Backtest results inaccurate

Hi Strategy Quant/Algo wizard team,

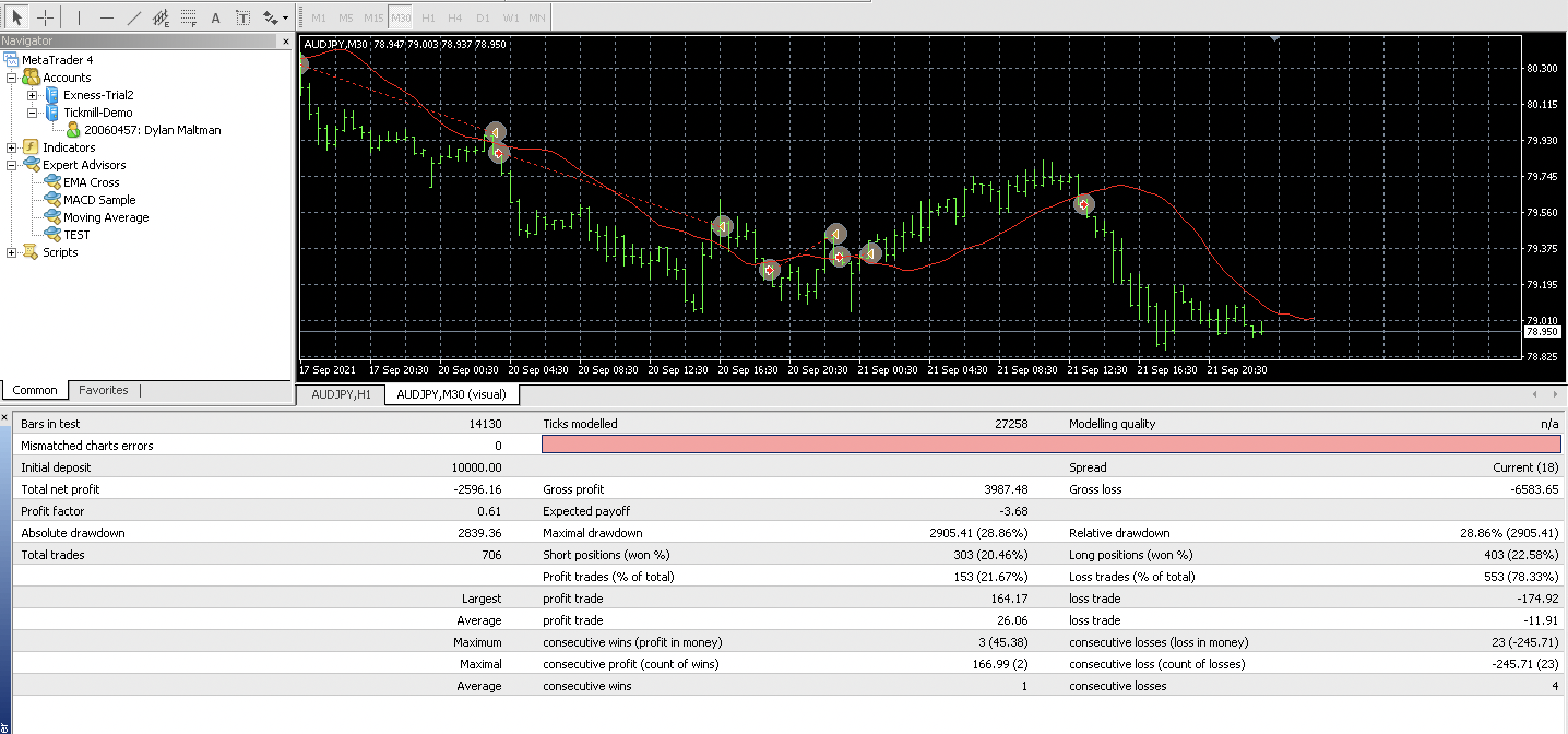

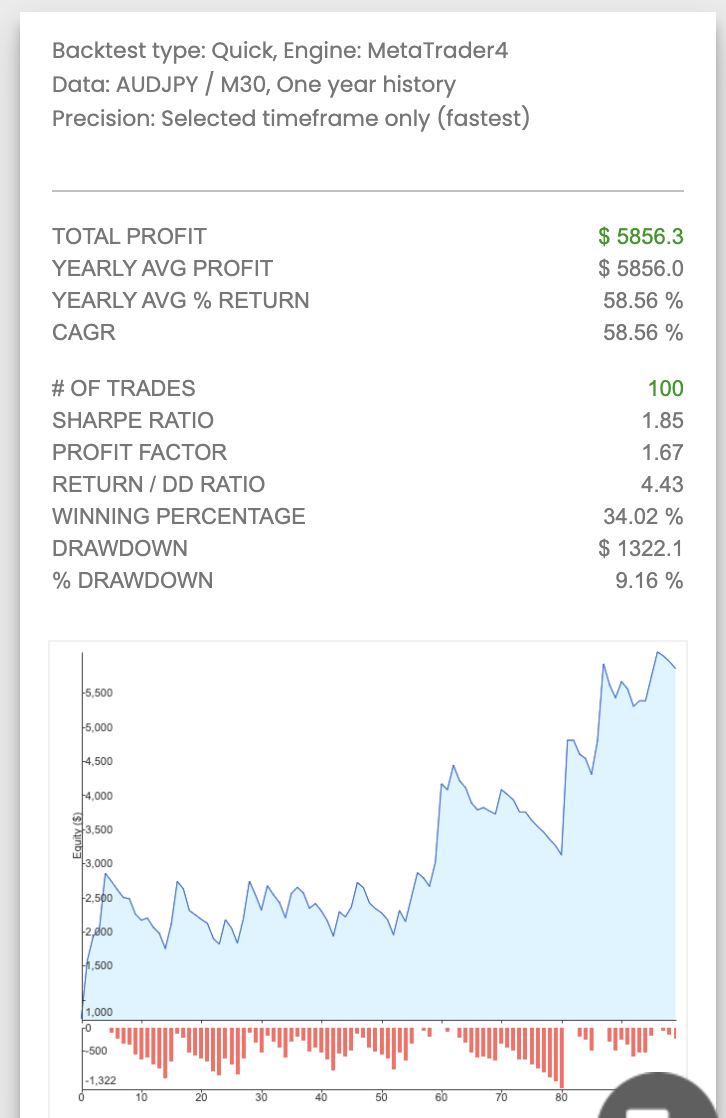

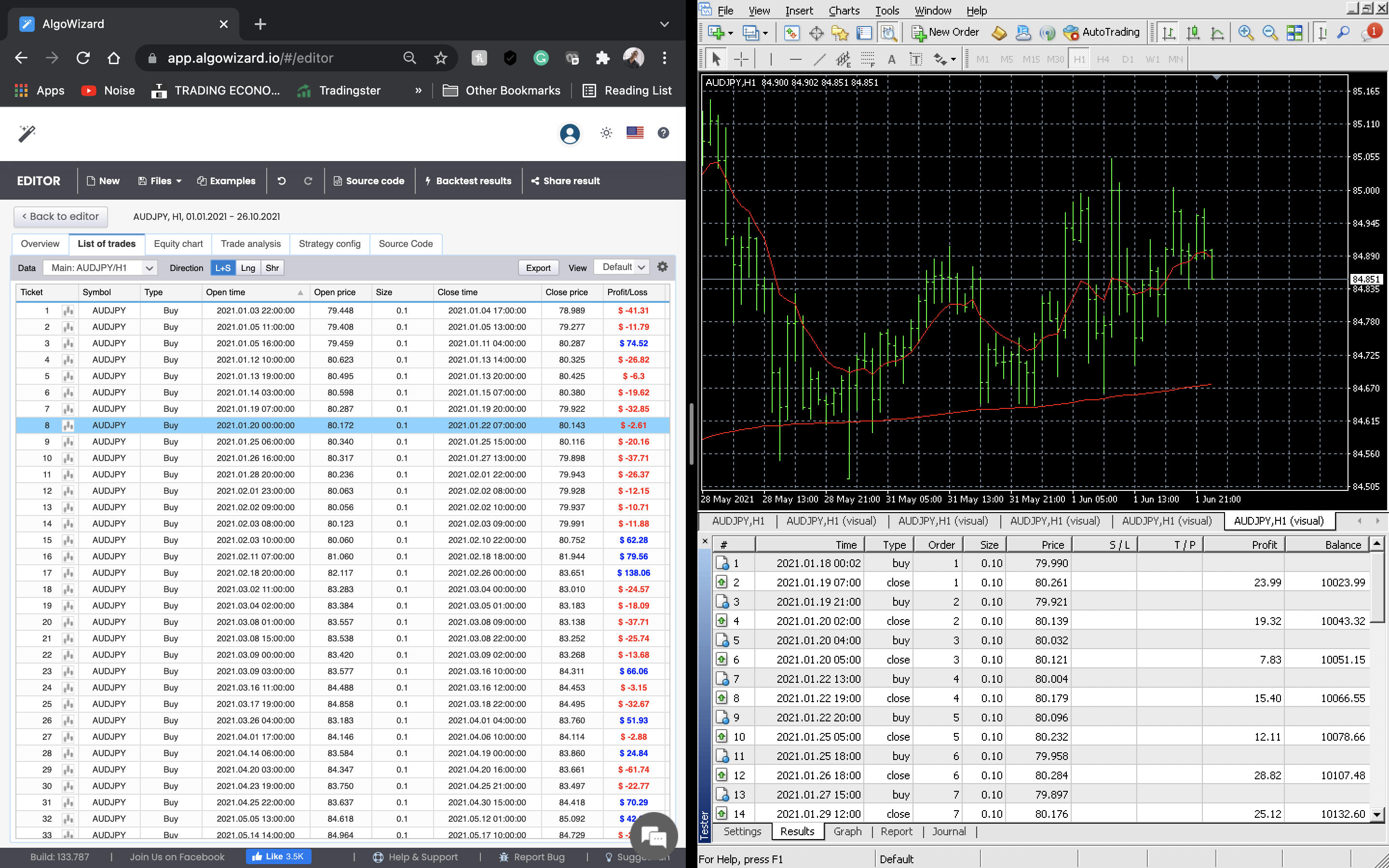

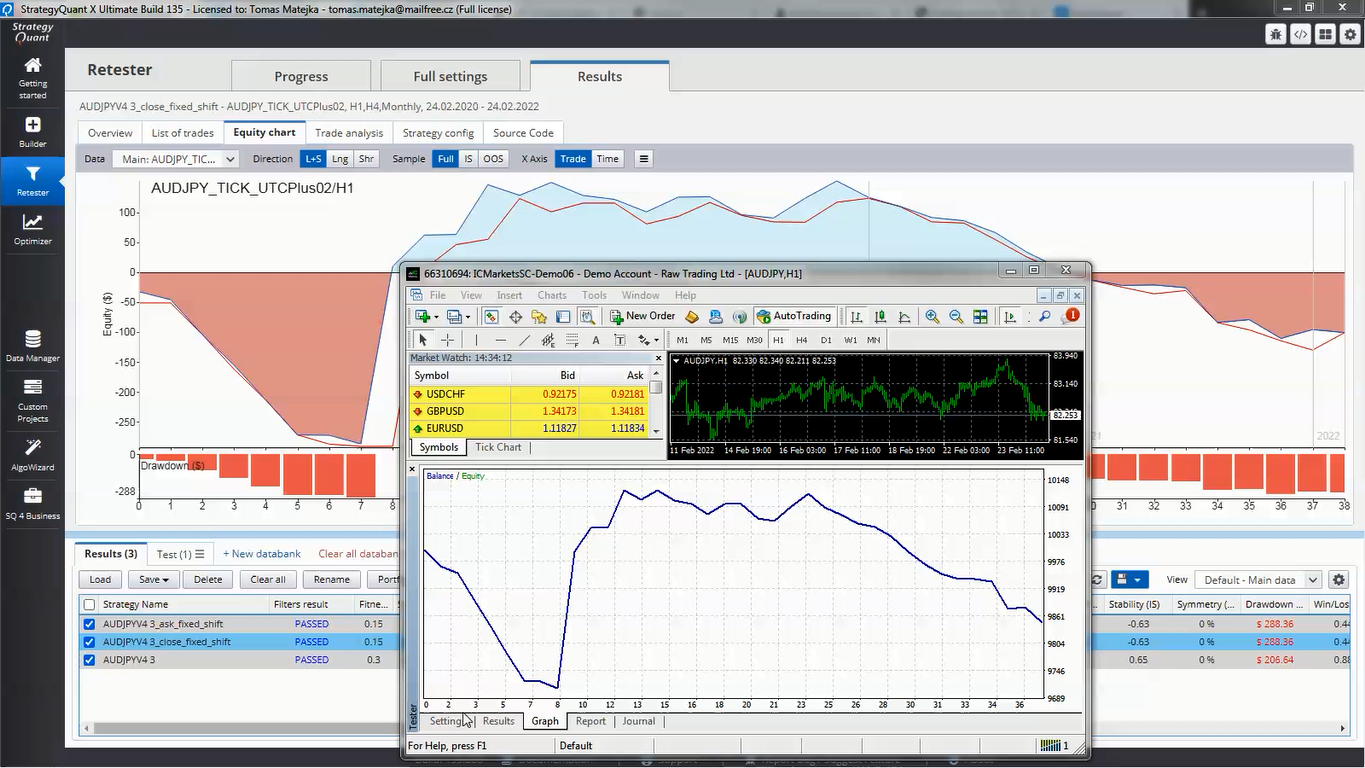

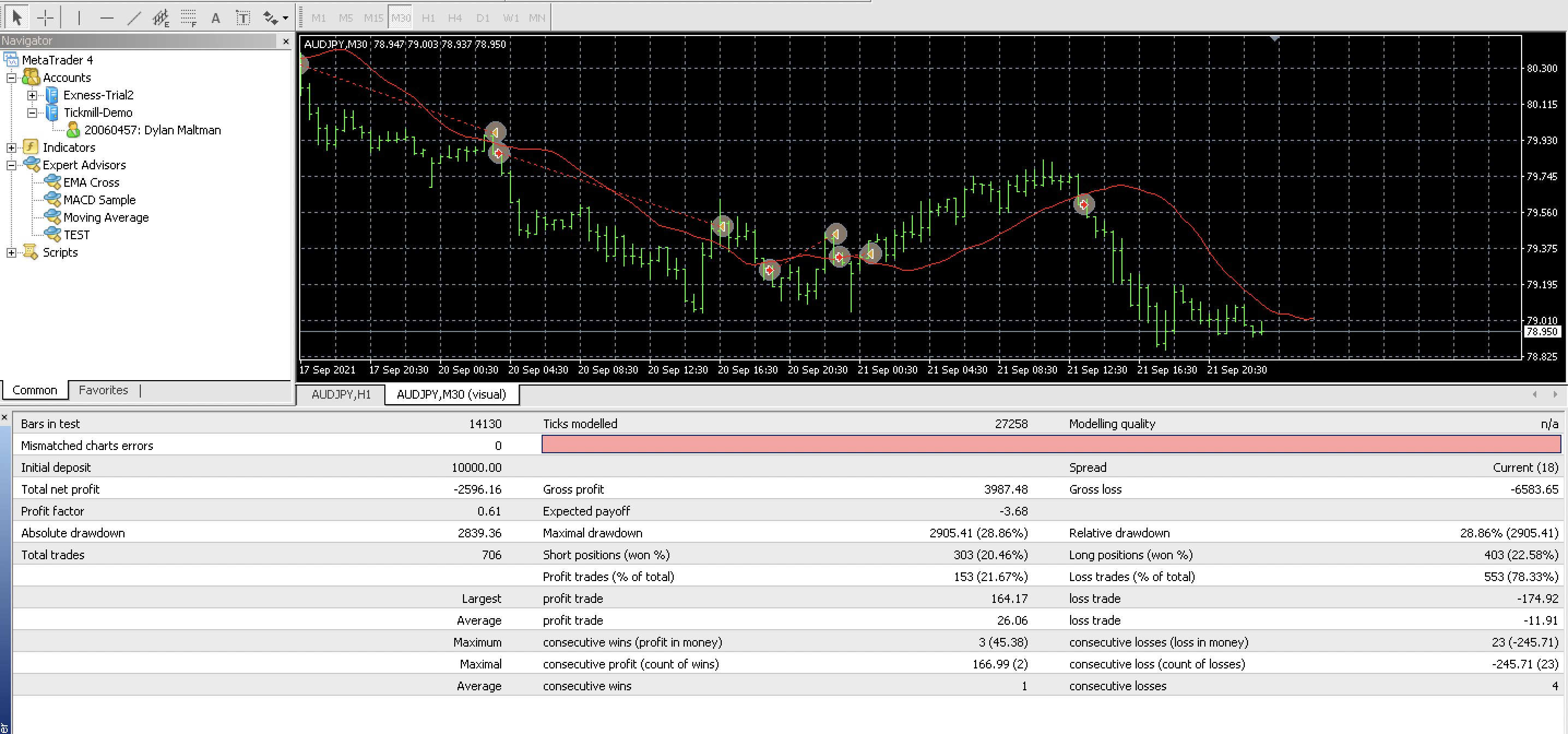

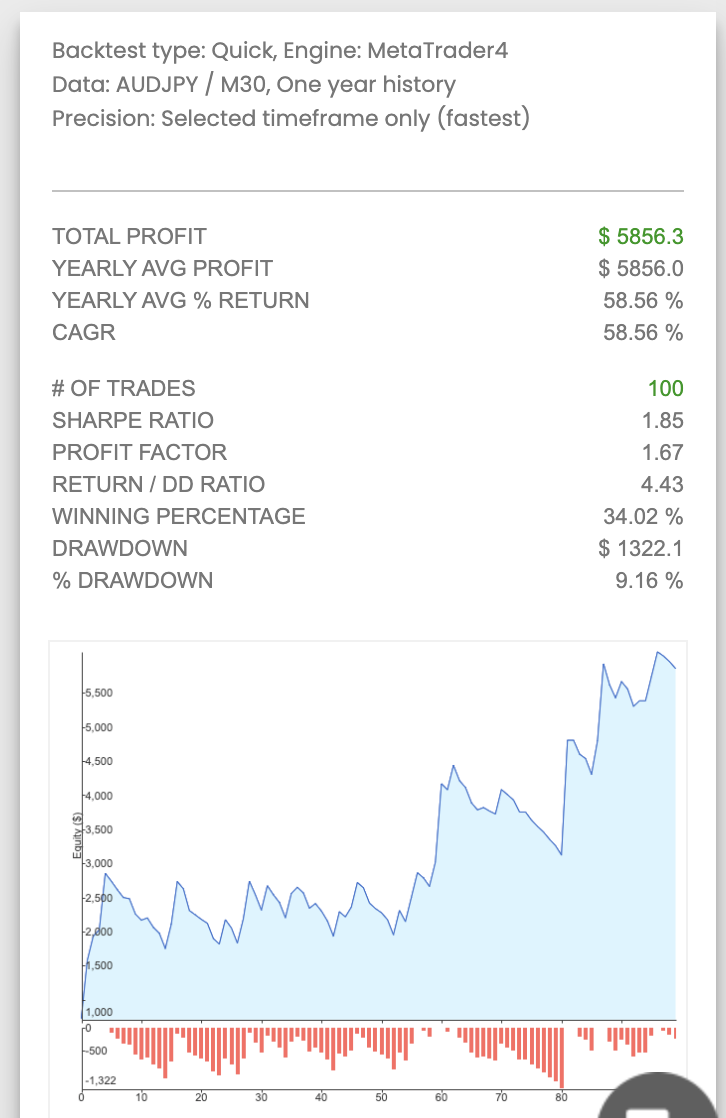

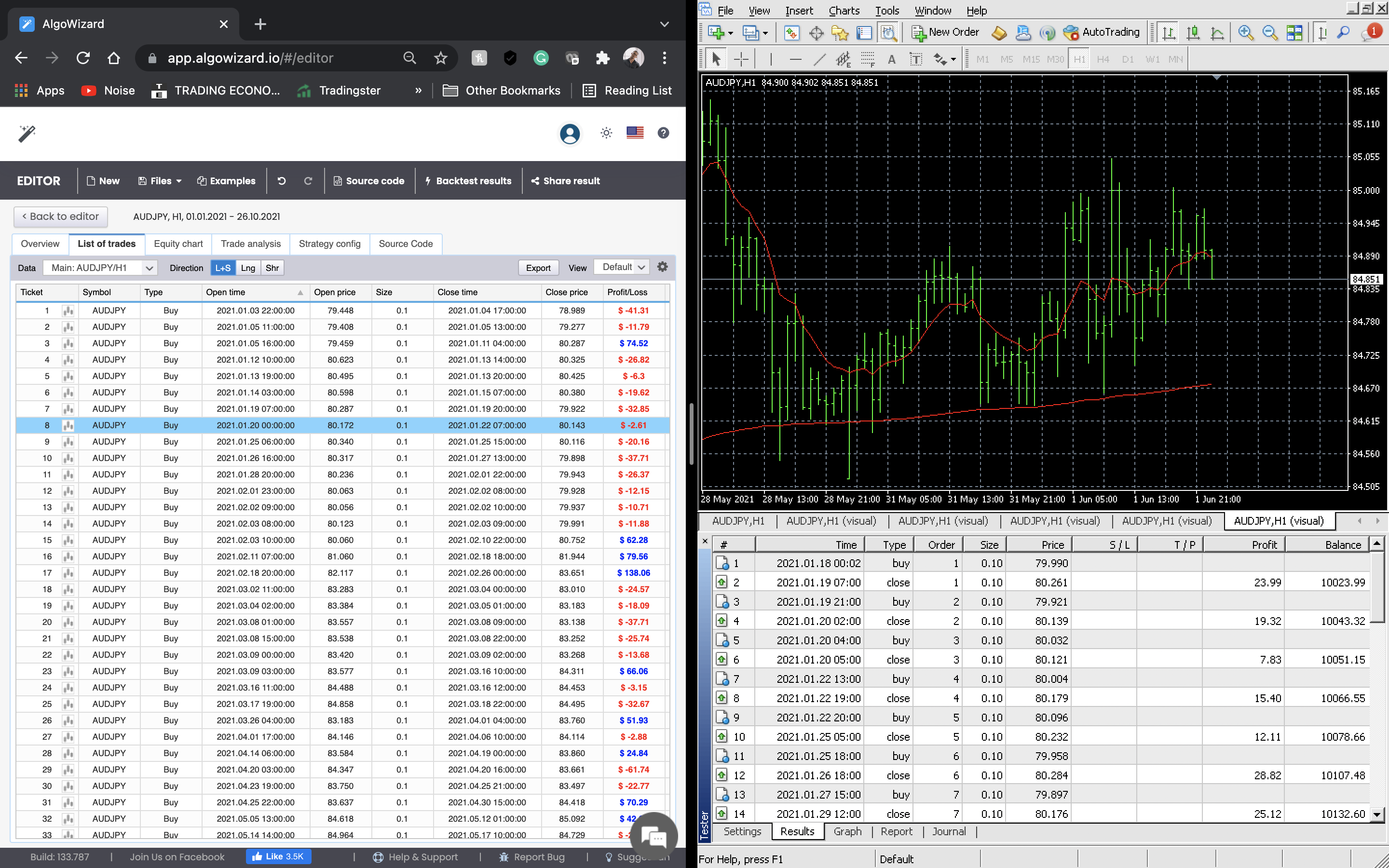

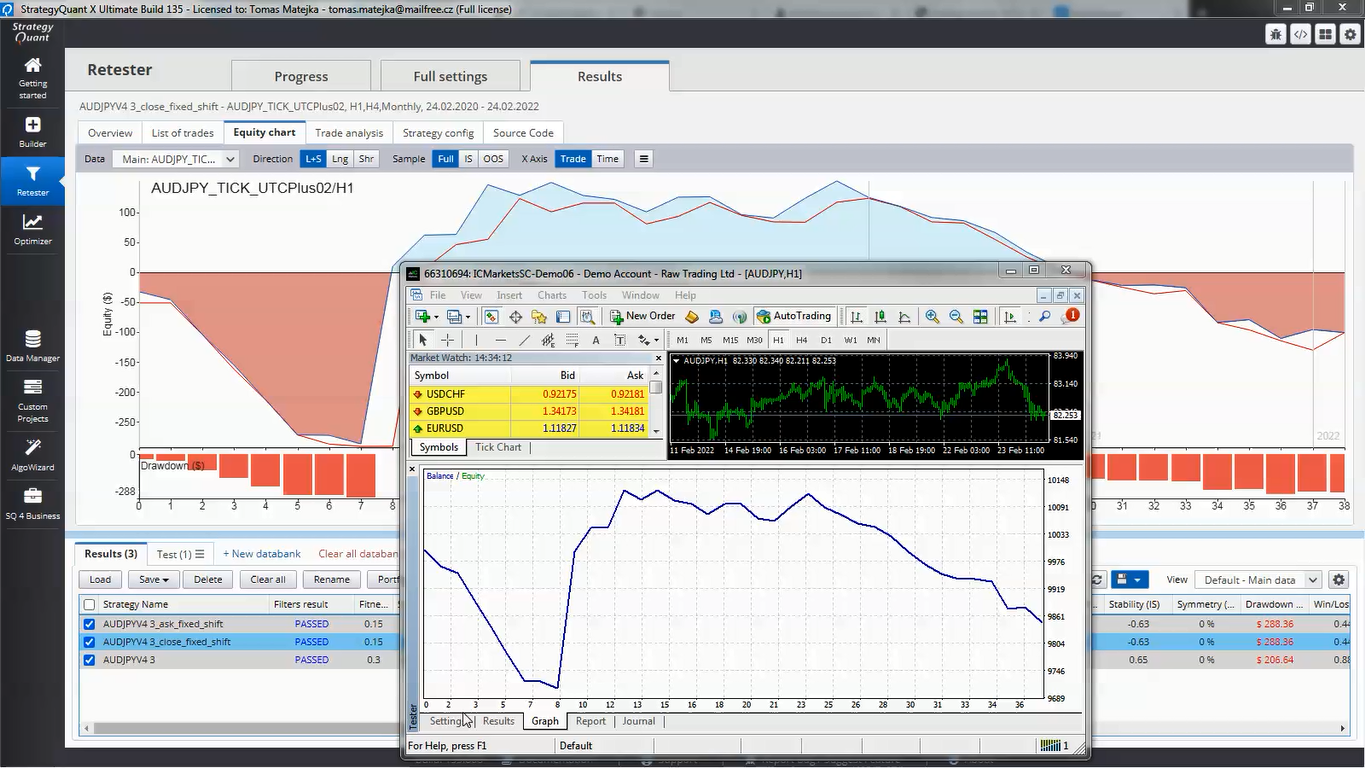

Across all the strategies that have been created, backtest results significantly differ from Mt4 backtest results (see screenshots attached). Backtests have been conducted between brokers and on Mt4's data itself. Why is this?

-

Votes +2

-

Project AlgoWizard

-

Type Bug

-

Status Fixed

-

Priority Normal

History

tmatejka.

24.02.2022 20:34

We have checked the strategy with developers and found out discprepancies in the results your reported have been likely caused by the fact you use the shift = 0 in your entry and exit conditions together with low backtest precision in AlgoWizard together with conditions setup such as:

1) when using Ask in the input conditions the strategy can be sensitive to broker data -> better option is to use Close [0] or rather Close [1] when tick data backtest is not available

2) the strategy uses a large shift (200) along with a large EMA period (250). It takes quite a long history before the backtest begins, so that the values can stabilize

3) to backtest the strategy properly real tick data is required but it is not available in the AlgoWizard platform (only the StrategyQuantX)

When I modified your strategy to use the shift = 1 in all conditions though the backtest match pretty good between SQ and MT4 using real tick data shifted to UTC + 2 timezone

So to sum up: due to relatively low backtest precision available in the online AlgoWizard platform you need to be careful about the strategy logic and whether it is viable and realistic

dylanmaltman

28.02.2022 13:09Thank you for the feedback. With reference to point 2, do the indicators effectively start from scratch until such time that there is enough data to create the indicator (e.g. 250 ema requires 250 data points from the start of the backtest until the indicator is generated)?

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}