Wrong statistical results on different levels of confidence when batch Monte Carlo trade manipulation analysis for individual strategies with money management.

First of all,I want to start by stating the importance and high priority of this task. For trading based on volume and price time series strategies, developing robust strategies, constructing low correlation, diversified portfolios and implementing proper money and risk management are all essential.

as an aside, The automatic retest feature in custom project is great and will have unlimited potential. I like it.

Back to the topic:

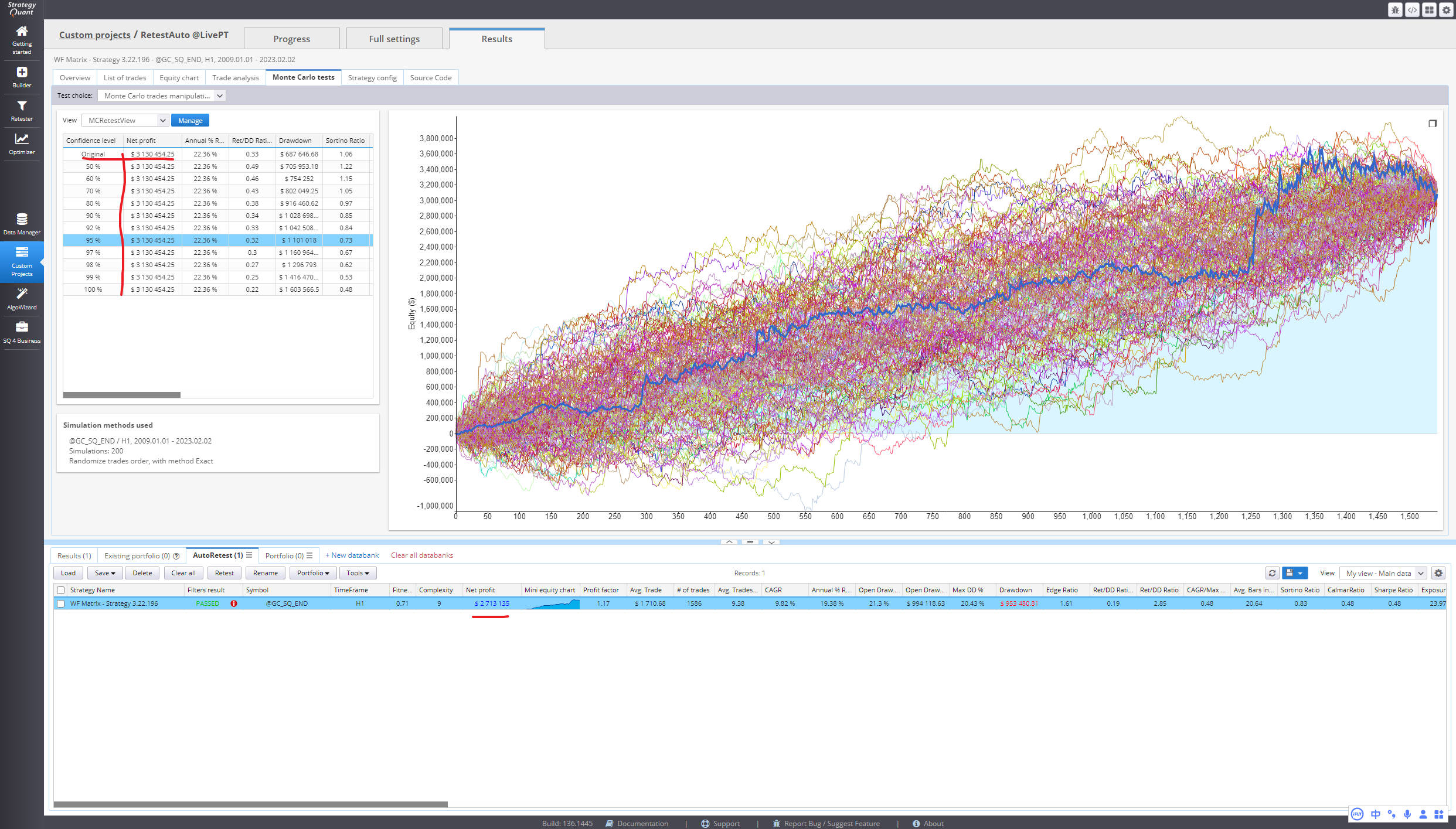

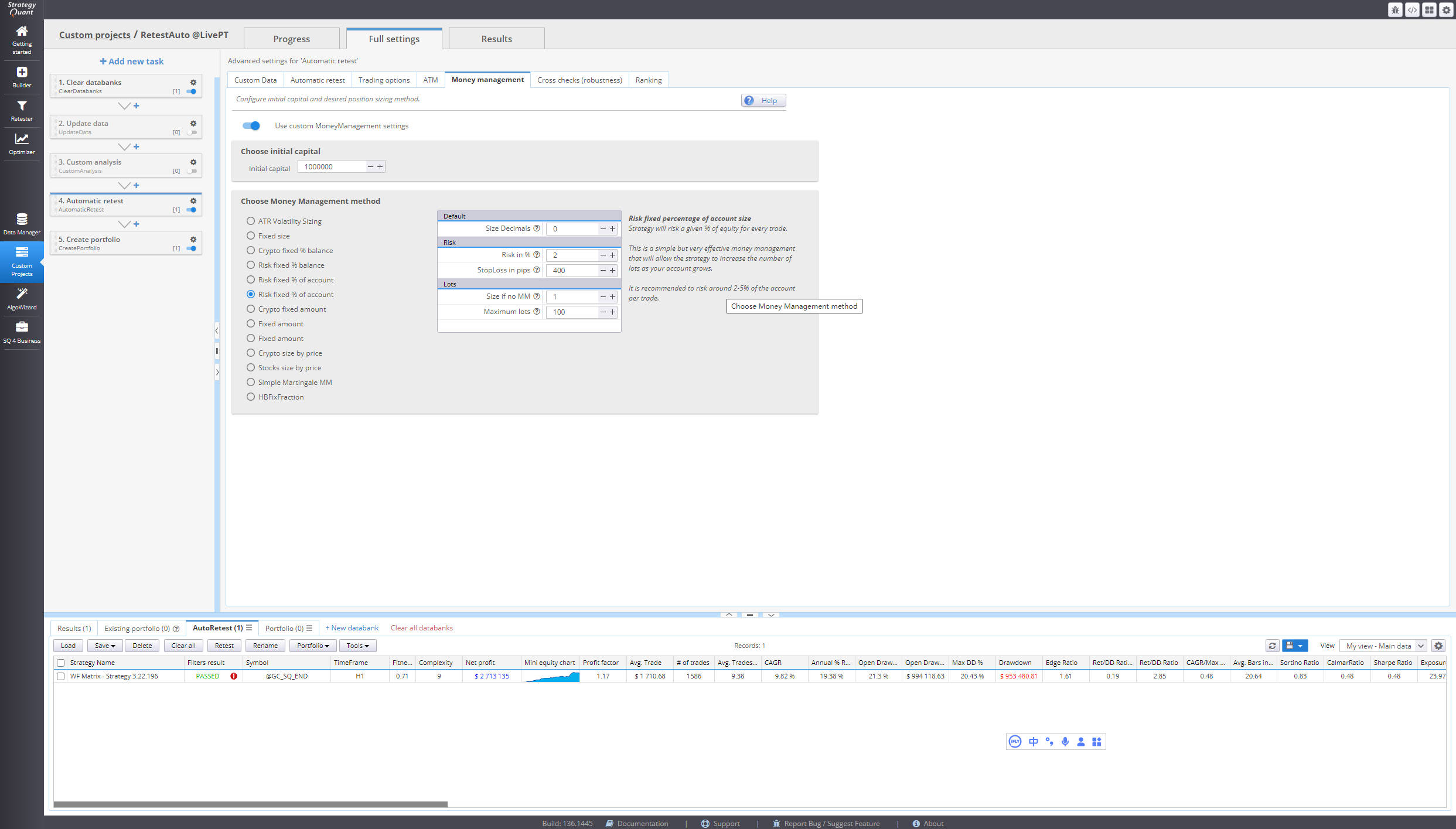

1.This is somewhere between a bug and a feature. We need a Monte Carlo analysis of a strategy with money management. In fact, the software also objectively support to set up Monte Carlo trade manipulation and MM method at the same time. Not only Retester but also Automatic retest task. But as you can see in attachment, we can see from the analysis results that Net Profit is same in any confidence interval.

My guess is that sq simply randomly changed the order of profit per trade . But it is meaningless to do so. Let me explain the theoretical basis, why do we need Monte Carlo trade manipulation analysis?

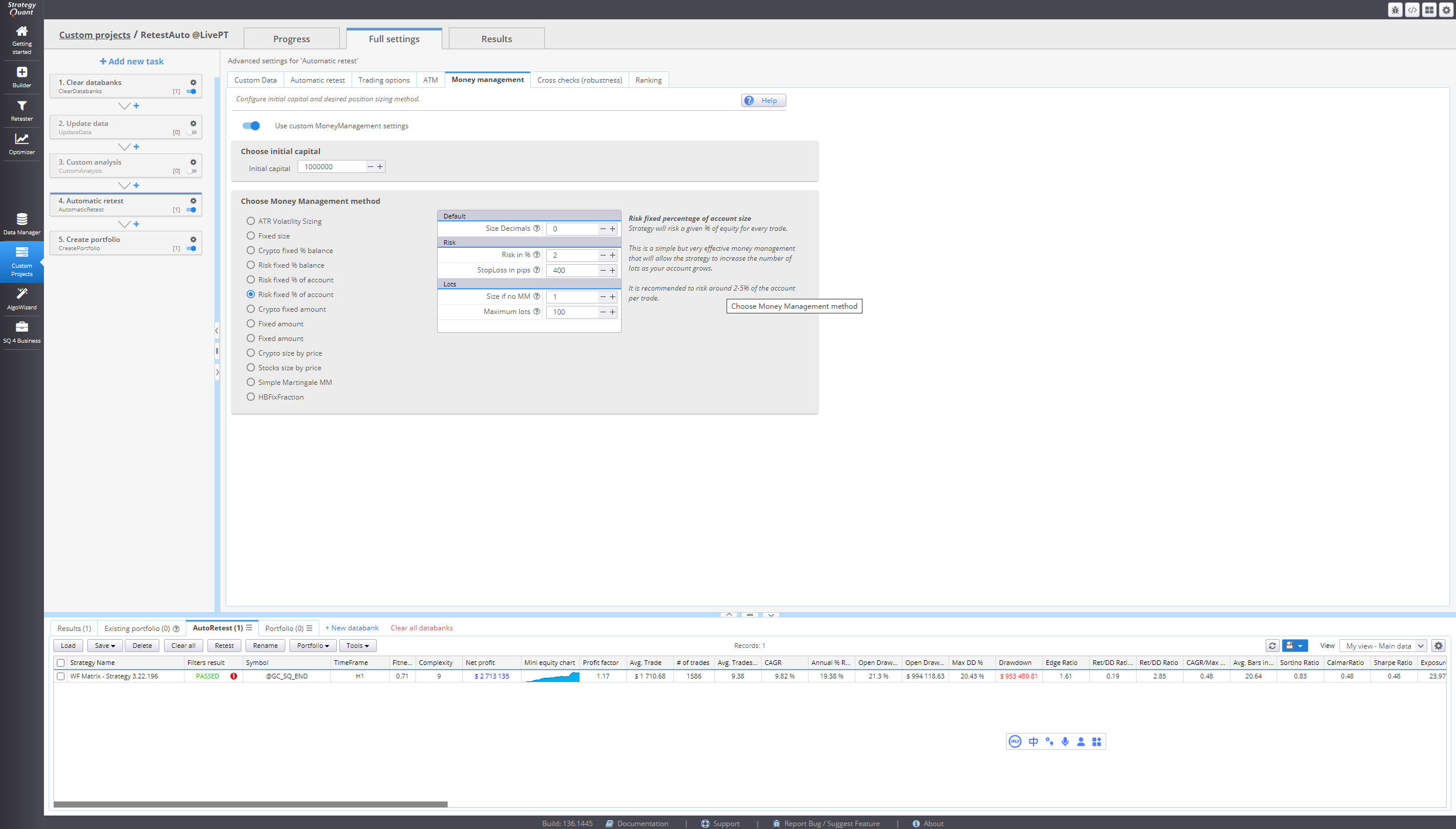

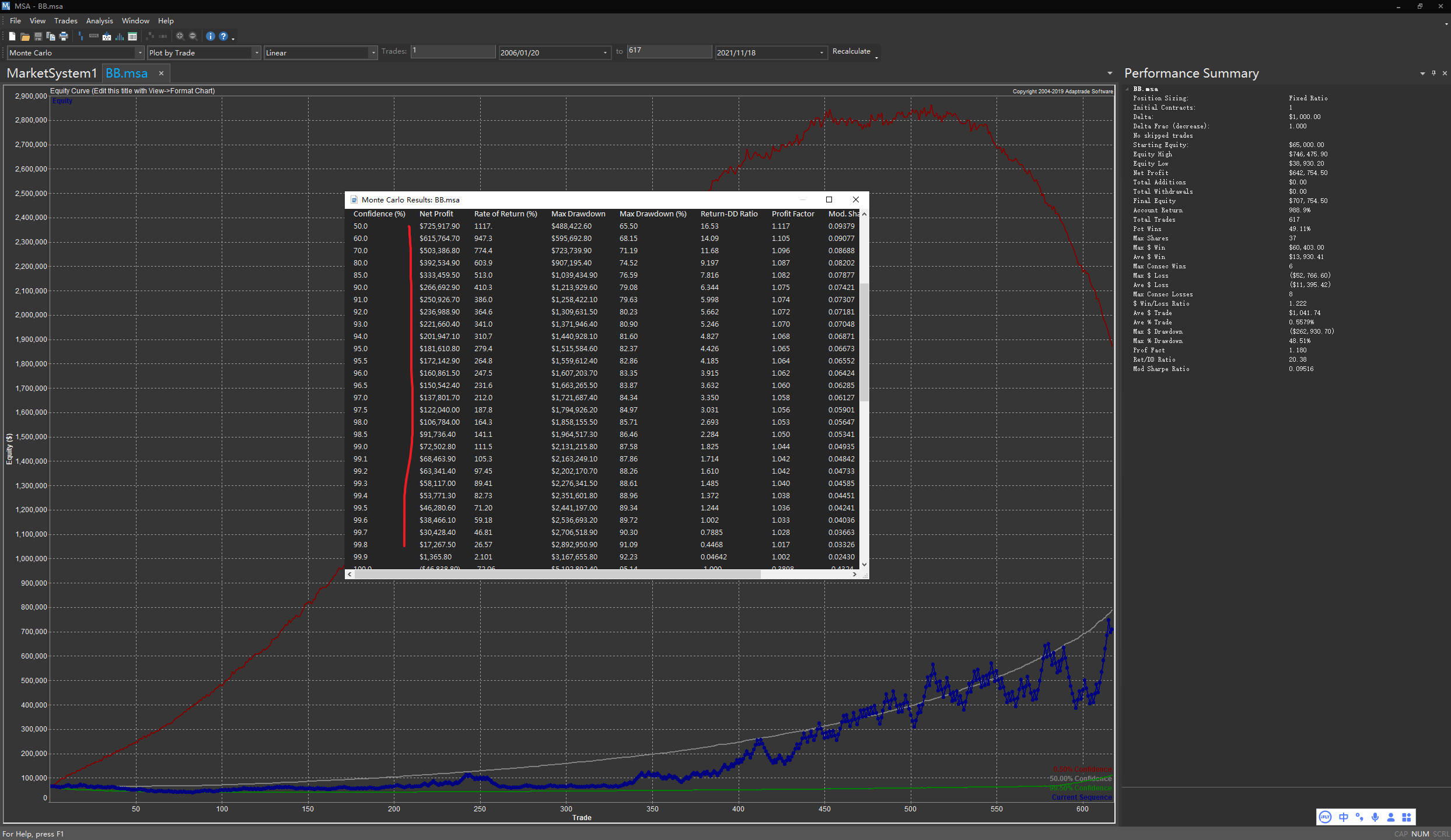

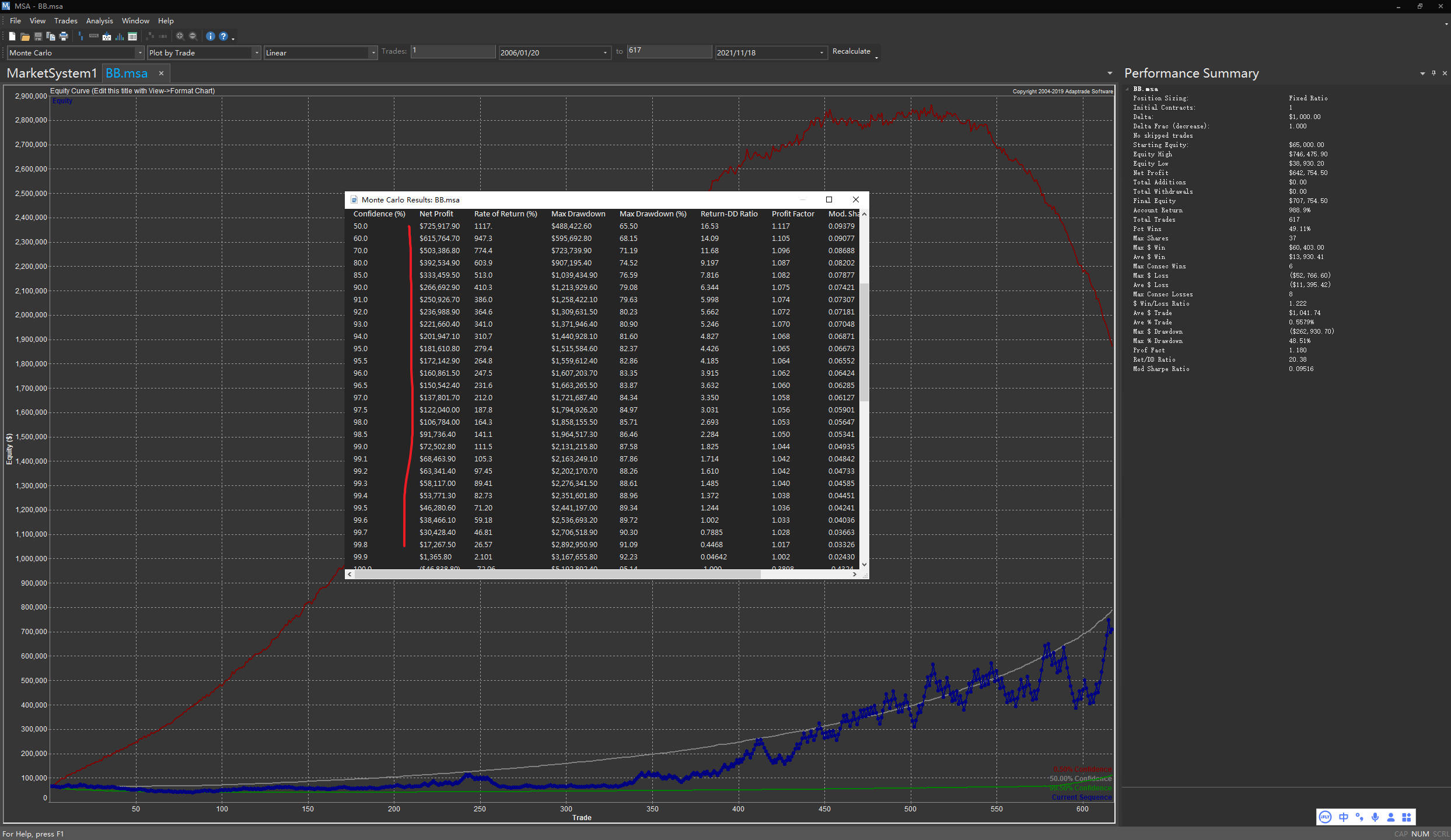

Because the market is cyclical, It could be a bull market or a bear market, high volatility and low volatility and others. We can't predict what will happen in the coming year.Therefore, when doing historical backtesting, we can check the robustness of the strategy by randomly changing the order of price quotations.When the strategy is to fixed one contract, randomly changing the order of the profits per trade is close effect to randomly changing the order of the price quotes. But suppose we use money management,with the constant change of net profit, The number of contracts for every trade is constantly changing. It is inappropriate to directly modify the order of profit per trade at this time. The calculation logic should be to randomly modify the order of profit per contract and then implement the MM method over time. For example, after 500 simulation tests,The net profit should be different in every confidence interval. Every other money management tool I've used has been done like i said. For example, as you can see in the attached screenshot of one of the tools, MSA.

Whether we use the money management method directly in the code or modify the contract manually in live trading, At least on backtesting, We should not only do a Monte Carlo analysis for fixed one contract strategy, but also do further Monte Carlo analysis for strategy with money management. In order to understand the risk and control the risk.

To sum up, personally, I'm more inclined to think it's a bug.

As for other types of Monte Carlo analysis for individual strategy with MM method, I haven't gone into them. It may also need to be revised and optimized accordingly, But they're not as urgent as Monte Carlo trade manipulation.

Highly relevant task references. https://roadmap.strategyquant.com/tasks/sq4_9924 This is a Monte Carlo analysis of the portfolio with MM method feature request. I sincerely hope that the development team will seriously consider it again.

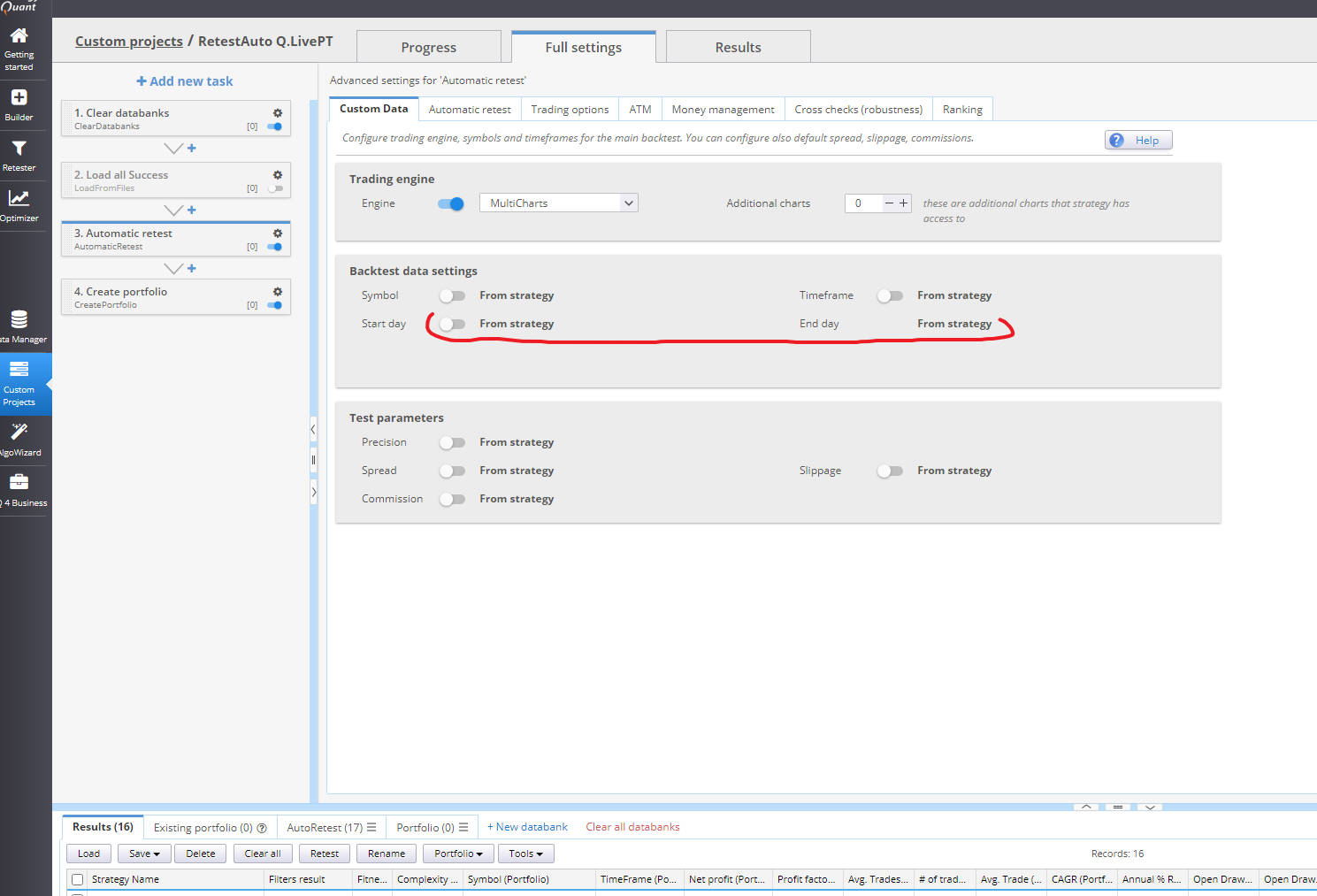

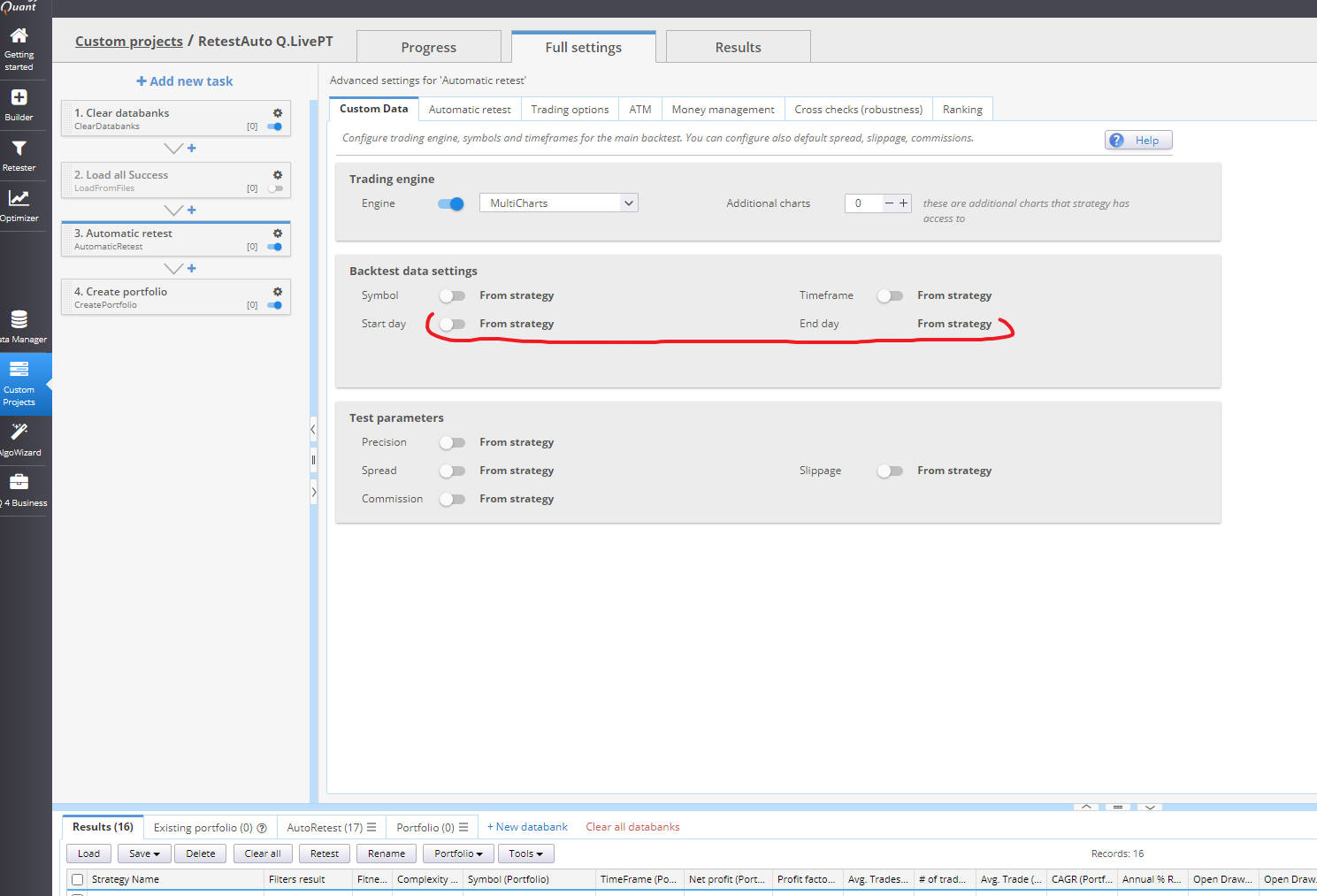

2.Another question :as shown in the attachment, in an Automatic retest task, If the default original strategy time range is used. Net profit in MC results and Net profit in databank are not same.

In fact, as you can see data setting attachment. I think the data setting in Automatic retest task should be strictly according to the time range of the original strategy(from strategy config),if we don't change any data setting, and the other setting option is according to the latest full sample data if we change data setting.

-

Votes +4

-

Project StrategyQuant X

-

Type Bug

-

Status New

-

Priority Normal

History

binhsir

18.02.2023 06:24

binhsir

18.02.2023 06:29Subject changed from Wrong statistical results on different levels of confidence when batch Monte Carlo trade manipulation analysis of individual strategies with money management. to Wrong statistical results on different levels of confidence when batch Monte Carlo trade manipulation analysis for individual strategies with money management.

binhsir

18.02.2023 10:48Description changed:

First of all,I want to start by stating the importance and high priority of this task. For trading based on volume and price time series strategies, developing robust strategies, constructing low correlation, diversified portfolios and implementing proper money and risk management are all essential.

as an aside, The automatic retest feature in custom project is great and will have unlimited potential. I like it.

Back to the topic:

1.This is somewhere between a bug and a feature. We need a Monte Carlo analysis of a strategy with money management. In fact, the software also objectively supports to set up Monte Carlo trade manipulation and MM method at the same time. Not only Retester but also Automatic retest task. But as you can see in attachment, we can see from the analysis results that Net Profit is same in any confidence interval.

My guess is that sq simply randomly changed the order of profit per trade . But it is meaningless to do so. Let me explain the theoretical basis, why do we need Monte Carlo trade manipulation analysis?

Because the market is cyclical, It could be a bull market or a bear market, high volatility and low volatility and others. We can't predict what will happen in the coming year.Therefore, when doing historical backtesting, we can check the robustness of the strategy by randomly changing the order of price quotations.When the strategy is to fix one contract, randomly changing the order of the profits per trade is close to randomly changing the order of the price quotes. But suppose we use money management,with the constant change of net profit, The number of contracts for every trade is constantly changing. It is inappropriate to directly modify the order of profit per trade at this time. The calculation logic should be to randomly modify the order of profit per contract and then implement the MM method over time. After 500 simulation tests,The net profit should be different in different confidence interval. Every other money management tool I've used has been like this. As you can see in the attached screenshot of one of the tools, MSA.

Whether we use the money management method directly in the code or modify the contract manually in live trading, At least on backtesting, We should not only do a Monte Carlo analysis of fixed one contract, but also do a Monte Carlo analysis with money management. In order to understand the risk and control the risk.

To sum up, personally, I'm more inclined to think it's a bug.

As for other types of Monte Carlo analysis for individual strategy with MM method, I haven't gone into them. It may also need to be revised and optimized accordingly, But they're not as urgent as trade manipulation.

Highly relevant task references. https://roadmap.strategyquant.com/tasks/sq4_9924 This is a Monte Carlo analysis of the portfolio with MM method feature request. I sincerely hope that the development team will seriously consider it again.

2.Another question :as shown in the attachment, in an Automatic retest task, If the default original strategy time range is used. Net profit in MC results and Net profit in databank are not same.

In fact, as you can see data setting attachment. I think the data setting in Automatic retest task should be strictly according to the time range of the original strategy(from strategy config),if we don't change any data setting, and the other setting option is according to the latest full sample data if we change data setting.

Attachment data setting in Atutomatic restest.jpg added

binhsir

18.02.2023 11:08Description changed:

First of all,I want to start by stating the importance and high priority of this task. For trading based on volume and price time series strategies, developing robust strategies, constructing low correlation, diversified portfolios and implementing proper money and risk management are all essential.

as an aside, The automatic retest feature in custom project is great and will have unlimited potential. I like it.

Back to the topic:

1.This is somewhere between a bug and a feature. We need a Monte Carlo analysis of a strategy with money management. In fact, the software also objectively support to set up Monte Carlo trade manipulation and MM method at the same time. Not only Retester but also Automatic retest task. But as you can see in attachment, we can see from the analysis results that Net Profit is same in any confidence interval.

My guess is that sq simply randomly changed the order of profit per trade . But it is meaningless to do so. Let me explain the theoretical basis, why do we need Monte Carlo trade manipulation analysis?

Because the market is cyclical, It could be a bull market or a bear market, high volatility and low volatility and others. We can't predict what will happen in the coming year.Therefore, when doing historical backtesting, we can check the robustness of the strategy by randomly changing the order of price quotations.When the strategy is to fixed one contract, randomly changing the order of the profits per trade is close to randomly changing the order of the price quotes. But suppose we use money management,with the constant change of net profit, The number of contracts for every trade is constantly changing. It is inappropriate to directly modify the order of profit per trade at this time. The calculation logic should be to randomly modify the order of profit per contract and then implement the MM method over time. After 500 simulation tests,The net profit should be different in different confidence interval. Every other money management tool I've used has been like this. As you can see in the attached screenshot of one of the tools, MSA.

Whether we use the money management method directly in the code or modify the contract manually in live trading, At least on backtesting, We should not only do a Monte Carlo analysis of fixed one contract, but also do a Monte Carlo analysis with money management. In order to understand the risk and control the risk.

To sum up, personally, I'm more inclined to think it's a bug.

As for other types of Monte Carlo analysis for individual strategy with MM method, I haven't gone into them. It may also need to be revised and optimized accordingly, But they're not as urgent as trade manipulation.

Highly relevant task references. https://roadmap.strategyquant.com/tasks/sq4_9924 This is a Monte Carlo analysis of the portfolio with MM method feature request. I sincerely hope that the development team will seriously consider it again.

2.Another question :as shown in the attachment, in an Automatic retest task, If the default original strategy time range is used. Net profit in MC results and Net profit in databank are not same.

In fact, as you can see data setting attachment. I think the data setting in Automatic retest task should be strictly according to the time range of the original strategy(from strategy config),if we don't change any data setting, and the other setting option is according to the latest full sample data if we change data setting.

binhsir

18.02.2023 11:16Description changed:

First of all,I want to start by stating the importance and high priority of this task. For trading based on volume and price time series strategies, developing robust strategies, constructing low correlation, diversified portfolios and implementing proper money and risk management are all essential.

as an aside, The automatic retest feature in custom project is great and will have unlimited potential. I like it.

Back to the topic:

1.This is somewhere between a bug and a feature. We need a Monte Carlo analysis of a strategy with money management. In fact, the software also objectively support to set up Monte Carlo trade manipulation and MM method at the same time. Not only Retester but also Automatic retest task. But as you can see in attachment, we can see from the analysis results that Net Profit is same in any confidence interval.

My guess is that sq simply randomly changed the order of profit per trade . But it is meaningless to do so. Let me explain the theoretical basis, why do we need Monte Carlo trade manipulation analysis?

Because the market is cyclical, It could be a bull market or a bear market, high volatility and low volatility and others. We can't predict what will happen in the coming year.Therefore, when doing historical backtesting, we can check the robustness of the strategy by randomly changing the order of price quotations.When the strategy is to fixed one contract, randomly changing the order of the profits per trade is close effect to randomly changing the order of the price quotes. But suppose we use money management,with the constant change of net profit, The number of contracts for every trade is constantly changing. It is inappropriate to directly modify the order of profit per trade at this time. The calculation logic should be to randomly modify the order of profit per contract and then implement the MM method over time. For example, after 500 simulation tests,The net profit should be different in every confidence interval. Every other money management tool I've used has been done like i said. For example, as you can see in the attached screenshot of one of the tools, MSA.

Whether we use the money management method directly in the code or modify the contract manually in live trading, At least on backtesting, We should not only do a Monte Carlo analysis for fixed one contract strategy, but also do further Monte Carlo analysis for strategy with money management. In order to understand the risk and control the risk.

To sum up, personally, I'm more inclined to think it's a bug.

As for other types of Monte Carlo analysis for individual strategy with MM method, I haven't gone into them. It may also need to be revised and optimized accordingly, But they're not as urgent as Monte Carlo trade manipulation.

Highly relevant task references. https://roadmap.strategyquant.com/tasks/sq4_9924 This is a Monte Carlo analysis of the portfolio with MM method feature request. I sincerely hope that the development team will seriously consider it again.

2.Another question :as shown in the attachment, in an Automatic retest task, If the default original strategy time range is used. Net profit in MC results and Net profit in databank are not same.

In fact, as you can see data setting attachment. I think the data setting in Automatic retest task should be strictly according to the time range of the original strategy(from strategy config),if we don't change any data setting, and the other setting option is according to the latest full sample data if we change data setting.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}