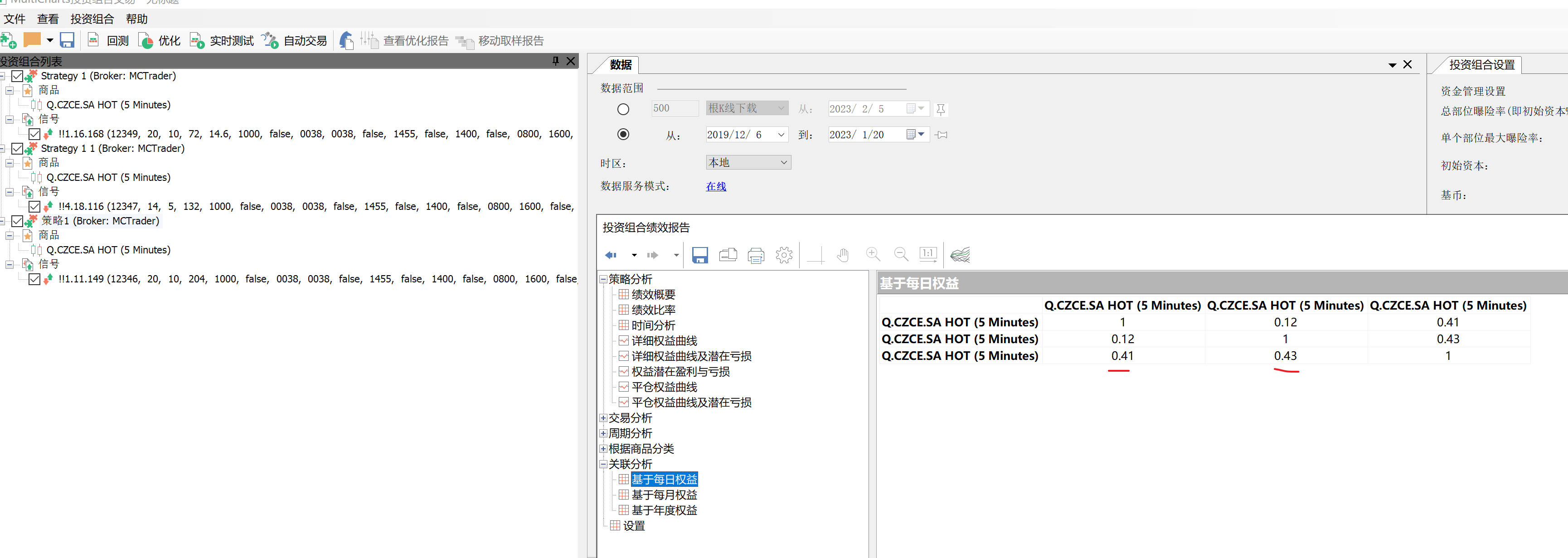

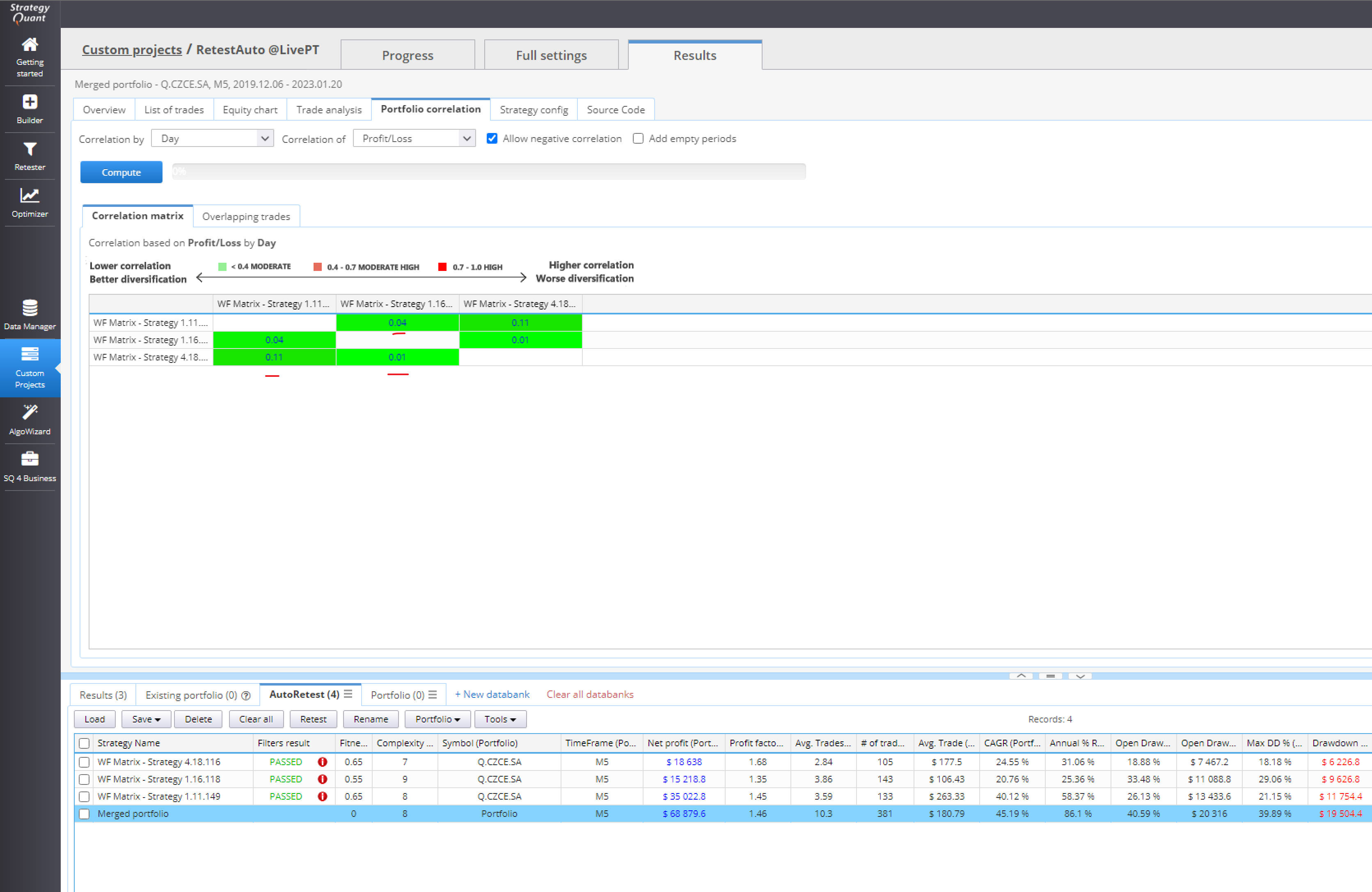

Huge portfolio correlation difference bettween SQ and MC

Is the calculation formula of correlation coefficient different or the choice of profit different? Such as based on open profit or close trade profit.

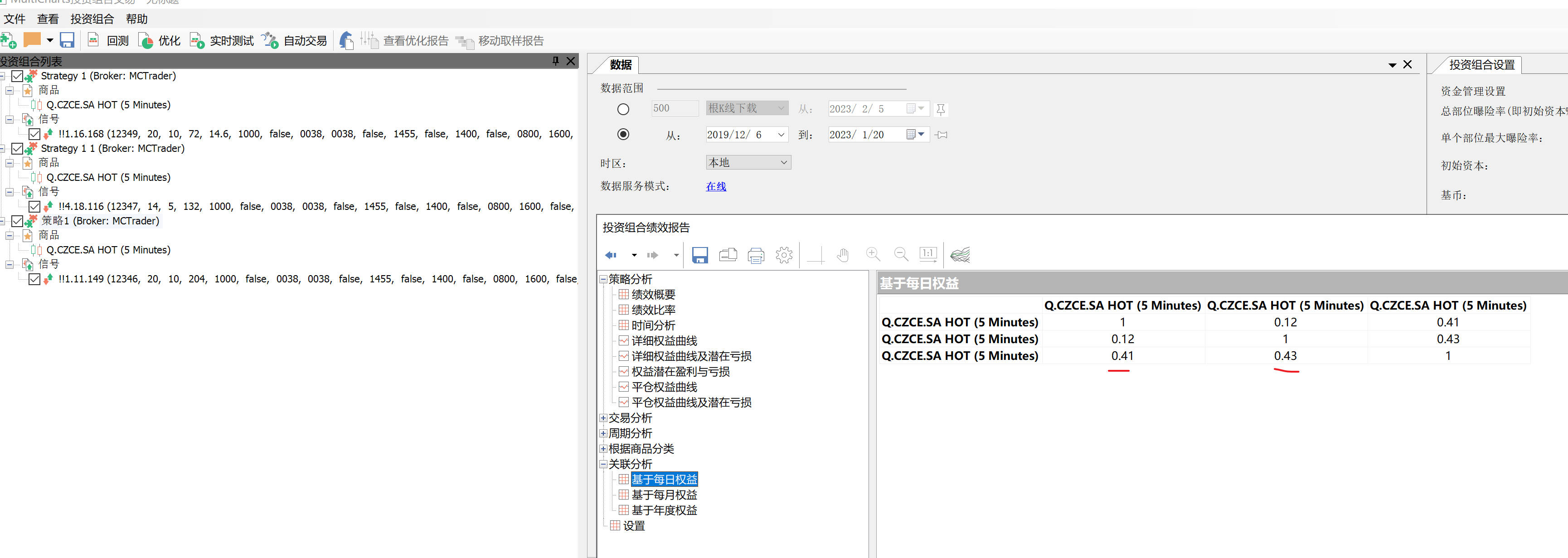

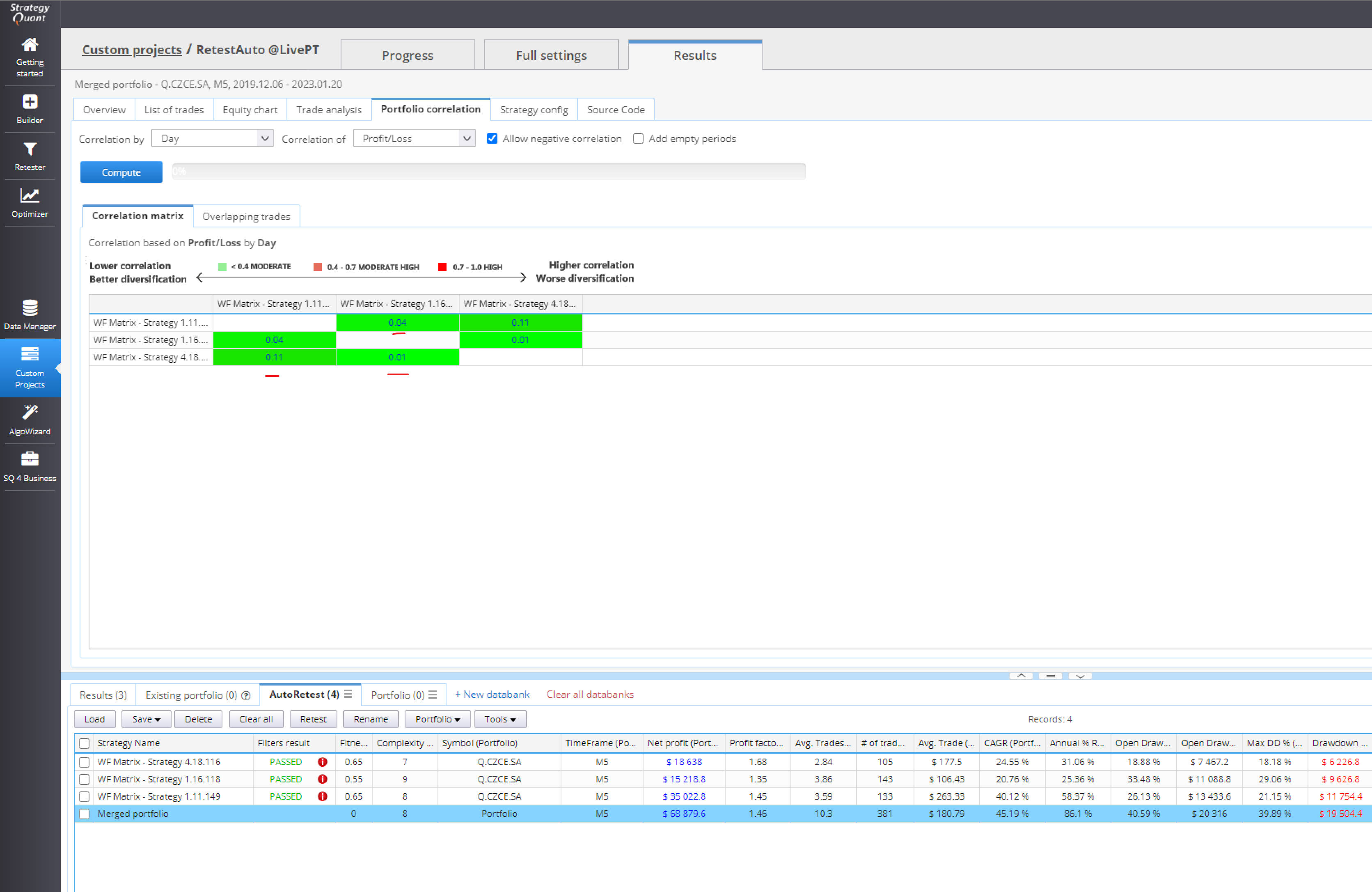

I chose a set of strategies at random, on the same instrument, please refer to attachment.

One more point:

1. there are very different entry and exit time for each trade in two strategies.

2. When calculating the correlation coefficient of the two strategies in any trading software, it is required to select daily profit or weekly profit or montyly profit.

So that mean it is likely to be calculated with daily or weekly or monthly open profit data series , not the closing profit on each trade.

I really hope that the development team will solve this bug as soon as possible. This also helps to make the annual and monthly profit values in the performance report more accurate in SQ. Then it will be more efficient to verify the performance report on the trading platform. Thanks

-

Votes +5

-

Project StrategyQuant X

-

Type Bug

-

Status New

-

Priority Normal

History

binhsir

07.02.2023 02:33This is a bug that is seriously plaguing the build portfolio and has seriously affected my current work progress. It is sincerely hoped that the development team will prioritise fixing it if possible, preferably in version 137.

Also, if it's convenient, please tell me the reason for the bug. Is it something to do with the fact that it is not calculated according to open profit in SQ?

Many thanks.

eastpeace

17.02.2023 04:19+ vx: wanggang_qd , we are trading the same market.

binhsir

16.08.2023 12:48Description changed:

Is the calculation formula of correlation coefficient different or the choice of profit different? Such as based on open profit or close trade profit.

I chose a set of strategies at random, on the same instrument, please refer to attachment.

One more point:

1. there are very different entry and exit time for each trade in two strategies.

2. When calculating the correlation coefficient of the two strategies in any trading software, it is required to select daily profit or weekly profit or montyly profit.

So that mean it is likely to be calculated with daily or weekly or monthly open profit data series , not the closing profit on each trade.

I really hope that the development team will solve this bug as soon as possible. This also helps to make the annual and monthly profit values in the performance report more accurate in SQ. Then it will be more efficient to verify the performance report on the trading platform. Thanks

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}