[B136 Dev1] Optimizer: class com.strategyquant.tradinglib.SwapMethod cannot be cast to class com.strategyquant.tradinglib.CommissionsMethod

I am trying to optimize a strategy from build 135 that (of course) didn´t use any swap. Loading the strategy to the optimizer and then just trying to optimize even one variable always fails with:

23:18:14 class com.strategyquant.tradinglib.SwapMethod cannot be cast to class com.strategyquant.tradinglib.CommissionsMethod (com.strategyquant.tradinglib.SwapMethod and com.strategyquant.tradinglib.CommissionsMethod are in unnamed module of loader com.strategyquant.launcher.EmbeddedClassLoader @1dd92fe2) 23:18:14 Brute Force method 23:18:04 Testing original parameters 23:18:04 Testing original strategy 23:18:04 Running simple optimization on Strategy 2.57.2397

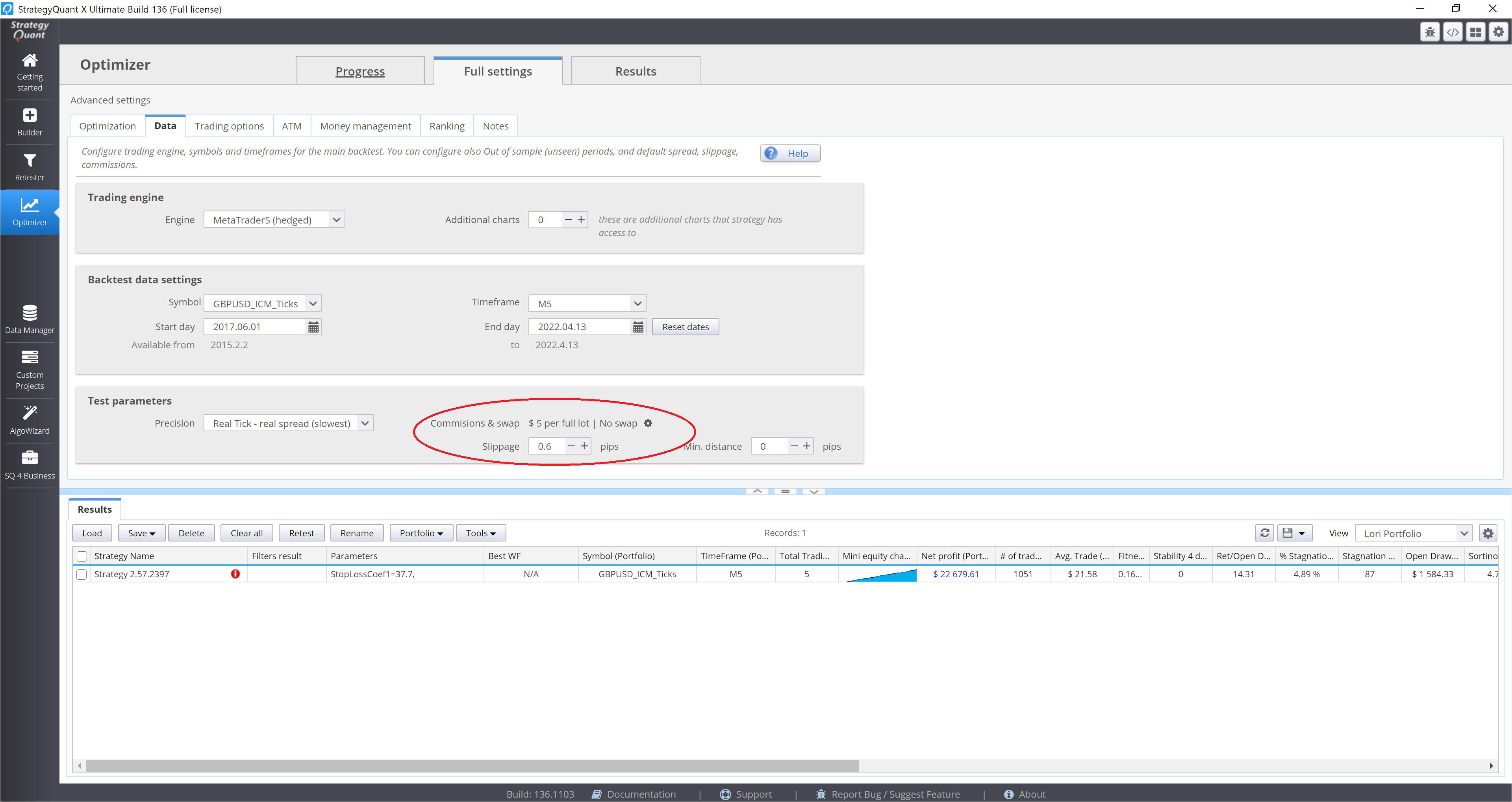

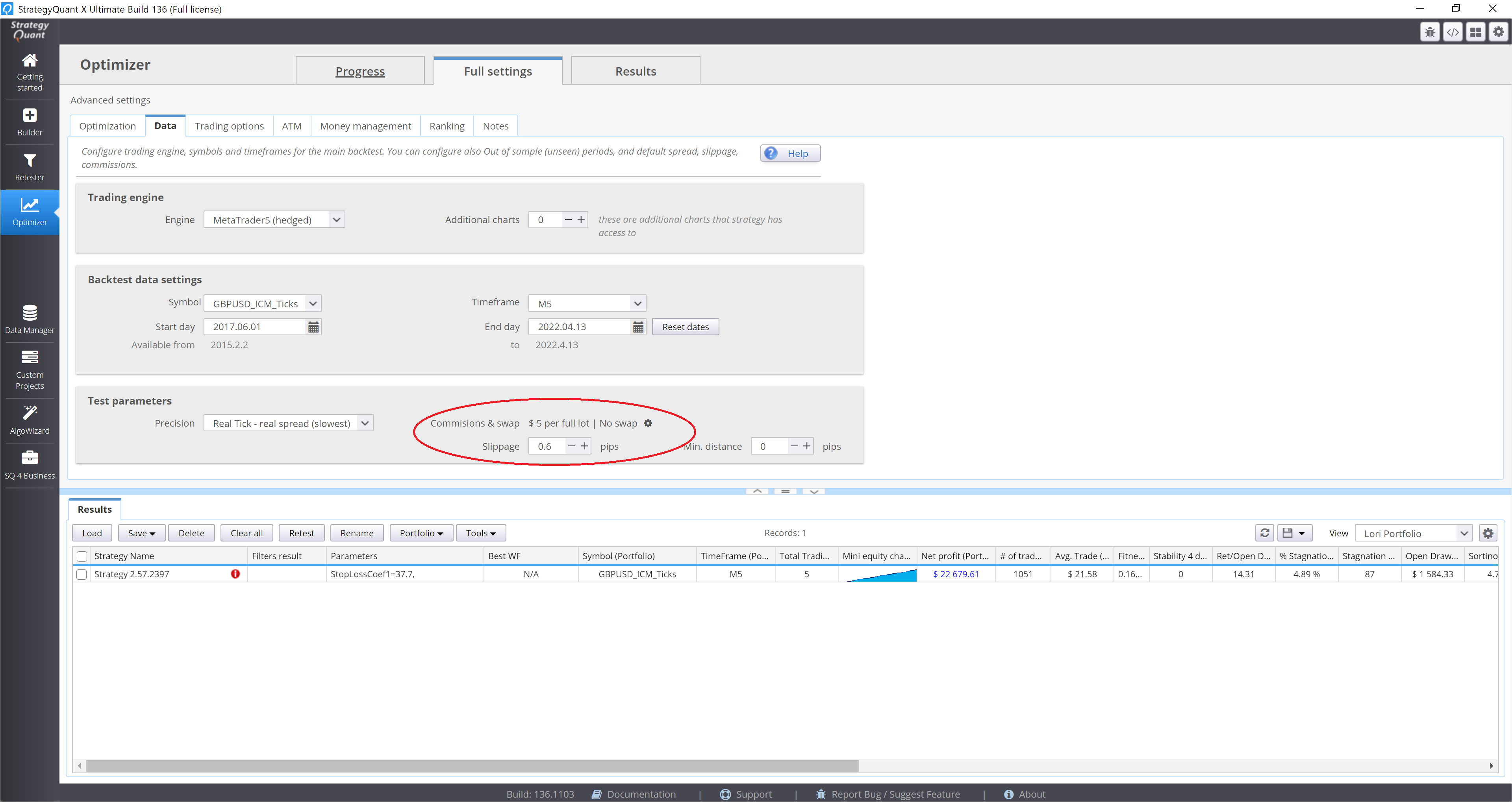

I didn't set any swap, it says "No swap" in the Test Parameters (see screenshot). The same error appears if enabling Swap. This happens with any strategy I am trying to optimize.

-

Votes +8

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

g

b

E

JJ

g

IN

Cc

BP

KB

Votes: +8

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}