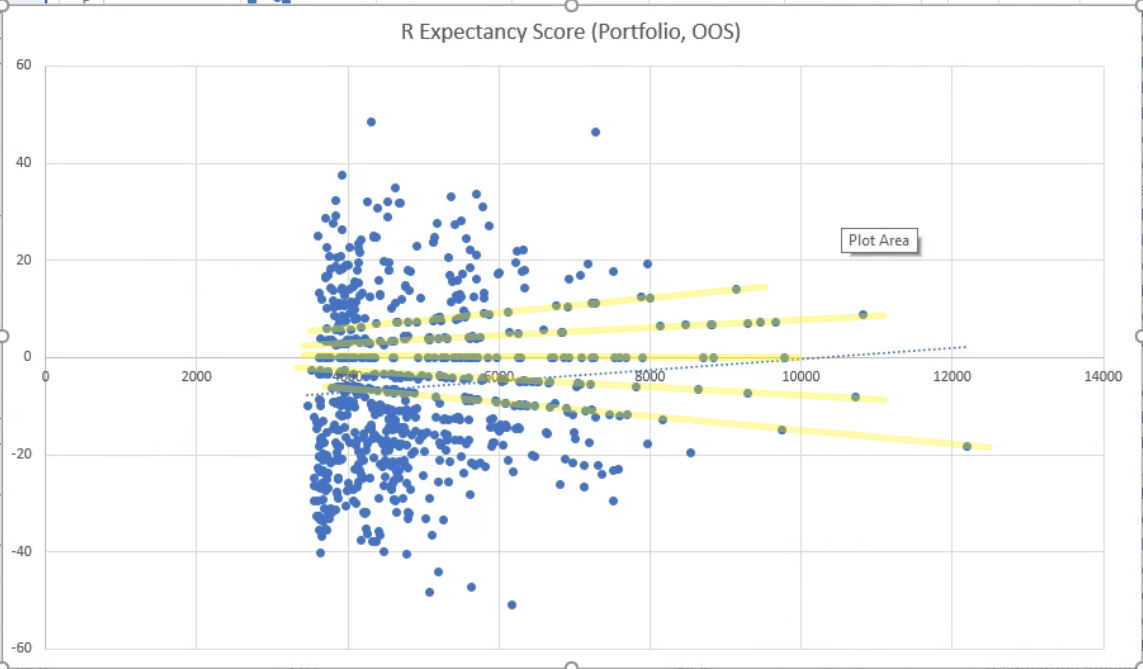

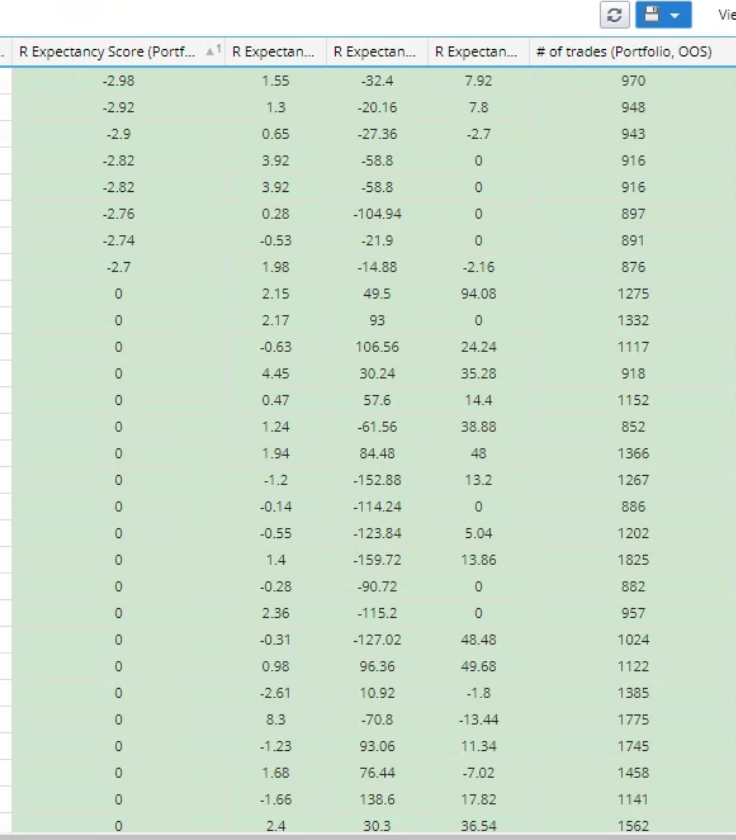

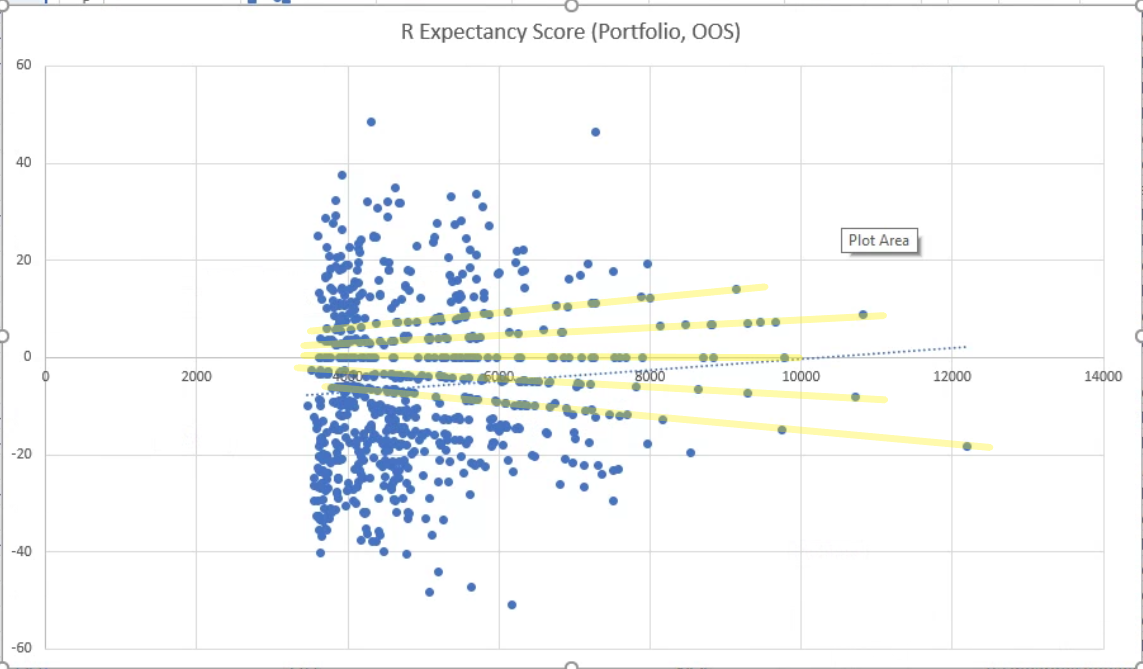

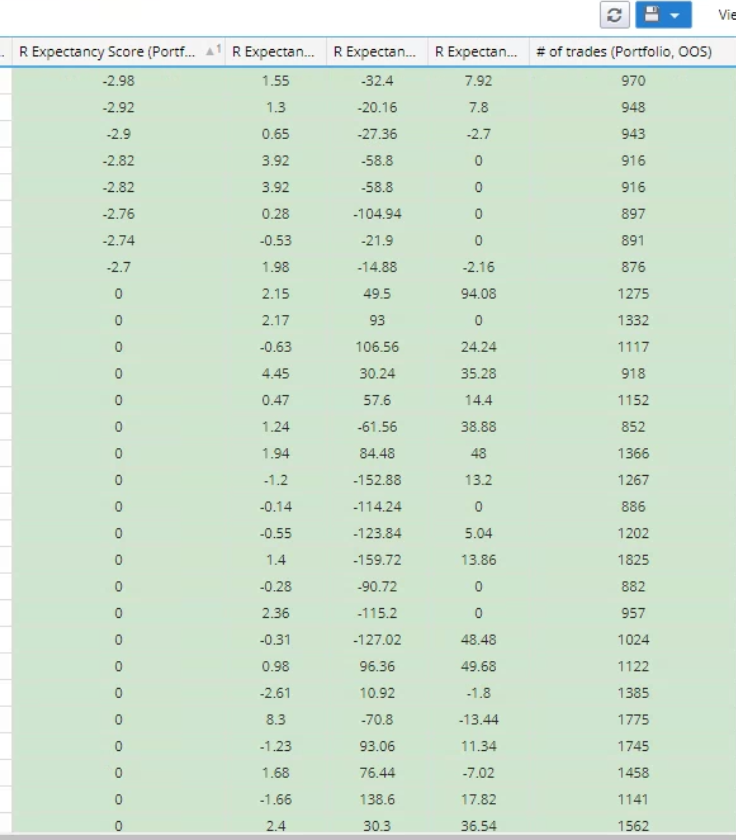

The 2 decimal "output accuracy" of r-expectancy score itself is not the problem. Something within the formula is being rounded way too much. You can see the "gan line pattern" in the r-expectancy chart, (everything is rounded to the nearest line) the more trades there are the less accurate (more rounded) r-expectancy SCORE becomes, also, with 1k trades in OOS, you can see in the table many 0's and nothing in between ~ 2.7 and ~ -2.7.

EDIT:

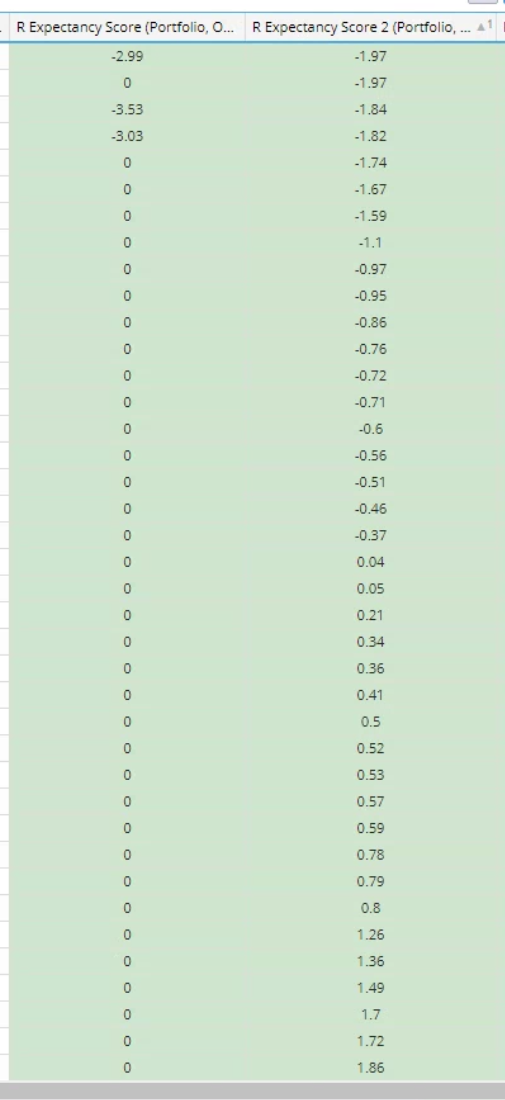

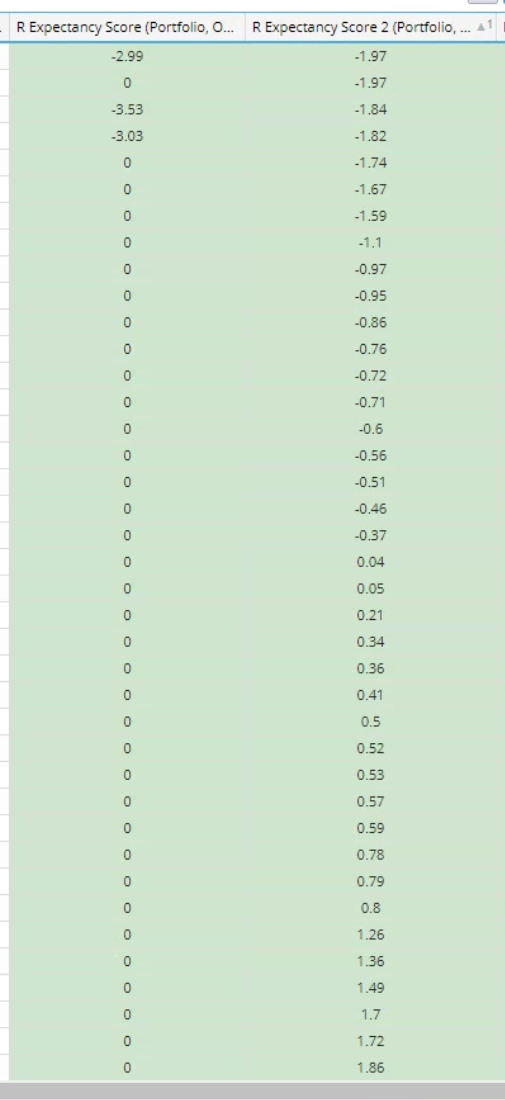

The solution is to base the r-expectancy SCORE column on a more accurate r-expectancy column. By simply creating an r-expectancy column that is accurate to 4 decimals instead of two and then creating an r-expectancy SCORE column based on this more accurate r-expectancy column I was able to eliminate the rounding issues.

To be clear:

R-expectancy rounded to 4d,

R-expectancy SCORE based on the more accurate R-expectancy but R-expectancy SCORE still rounded to 2d

EDIT:

The solution is to base the r-expectancy SCORE column on a more accurate r-expectancy column. By simply creating an r-expectancy column that is accurate to 4 decimals instead of two and then creating an r-expectancy SCORE column based on this more accurate r-expectancy column I was able to eliminate the rounding issues.

To be clear:

R-expectancy rounded to 4d,

R-expectancy SCORE based on the more accurate R-expectancy but R-expectancy SCORE still rounded to 2d

-

Votes +5

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

b

b

b

bentra

31.03.2022 18:35

The solution is to base the r-expectancy SCORE column on a more accurate r-expectancy column. By simply creating an r-expectancy column that is accurate to 4 decimals instead of two and then creating an r-expectancy SCORE column based on this more accurate r-expectancy column I was able to eliminate the rounding issues.

SF

M

E

CG

Votes: +5

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}