[B136_Dev5][AlgoWizard] No "MoneyManagement method" is set in portfolio.

Steps to reproduce:

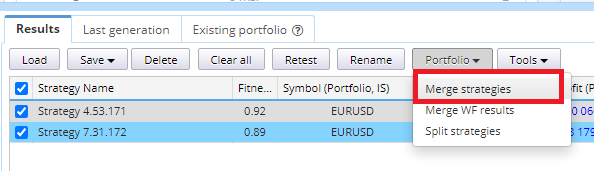

1: Load "Strategy 4.53.171.sqx" and "Strategy 7.31.172.sqx" into "Results" databank in Builder

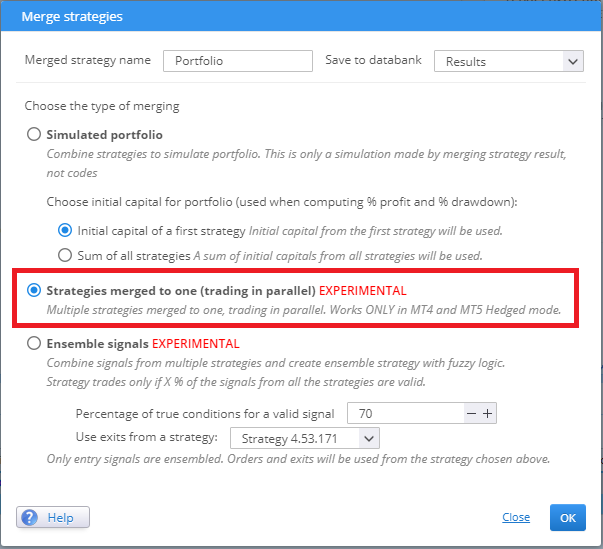

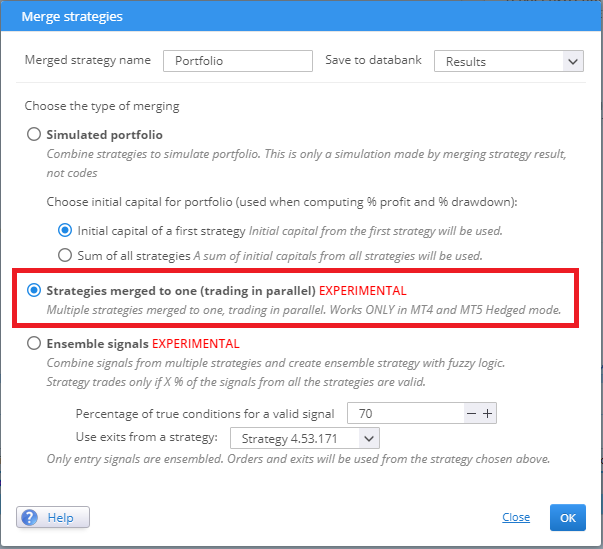

2: Select two strategies and choose "Portfolio" -> "Merge strategies".

3: Select "Strategies merged to one(trading in parallel)".

4: Save the generated portfolio as portfolio.sqx.

5: Open AlgoWizard

6: Load Strategy 4.53.171.sqx and run "Run quick backtest", to ensure we can get the result.

7: Load Strategy 7.31.172.sqx and run "Run quick backtest", to ensure we can get the result.

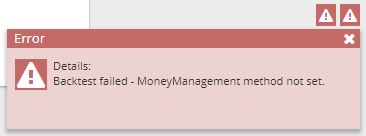

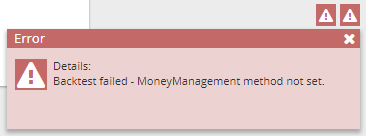

8: Load portfolio.sqx and run the "Run quick backtest", and "Backest failed. MoneyManagement method not set" dialog appear.

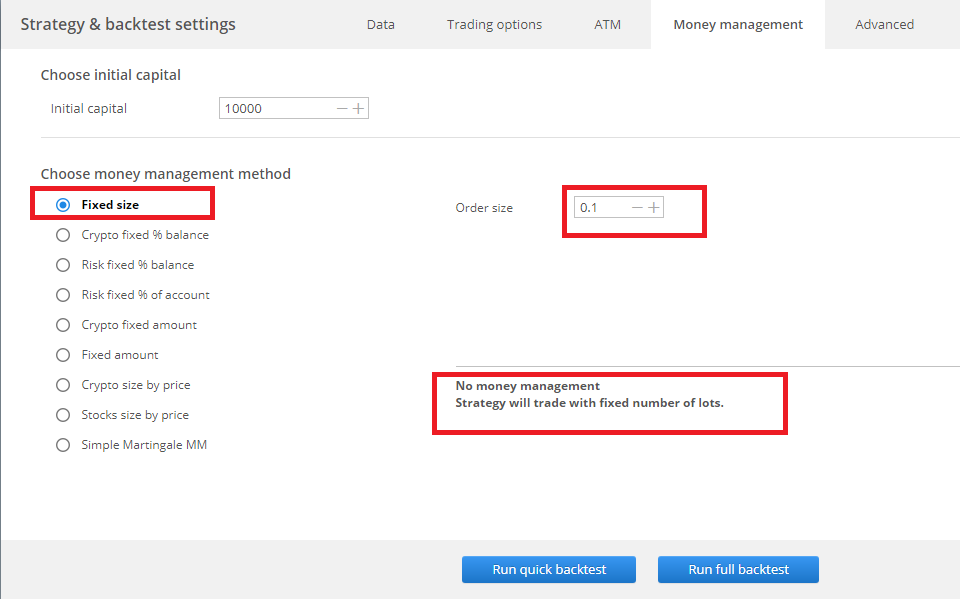

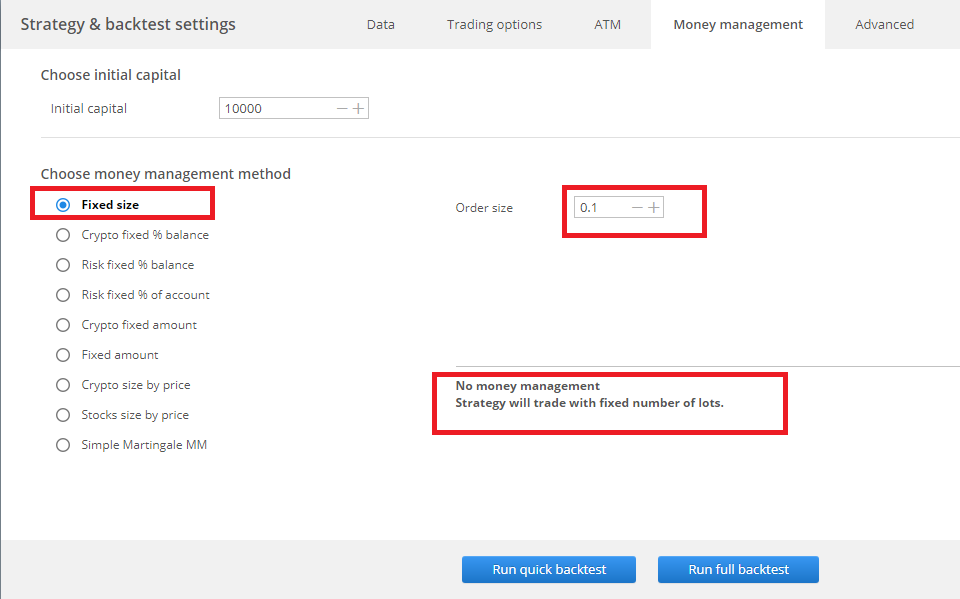

9: Open "settings".

10: Select the "Money management" tab.

11: Ensure there is a "Strategy will trade fixed number lots" and "Fixed size" and "0.1" value.

12: Click "Run quick backtest".

13: "Backest failed. MoneyManagement method not set" dialog appears again.

Problem:

1: "Strategy 4.53.171.sqx" and "Strategy 7.31.172.sqx" have a "MoneyManagement method", so the quick backtest succeeded.

But the portfolio doesn't have a "MoneyManagement method".

2: Even though I can see "Strategy will trade fixed number lots" and "Fixed size" and "0.1" value in the "Strategy & backtest settings" page, the quick backtest failed. The data is not passed to the quick backtest.

-

Votes +1

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

Lee Guan Chuan

09.02.2023 08:49Status changed from New to Fixed

I have fixed the "Money Management" issue. However, the portfolio are meant for code compilation/generation. Portfolio are not able to backtest in SQX.

Thank you.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}