SQX Strategie gets other results on liveaccount as in SQX by himself

Hello,

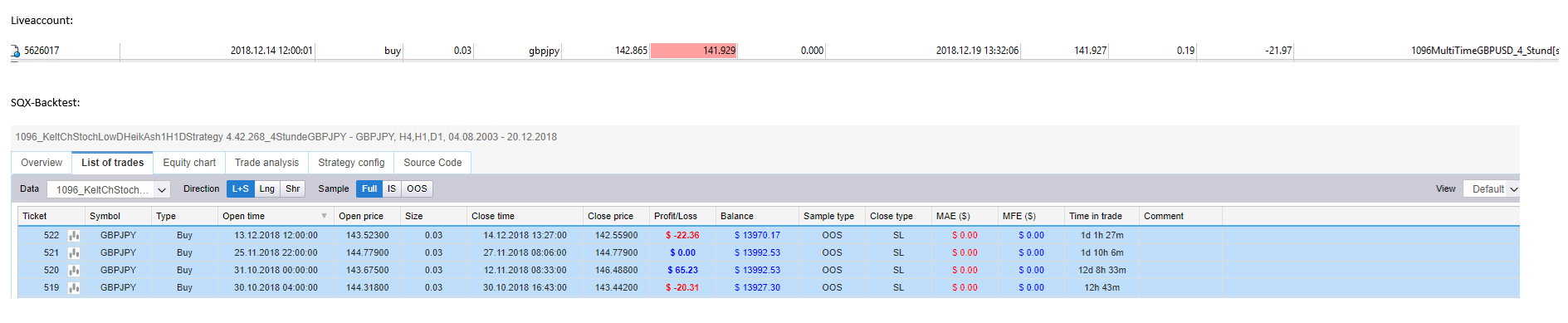

My attached file (GBP/JPY) has different results in the liveaccount than I get in the backtest at SQX.

The Strategy triggered 1x on 13 December and was closed again on 14 December. In the live account it ran until 21.12.2018 and was closed .

Why is this so?

-

Votes +1

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

geektrader

29.12.2018 20:19Description changed:

Hello,

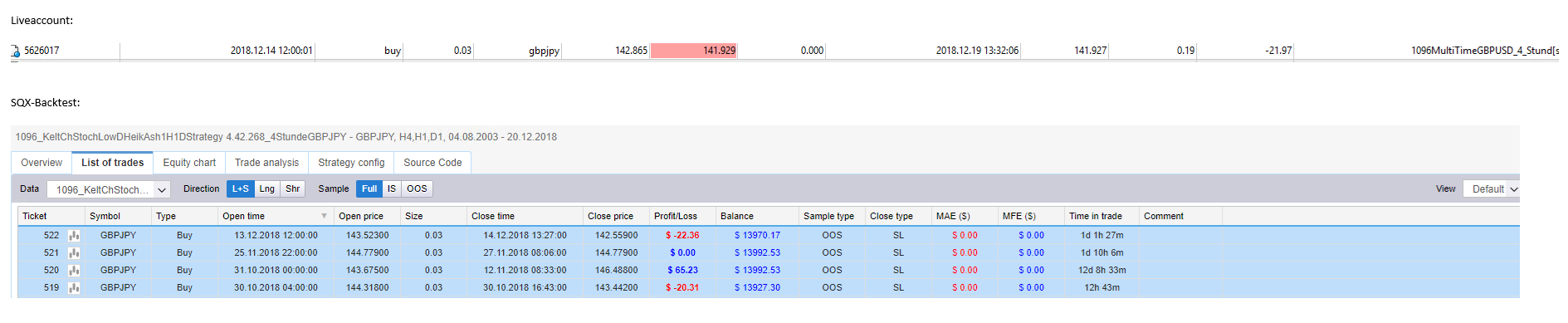

My attached file (GBP/JPY) has different results in the liveaccount than I get in the backtest at SQX.

The Strategy triggered 1x on 13 December and was closed again on 14 December. In the live account it ran until 21.12.2018 and was closed .

Why is this so?

Marcel

30.12.2018 16:57My confidence is accordingly a little shaken.

But I decided to do a real broker test with the EAs now.

All EA´s run at the same time with 3 different brokers, among other things also Dukascopy. After 2-3 months all data are placed next to each other and compared how reliable the backtest of SQ actually is....especially in the real test with Dukascopy you will see how trustful SQ is.

geektrader

31.12.2018 01:45anonymous

20.03.2019 20:15Tomas Brynda

14.06.2019 14:37Status changed from New to Fixed

Hello Marcel,

I am closing this task as it is probably not a bug in SQ.The other thing is these kinds of strategies (using multiple symbols or timeframes) are very hard to debug.

We would need some more materials to work with. We haven't discovered any problems in the attached strategies so far.

A lot of fixes has been made since the task was opened and I believe SQ backtest engine is reliable enough.

We are doing automated tests containing over 1000 strategies before every build to make sure we haven't introduced new bugs.

Feel free to add a comment if you have any doubts or have new information on this topic.

Best regards,

Tomas

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}