[115] Follow up on "strange" "Default" values in "Building Blocks"

I´ve just downloaded Build 115 and see that you´ve implemented most of my suggested changes for the "Default" values on most "Building Blocks". However, there are still some that you did not seem to have followed / haven´t been changed and I wanted to highlight these because some of these still prevent these indicators from being used "meaningful" in strategy building with their current "Default" values. So here is my "what still needs to be changed" list:

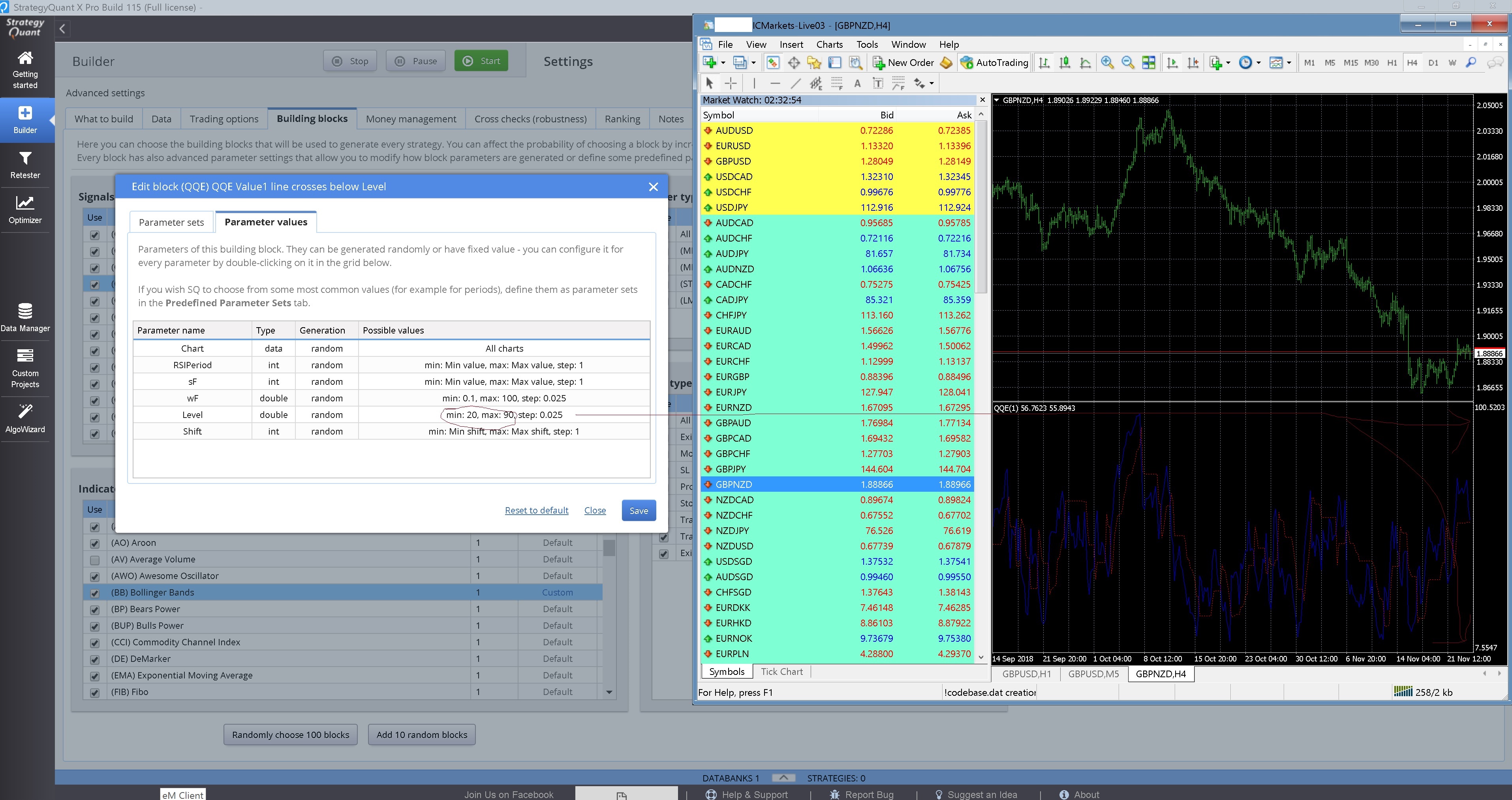

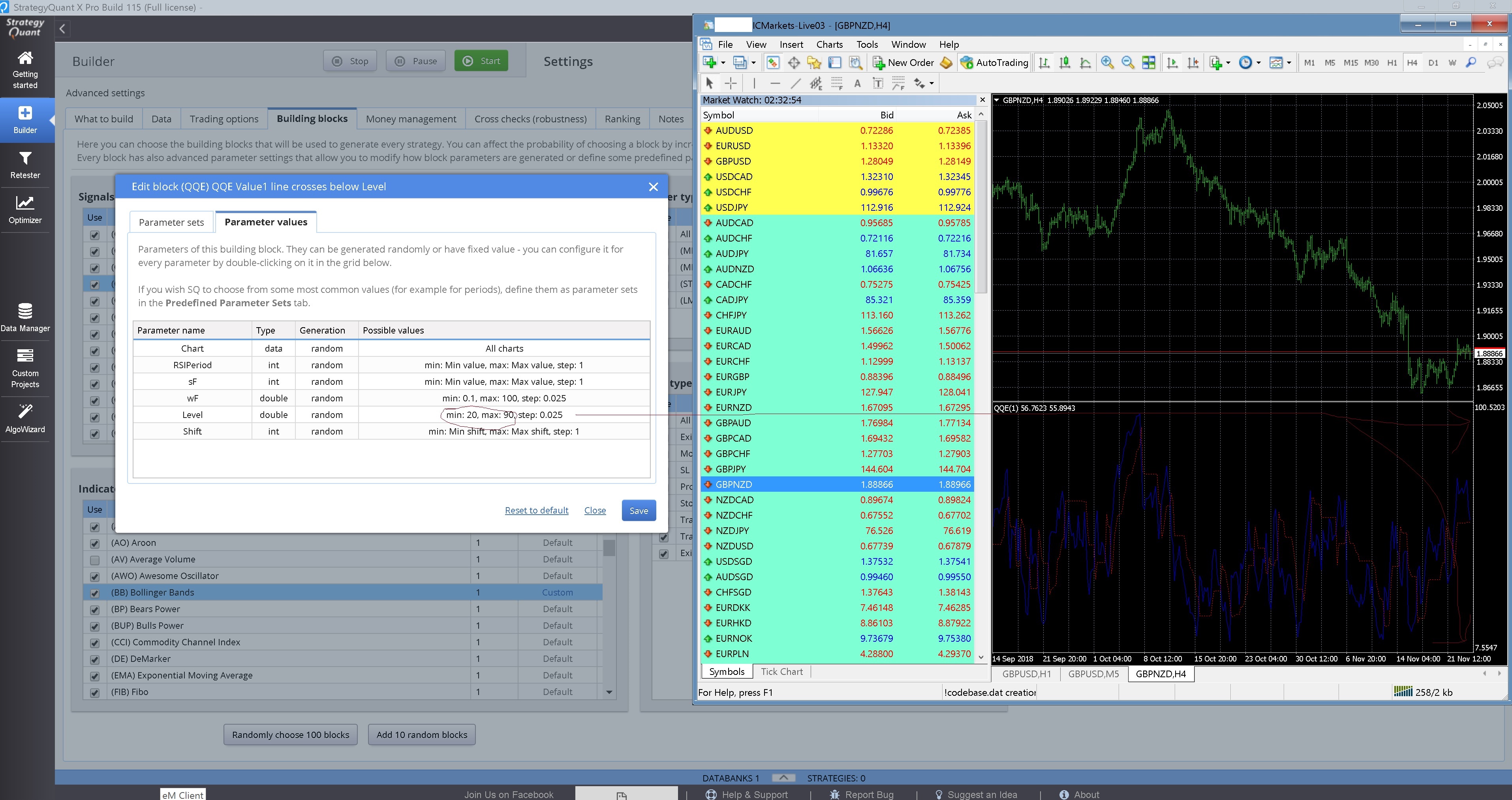

All blocks that use "QQE": Level in the new "Default" config is between 20 to 90, while in reality it clearly oscillates between 0 and 100 (just like RSI). See attached "QQE.jpg" screenshot. Also, the step size should be 0.25, not 0.025.

All blocks that use "CCI": Level in the new "Default" config is now set to between -300 to 300, while I suggested -500 to 500. No screenshot attached for this one, as you can easily check this, but especially on higher timeframes and longer CCI periods, the oscillation is rather in the -400 to 400 range, -300 to 300 is too tight.

All blocks that use "PSAR": there seems to be a mix up, as you´ve followed my suggested values for the "Parabolic SAR" entry in the "Indicators" block (Step, Min: 0.01, Max: 0.2, Step: 0.001 / Maximum, Min: 0.01, Max: 1.0, Step: 0.01), but not for all the PSAR entries in the "Signals (Predefined conditions)" blocks, there you are still using the old values. I´d highly suggest changing all PSAR blocks to the above-mentioned values, as I have several good strategies which for example use a "Maximum" of 0.6 for PSAR, while you limit this to 0.4 in your "Default" settings. Also, the step sizes for PSAR really need to be that low, as even 0.001 make a big difference. Again, if you simply copy the config "Parabolic SAR" block in "Indicators" to all the ones in "Signals", this will do the trick.

All blocks that use "Bollinger Bands" / "Keltner Channel" / "MT Keltner Channel" / "BB Range" / "BB Width Ratio". I had suggested a Deviation of min: 0.01, max 10.0, step 0.01, but SQX still uses the rather low range settings of min 0.5, max 3, step 0.1. I´d highly recommend going to my suggested values as you can easily verify in MT4 that all these related indicators still give crossings and hence signals on the outer bands even if using values like 9.0 for the deviation, so 3.0 as the max is too low and 0.5 for the minimum too high. I again have good strategies which use deviations of > 7.0 and are profitable, so 3.0 limits this indicator a lot.

"Is falling" / "Is rising" block. I had adjusted the "Bars falling" to a max of 50, you´ve cut it back to 10. Same goes here since I have set the values that high, I (or rather SQX, haha) have found several strategies that use this for an exit and use values up to 45 there, so I can only suggest to change it back to 50.

"Bars Valid" within "(STOP) Enter at stop" and "(LMT) Enter at limit": the default is a max of 20 bars here, which is much too short. Almost all strategies that I have use ~80 bars on H1 systems, almost none of those use below 40 bars, so 20 is a big issue which will seriously cut the number of profitable strategies found. I´d highly suggest a value between 1 to 120 there, possibly even more for strategies < H1, so better 0 to 500 maybe, but def. not 20 as a max.

"Exit after Bars" has a default max value of 20. Again, this is much to short and leads to that exit feature not being used at all most of the time as it cannot be profitable with such a short max duration. Most of my H1 strategies use values in the 40 to 150 range. Lower timeframes will naturally need longer values, so I really have set this to "1000" as the max and would highly suggest that this will be the new default too.

"SL 2 BE Add Pips" has a default step size of 10, which is too high in my opinion. I would suggest 2 or 5 at the most.

"Trailing Activation" has a default step size of 10, which is too high in my opinion. I would suggest 2 or 5 at the most. Also, it´s default max of 100 pips seems a bit low, I´d suggest at least 300 as the max.

That´s all for now :-)

-

Votes +18

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

geektrader

13.12.2018 07:47bentra

29.12.2018 21:29For "Exit after Bars" I'd say 40 is too high to be a minimum. I have decent strats with as low as 16 bars. Please don't go more than 20 for a MINIMUM "Exit after Bars"so I'd say 15-150 should make everyone happy. (My strats tend to show anything over 64 MAX is somewhat redundant but w/e)

geektrader

29.12.2018 22:10geektrader

29.12.2018 23:41hankeys

30.12.2018 11:21geektrader

30.12.2018 19:07Mark Fric

03.01.2019 09:24Status changed from New to Fixed

Thank you all for your work and comments.

Geektrader - the idea of calibration is good, I created a task for it: https://roadmap.strategyquant.com/tasks/sq4_3860

geektrader

03.01.2019 09:59Attachment Untitled.jpg added

Re: "I still think it doesn't make sense to use deviations bigger than 3"... Really? Check the screenshot :-) Hence the calibration thing would be the best idea as the ranges can be that different.

geektrader

03.01.2019 10:35geektrader

03.01.2019 10:35© Copyright. All rights reserved. ProjectPanel.com

{kind=link}