Wrong MC simulation of MT4 imported results

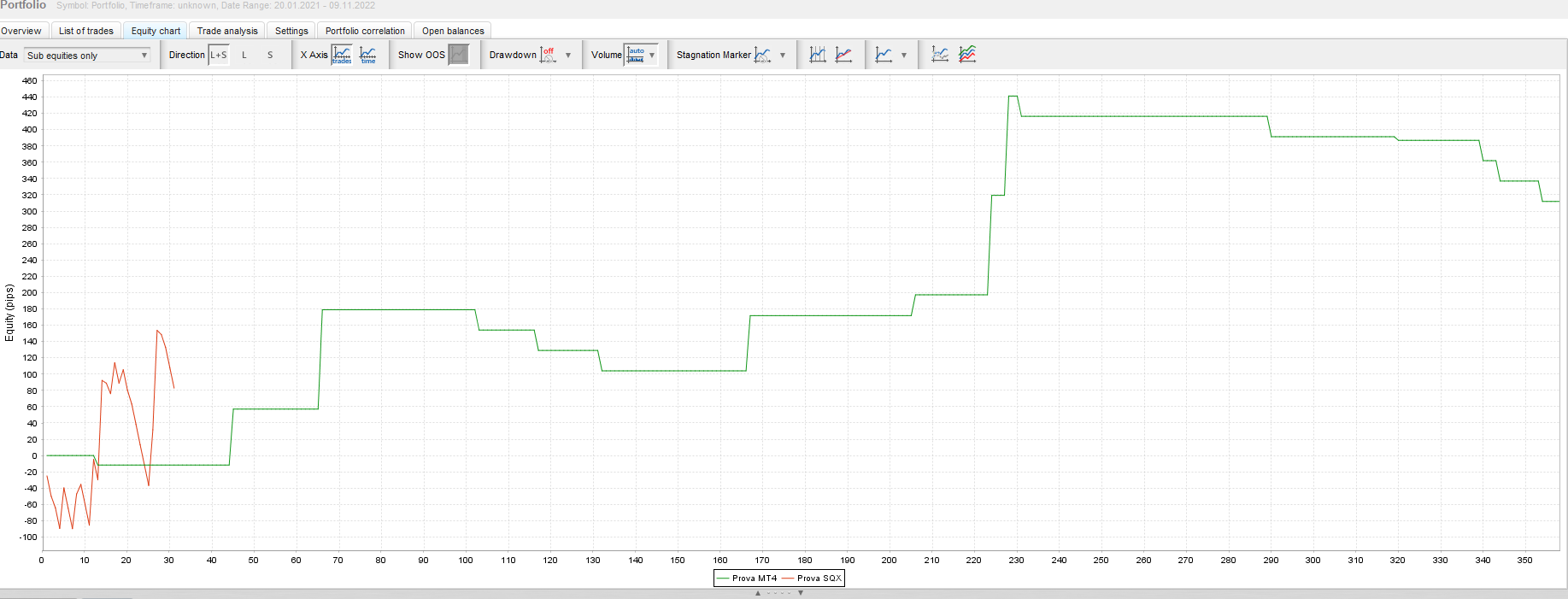

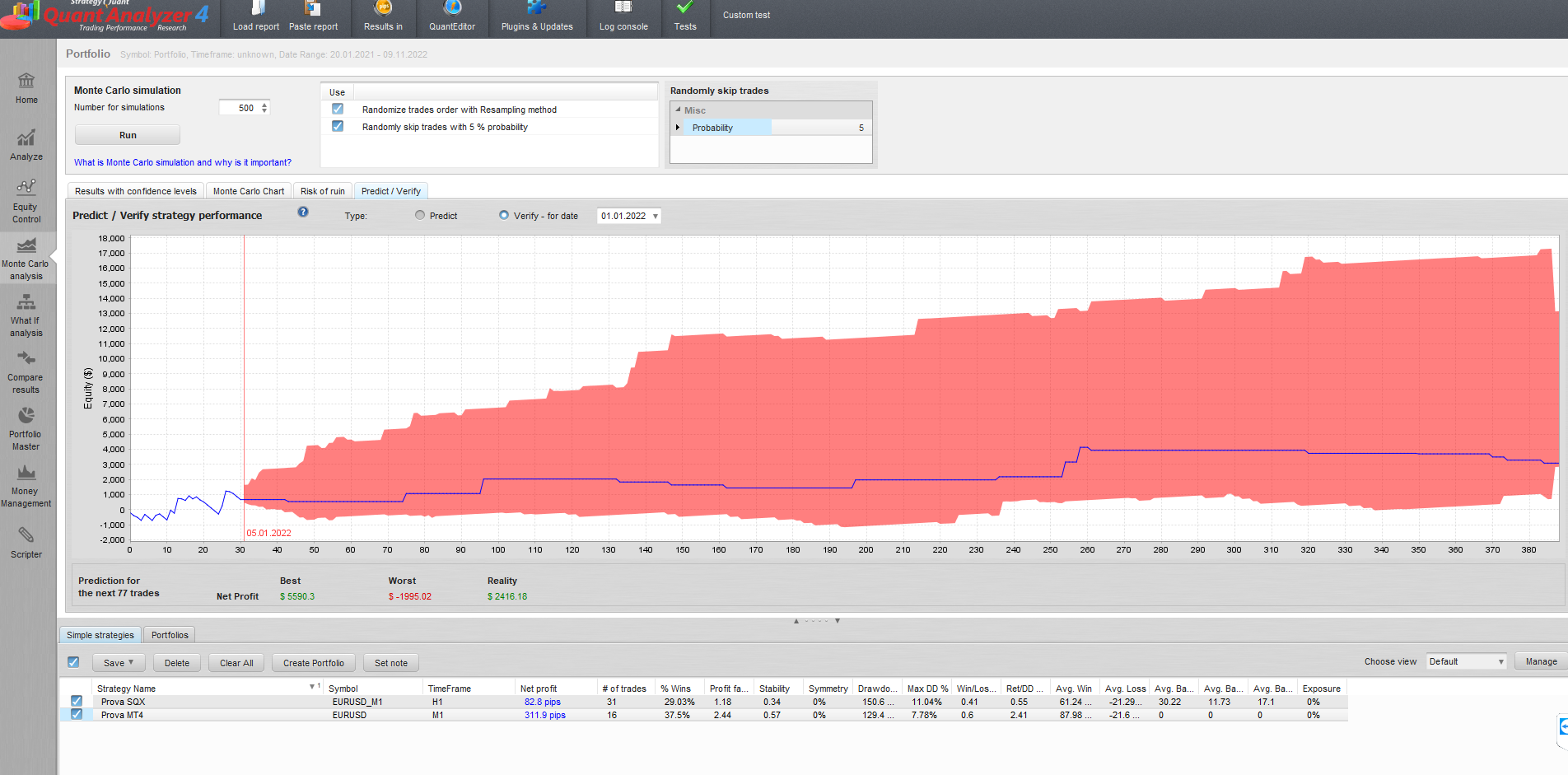

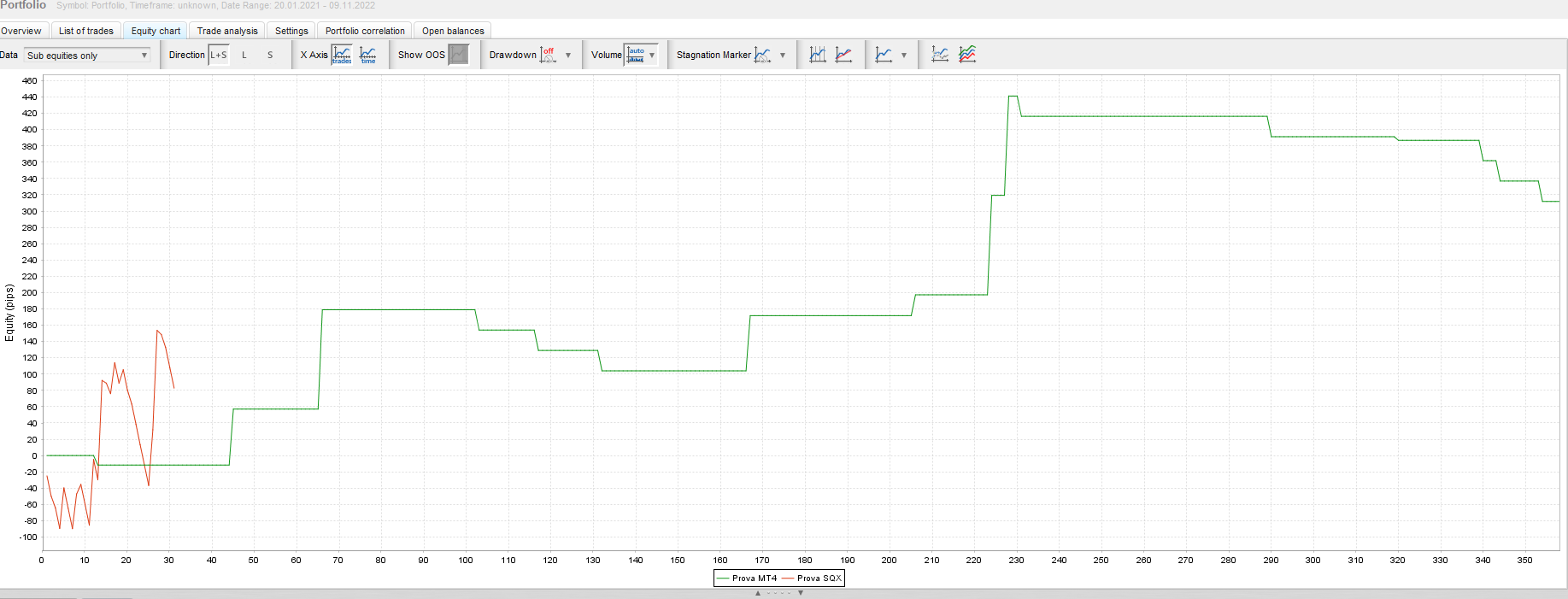

In the attached example, only the 31 trades (which are the part of portfolio which is related to the sqx simulation) should be used to project the remaining 16 (which are related to the MT4 imported data).

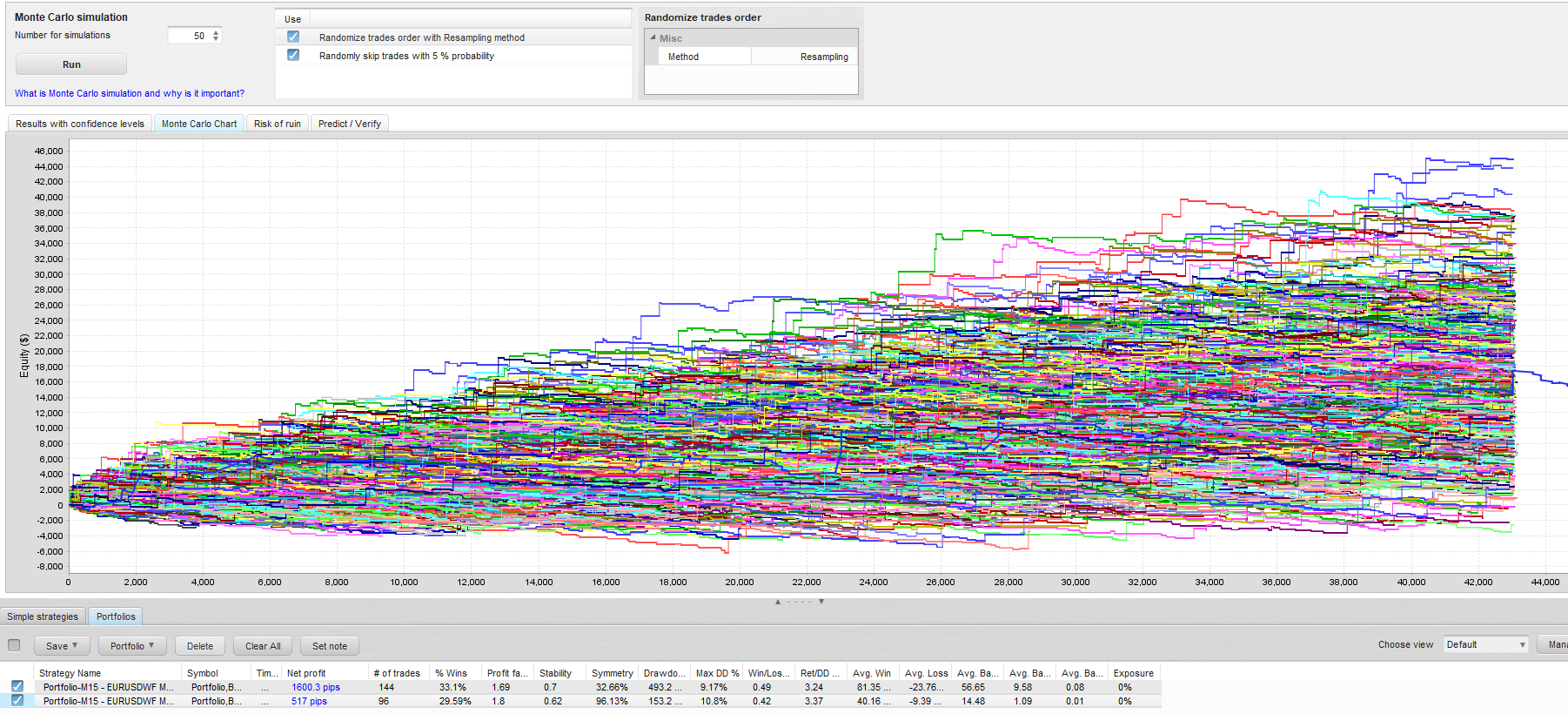

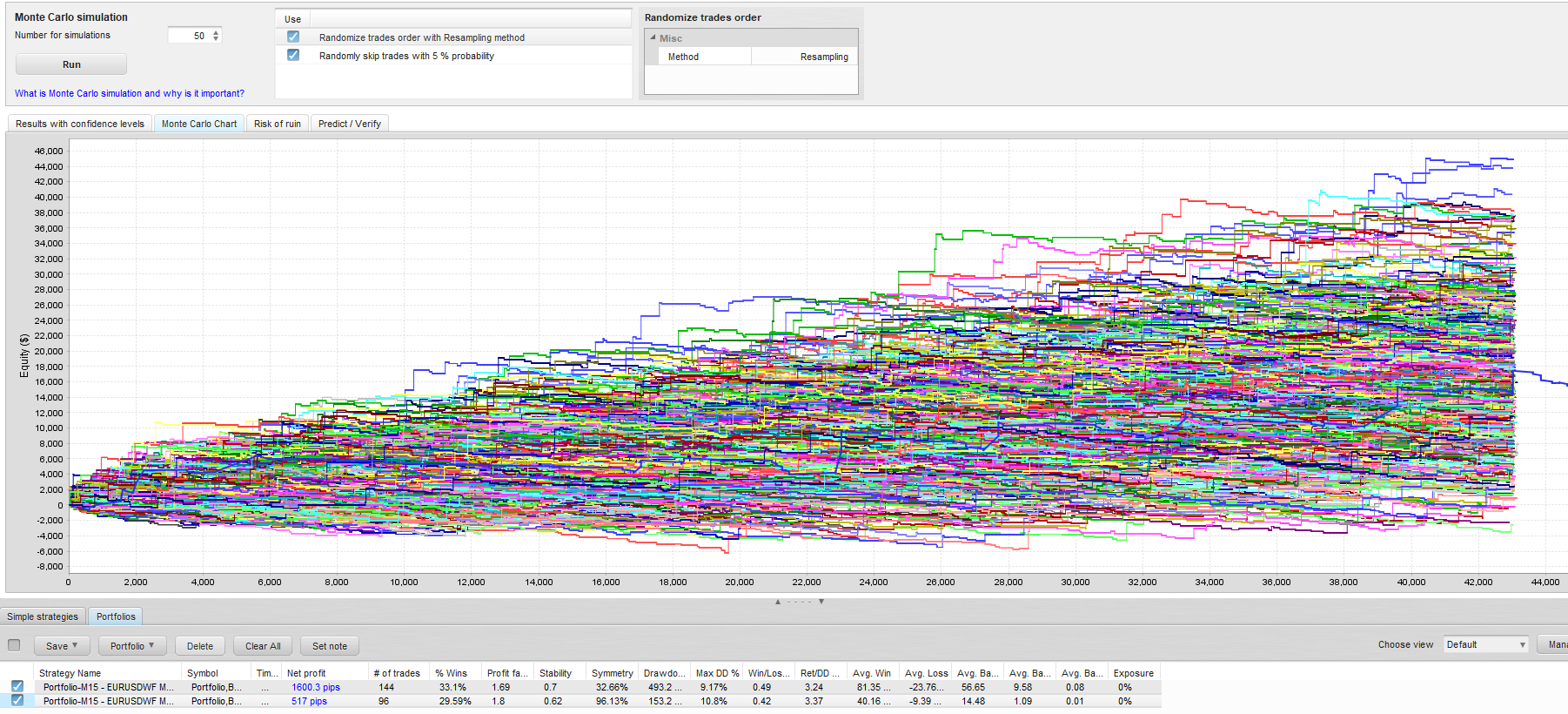

Instead, it seems that more than 300 trades are being simulated.

In my opinion, it would be better to filter the dummy trades directly during the import process , in order to avoid also issues when comparing strategy results in the equity charts using the trade number scale instead of the time scale.

-

Votes 0

-

Project QuantAnalyzer

-

Type Bug

-

Status New

-

Priority Low

History

mscapin95

22.11.2022 18:04Attachment Immagine 2022-11-22 175413.png added

Attachment M15 - EURUSDWF Matrix - Strategy 23119.sqx added

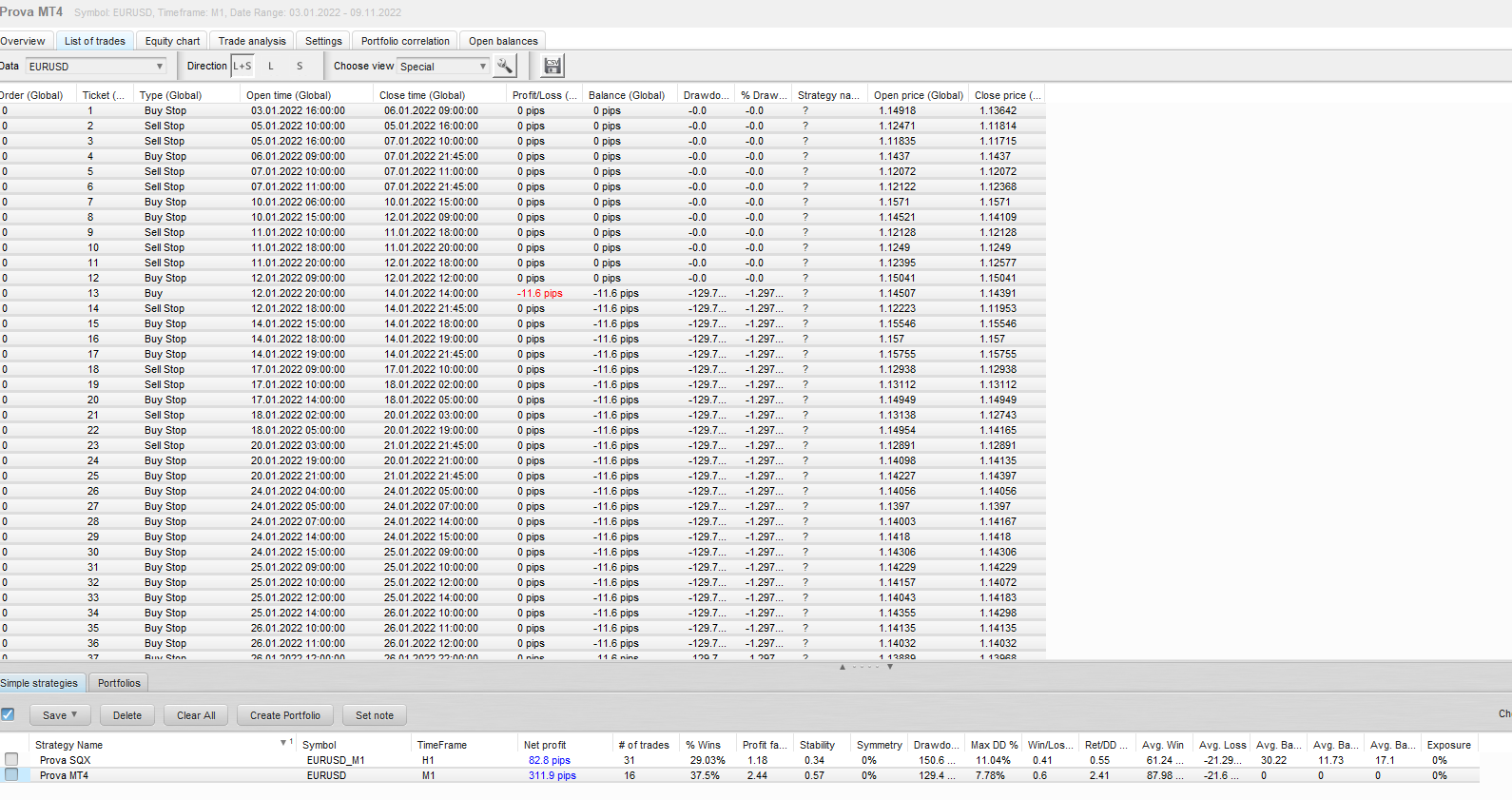

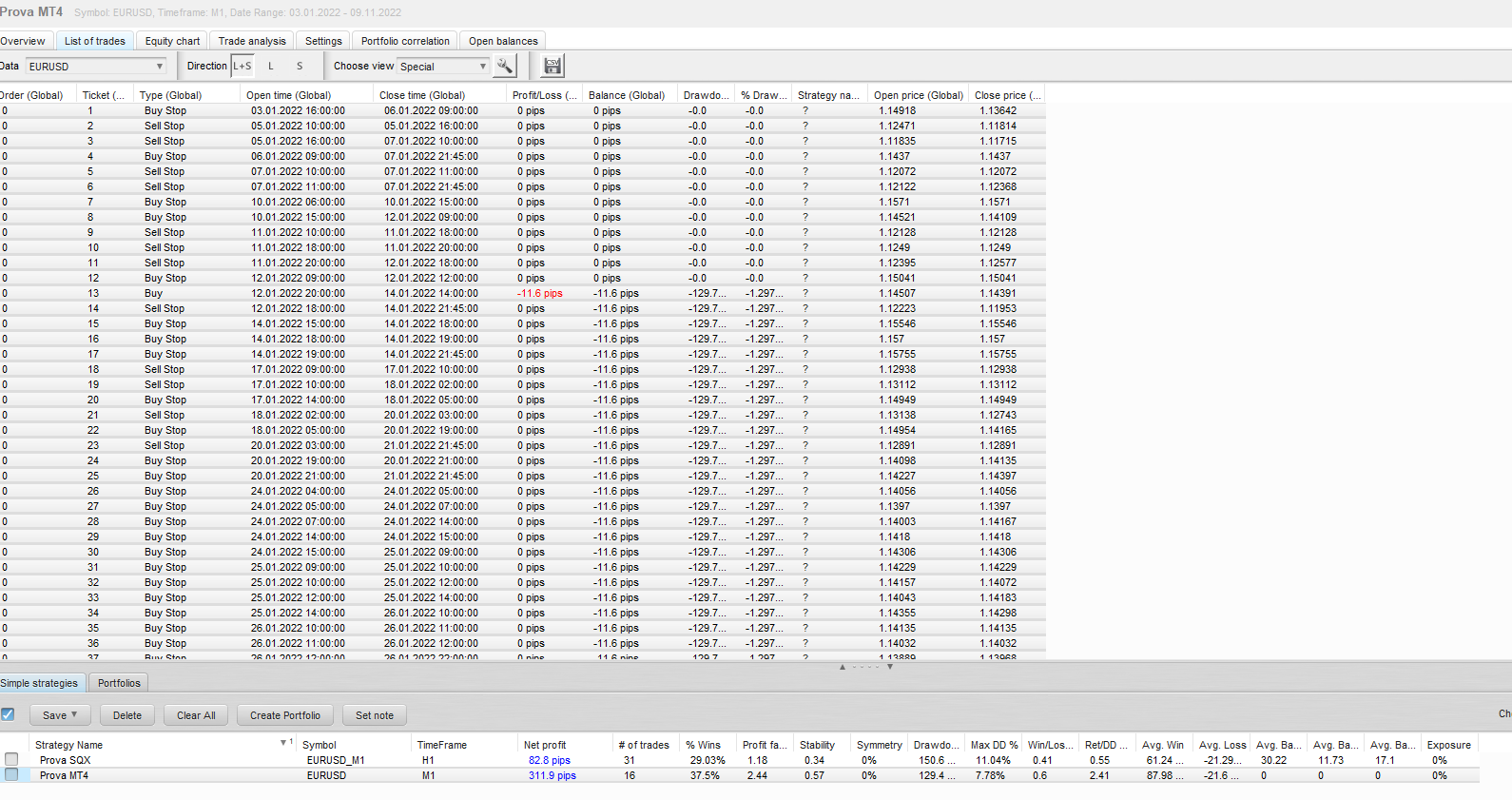

This pending orders are loaded by QA, and then simulated as real trades :-(

BtW, QA gets hung in the process and you have to kill and restart it

All pending orders should be filtered in the import process.

mscapin95

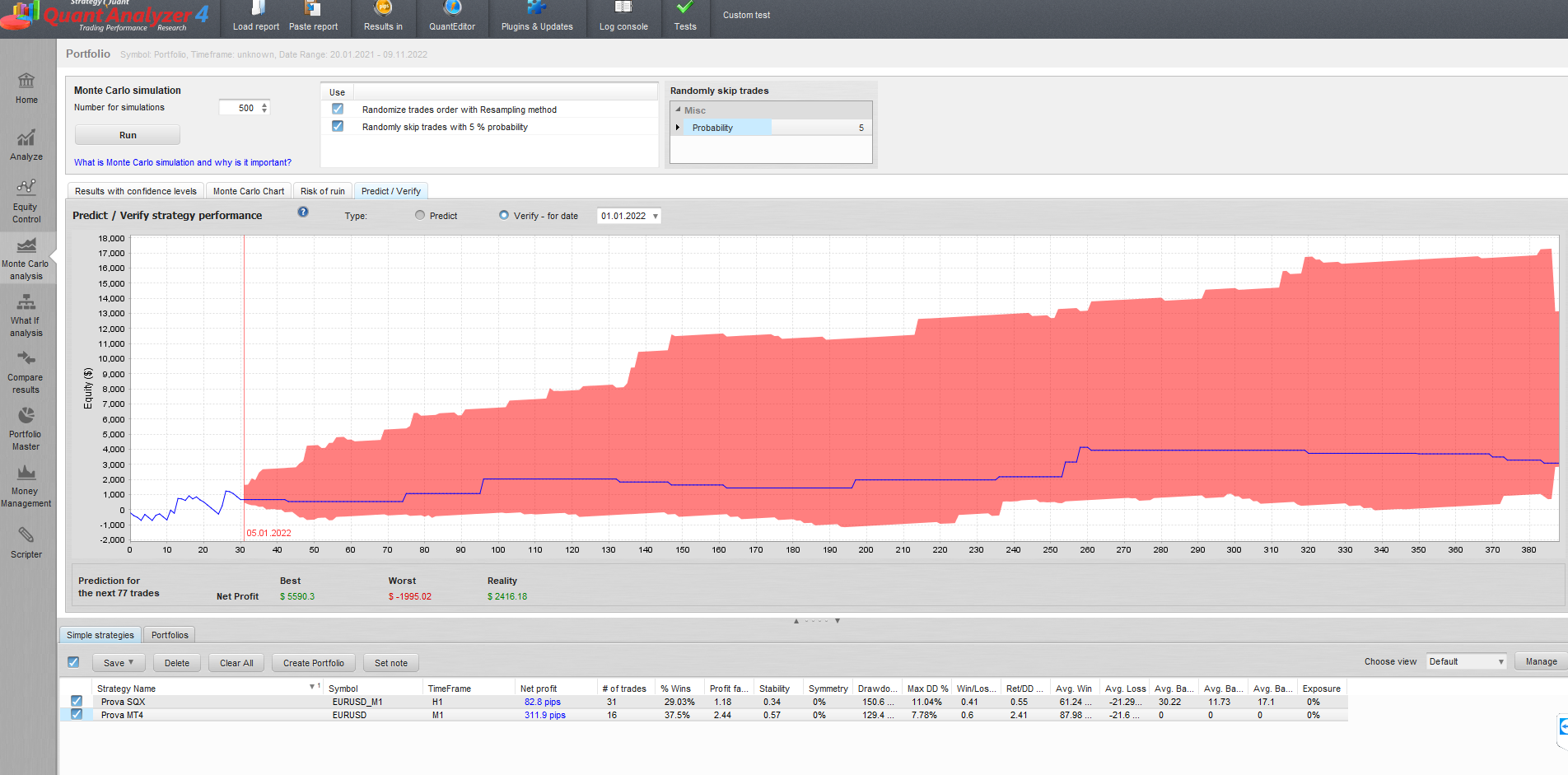

23.11.2022 10:54Nevertheless, the problems of considering all trades for the "VERIFY" option still remains.

In fact, the main use of this option should be to check if the live results are consistent with the past simulated results, and of course this is not possible if also the live results themselves are used for the simulation!

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

I believe that for the "VERIFY" option only trades BEFORE the reference date should be used for the MC simulation, while all past trades should be used for the "PREDICT" option only.

Moreover, for the "PREDICT" option it should be possible to chose the number of future trades to predict (if there is a way to configure this I did not find it)