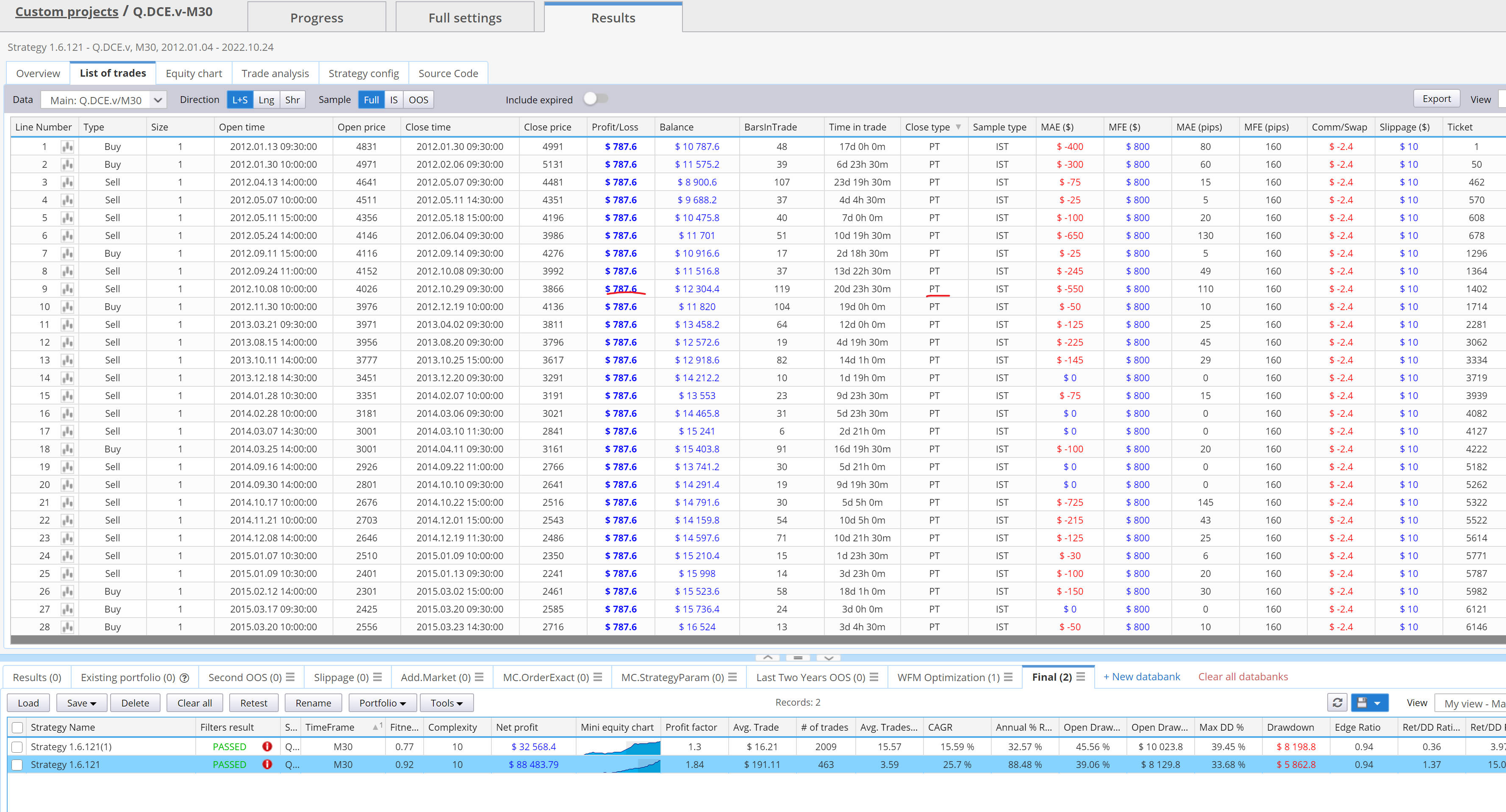

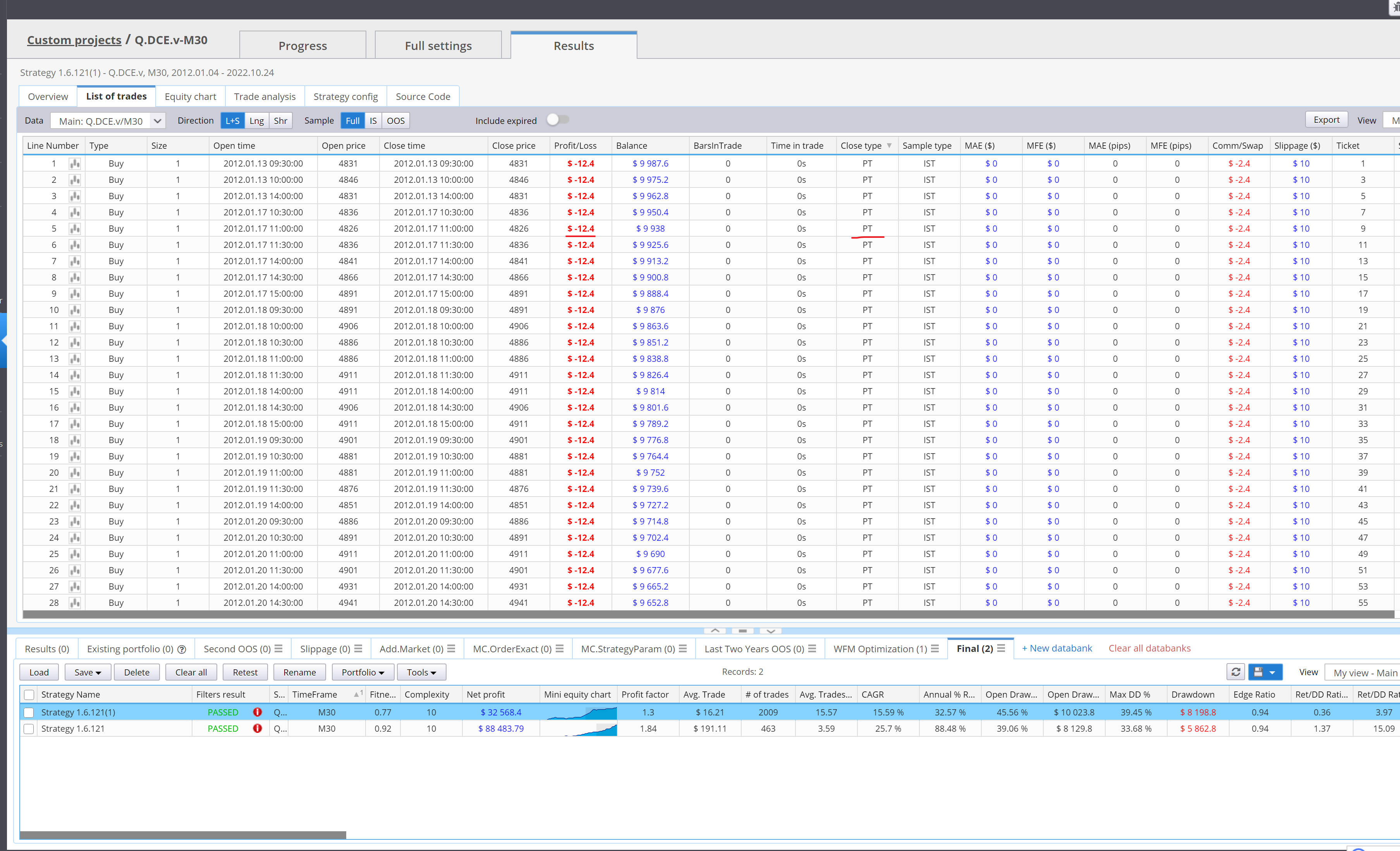

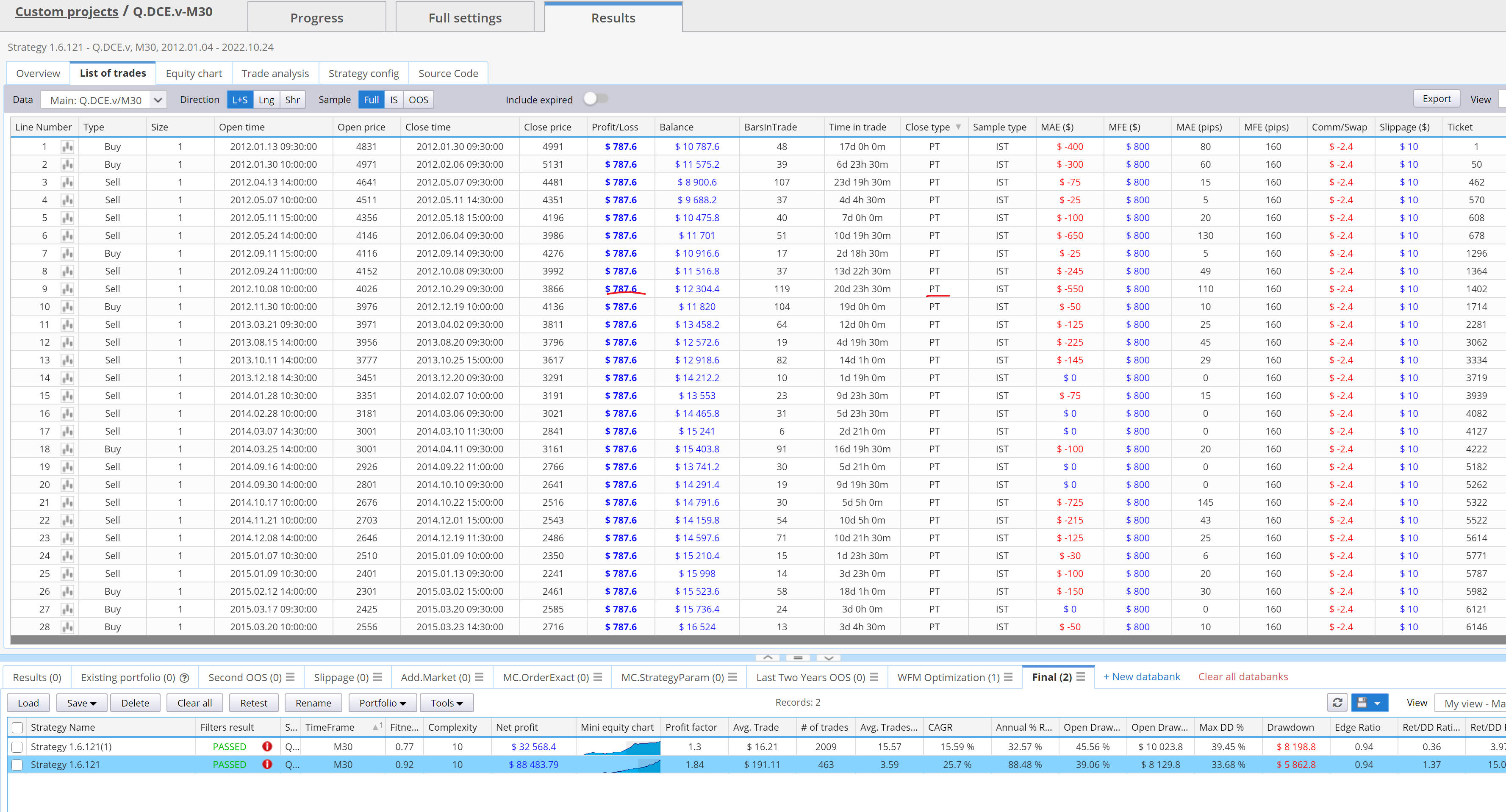

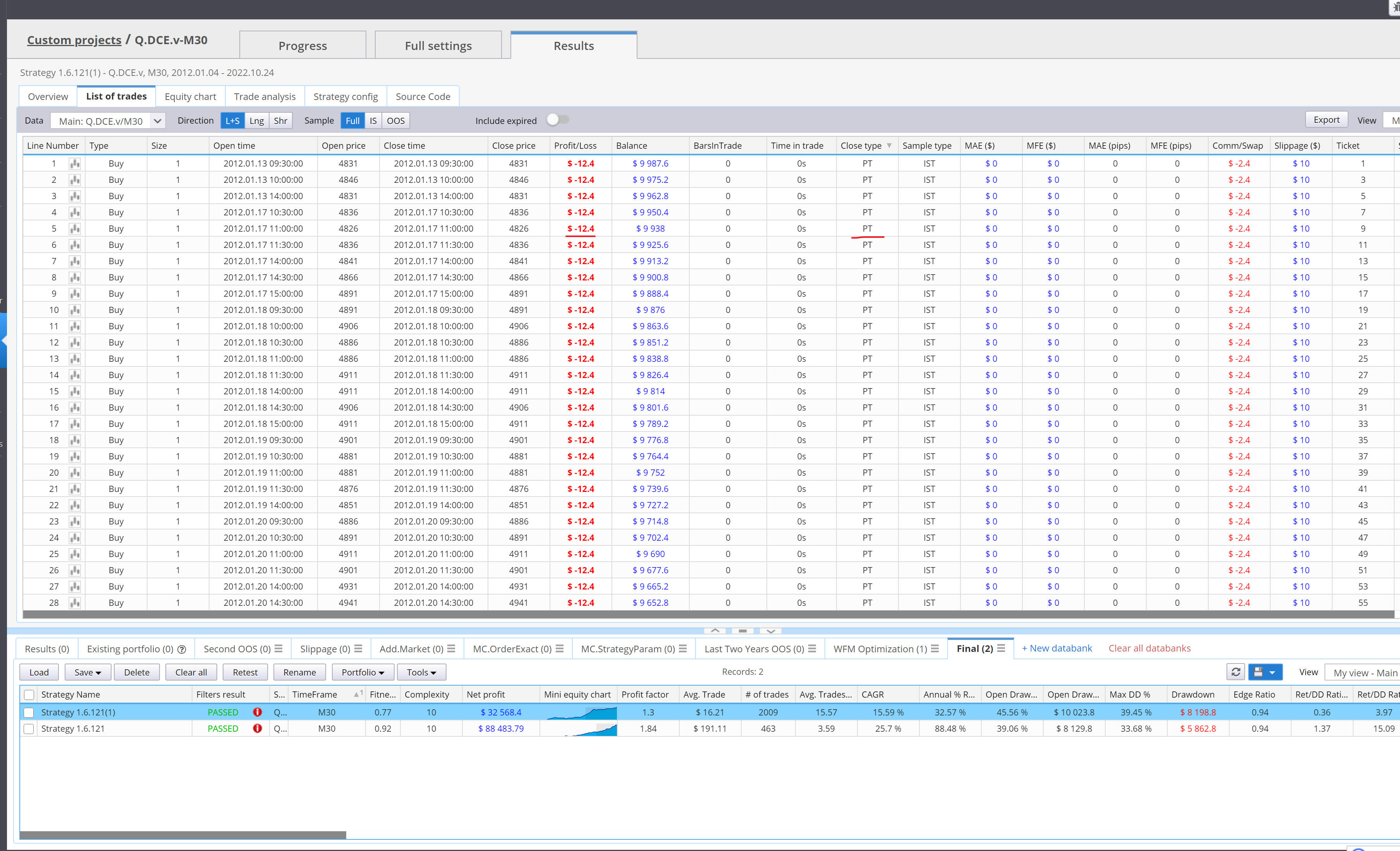

[SQ 136Final] The value of useinitialstoploss has an unusually large impact on the results of the strategy backtesting

And two different codes, I put them on MC for backtesting, but the results are very close.The final Netprofit is about 88000 whether useinitailstoploss is true or false.

I did a similar backtest on multiple strategies, and there was a huge difference in just this strategy, which is also very strange.Although I was confused, I probably thought that sq had made some mistakes.

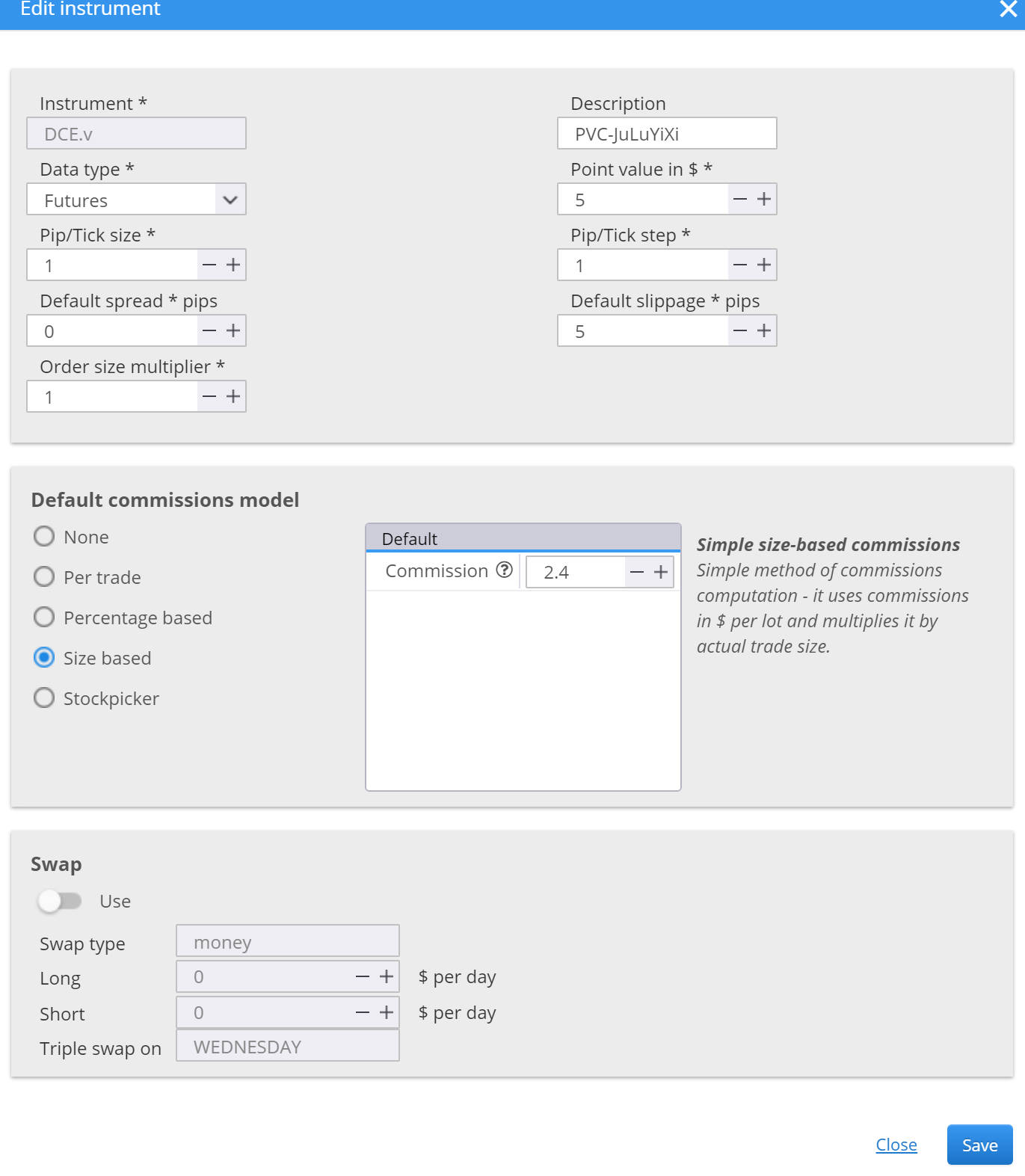

PS: slippage=5 pips

-

Votes +2

-

Project StrategyQuant X

-

Type Bug

-

Status New

-

Priority Normal

History

binhsir

31.01.2023 15:17This must be a serious bug.

1.By the way, in the source code, there are two variables IntLongSL,IntShortSL. but only one variable IntPT. The same variable is given different values twice in the code.

2. SetStopLoss((MinMove / PriceScale) * BigPointValue * IntShortSL); This code can actually be changed to SetStopContract; SetStopLoss_pt(IntShortSL); The same is SetProfitTargit_pt. The code will look more concise and elegant in this way.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}