Filter for accumulatted retdd of portfolio

Let's say i want to save into databank portfolio with retdd at least 10 and stategies which I have in databank have retdd least 5.

The problem is that not always 2 combined strategies (even if their correlation is lower than 0,4) give better accumulated retdd results than both of them have separately.

Check the example below

1) Two strategies give better retdd in portfolio that they have separately (that's a good portfolio)

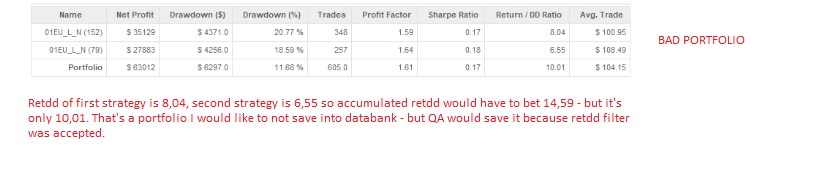

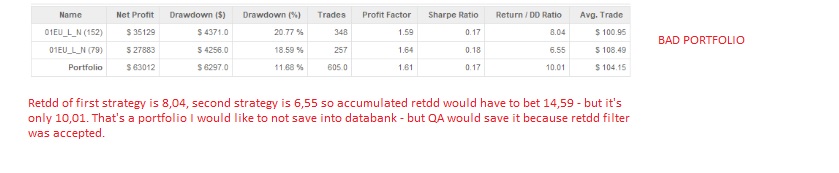

2) Two strategies give worse retdd that they separately - however they still would be save into databank because they reach desired retdd set in filters. That's a bad portfolio.

The idea is:

-save into databank only portofolios where accumulated result is only better that separeted strategies which are used to build that portfolio.

Second idea is to set an acceptable deviation (like 10 or 20%) for portolio even if the accumulated retdd is worse. So let's say I have 2 strategies with retdd 5 but I would like to

save intodatabank portolios where accumulated retdd is not worse than 90% of two retdd from strategies combined.

So: You have stategies with retdd 8 and retdd 12. Combined retdd would be 20 - but we allowed 10% deviation which means we would accept portofolio with retdd at least 18 for these 2

The problem is that not always 2 combined strategies (even if their correlation is lower than 0,4) give better accumulated retdd results than both of them have separately.

Check the example below

1) Two strategies give better retdd in portfolio that they have separately (that's a good portfolio)

2) Two strategies give worse retdd that they separately - however they still would be save into databank because they reach desired retdd set in filters. That's a bad portfolio.

The idea is:

-save into databank only portofolios where accumulated result is only better that separeted strategies which are used to build that portfolio.

Second idea is to set an acceptable deviation (like 10 or 20%) for portolio even if the accumulated retdd is worse. So let's say I have 2 strategies with retdd 5 but I would like to

save intodatabank portolios where accumulated retdd is not worse than 90% of two retdd from strategies combined.

So: You have stategies with retdd 8 and retdd 12. Combined retdd would be 20 - but we allowed 10% deviation which means we would accept portofolio with retdd at least 18 for these 2

strategies.

Please check attached screens with examples.

-

Votes +2

-

Project QuantAnalyzer

-

Type Feature

-

Status New

-

Priority Low

History

Votes: +2

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}