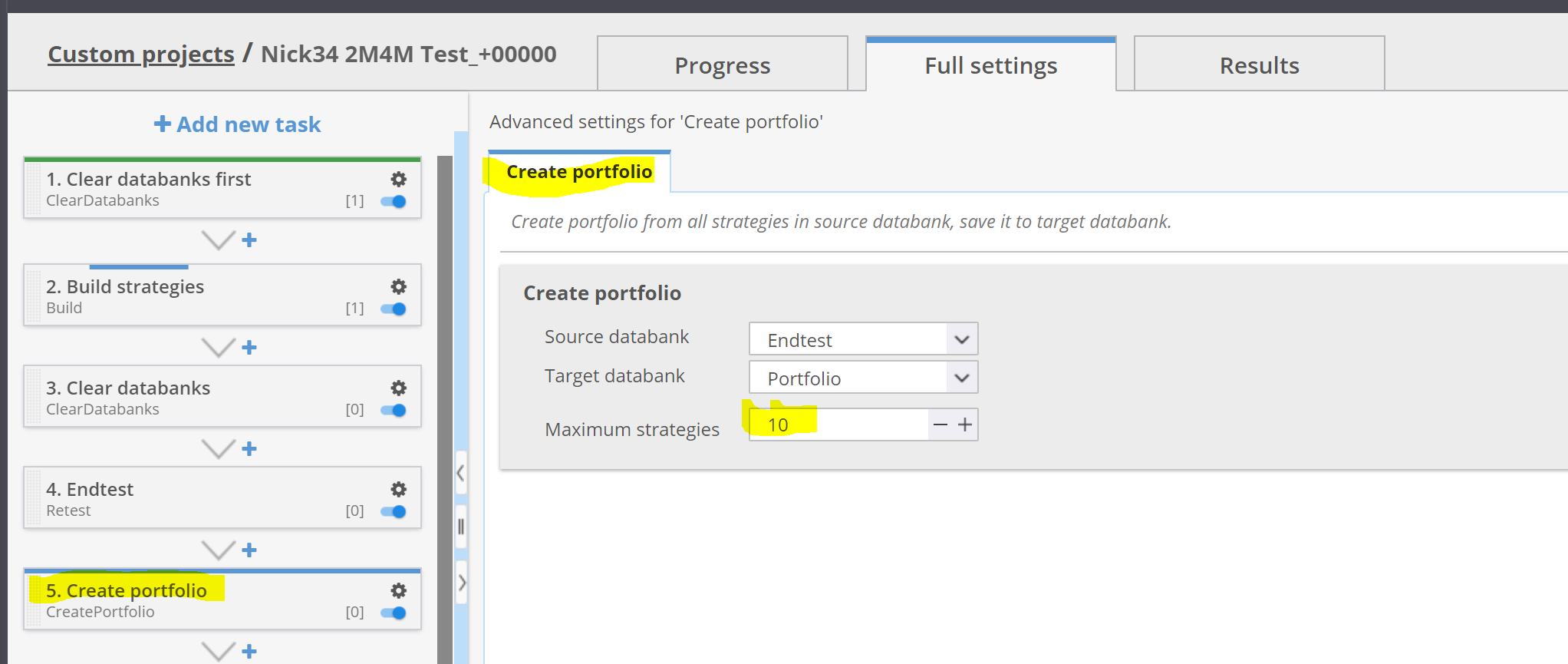

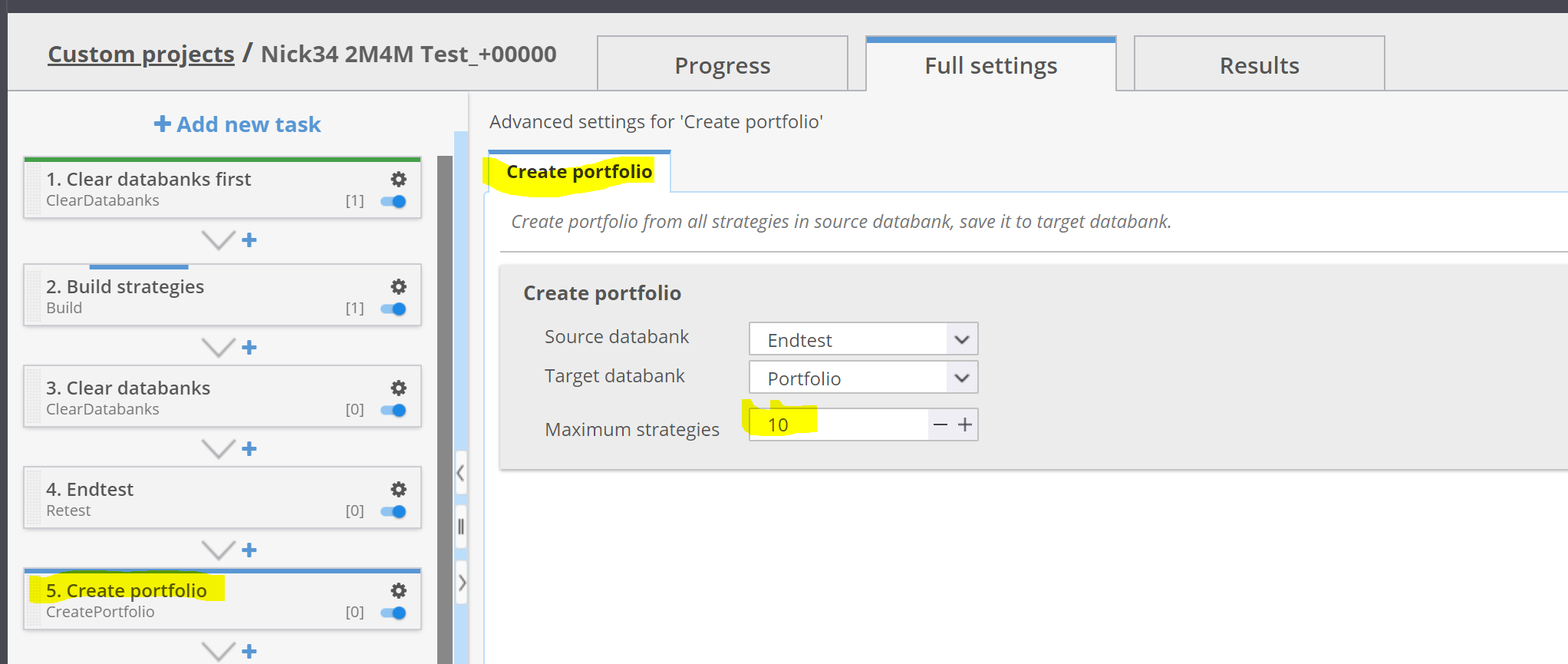

SQ 4.138 Create Portfolio of N strategies with Fitness Function

The create portfolio function takes x strategies from the set N of strategies found and builds a portfolio from them.

This x can be chosen arbitrarily.

I use this function to analyze generated strategies. This makes it easy to judge how good the strategies generated are.

The problem with this function at the moment is that random strategies are chosen from the set N of strategies found. But when building portfolios, I want to build “good” portfolios. It would be very helpful here not to simply select random strategies, but rather the best x of N strategies based on a fitness function.

-

Votes 0

-

Project StrategyQuant X

-

Type Feature

-

Status New

-

Priority Normal

History

Votes: 0

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}