Add test to verify edge in entry & exit (including BRILLIANT sample, take a look at it)

Hi,

Sometimes in a strategy, we think we found an edge to enter the market, but in reality our entry has no edge.

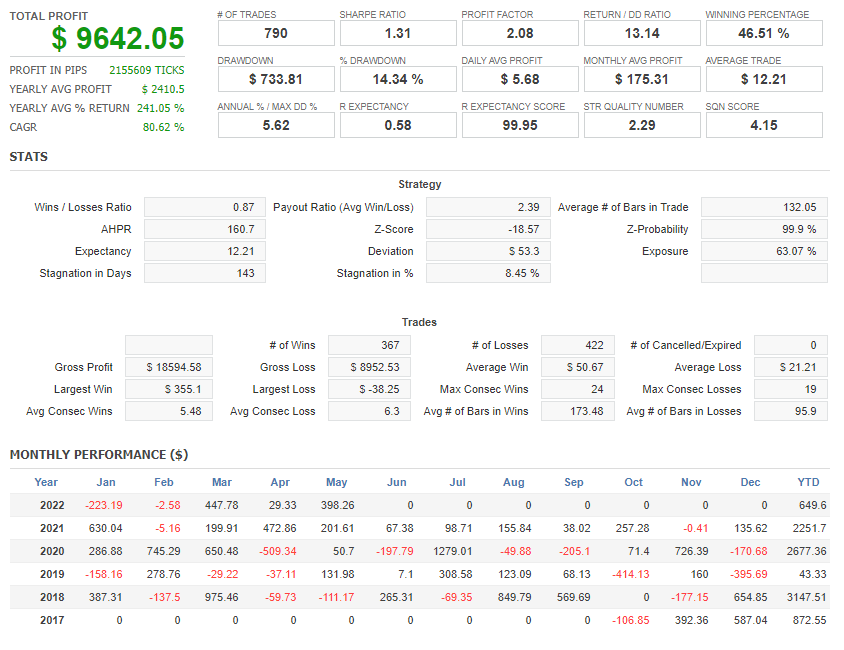

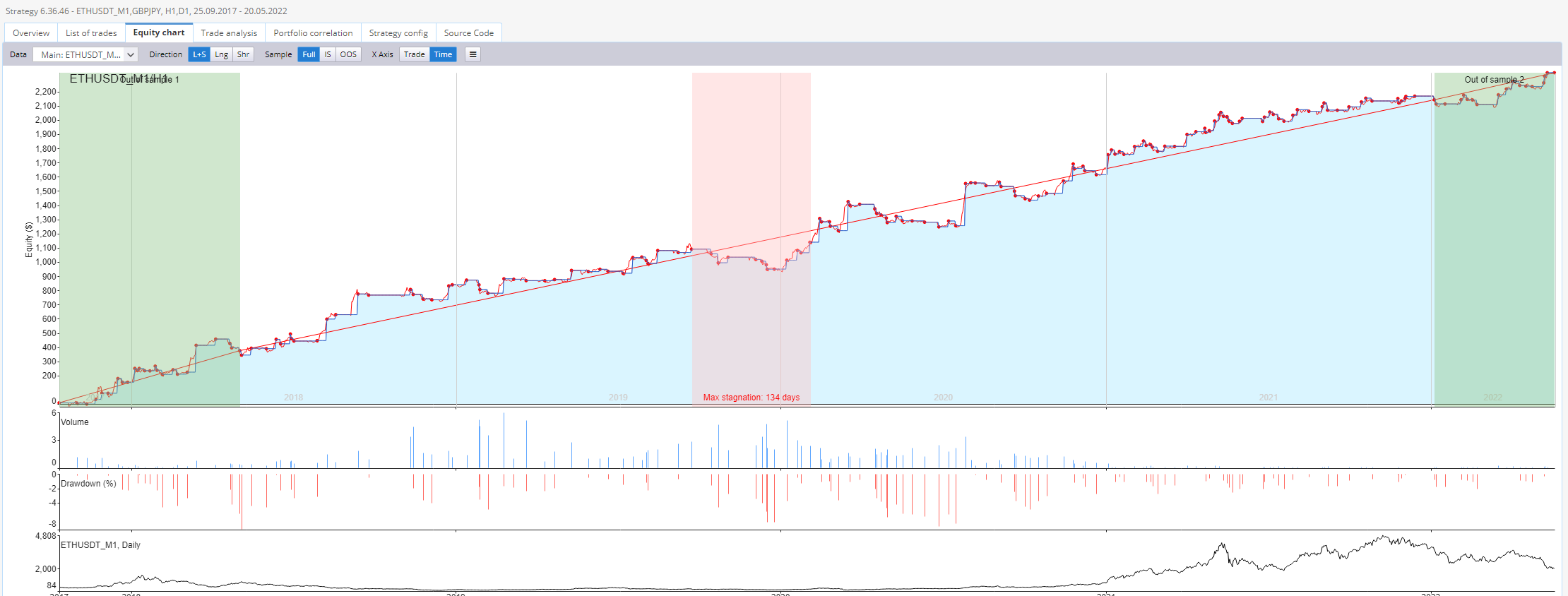

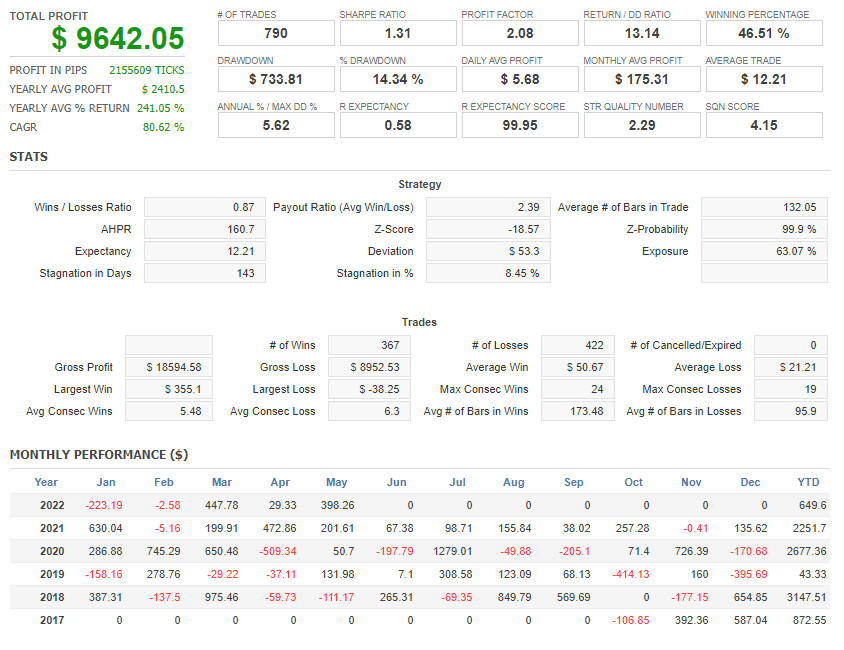

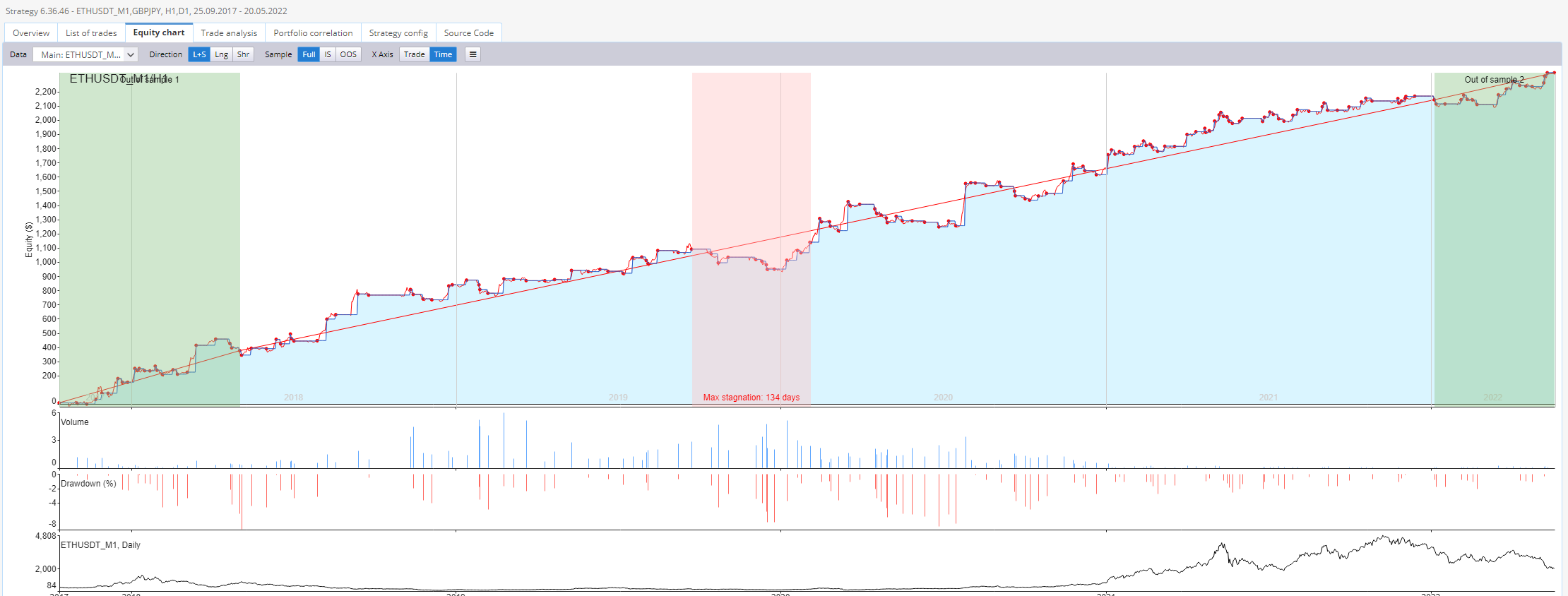

Take a look at the curve attached, it looks brilliant with very good metrics: PF=2.08, and Ret/DD = 13.14 over 5 years with a stagnation of only 134 days!

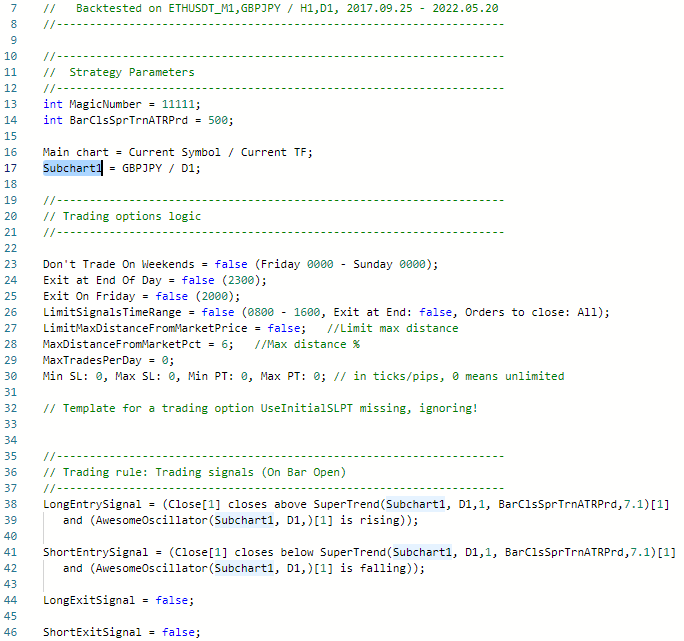

Now look at the attached strategy and see the entry.

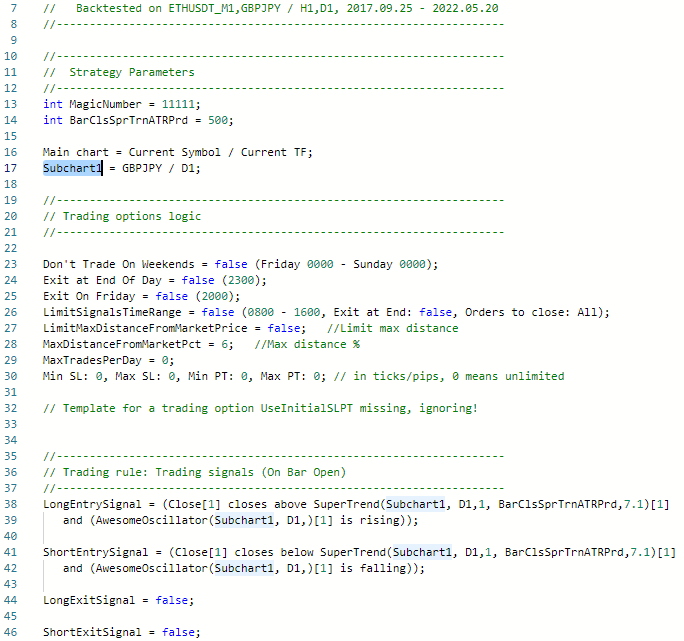

It enters trades on ETH/USD based on signals ONLY from GBP/JPY.

We know that GBP/JPY has no correlation with Cryptos.

So don't you think it's completely based upon chance?

By the way, I attached this sample for a reason.

It's good to have a test to see whether our strategy has an edge in entry/exit really or not.

I think if we just enter this market at some point randomly, we could have some good results such as this one.

Please add a test to randomly enter the market, and exit as strategy defines, add a test to enter by strategy but exit randomly and so on.

If we repeat above tests e.g. 100 times, we can be sure that our entry/exit have edge if our strategy do better than 95% of above tests

This idea is based upon Chapter 12 of a book from Kevin Davey: Building Winning Algorithmic Trading Systems.

-

Votes 0

-

Project StrategyQuant X

-

Type Feature

-

Status New

-

Priority Normal

History

AA

Votes: 0

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}