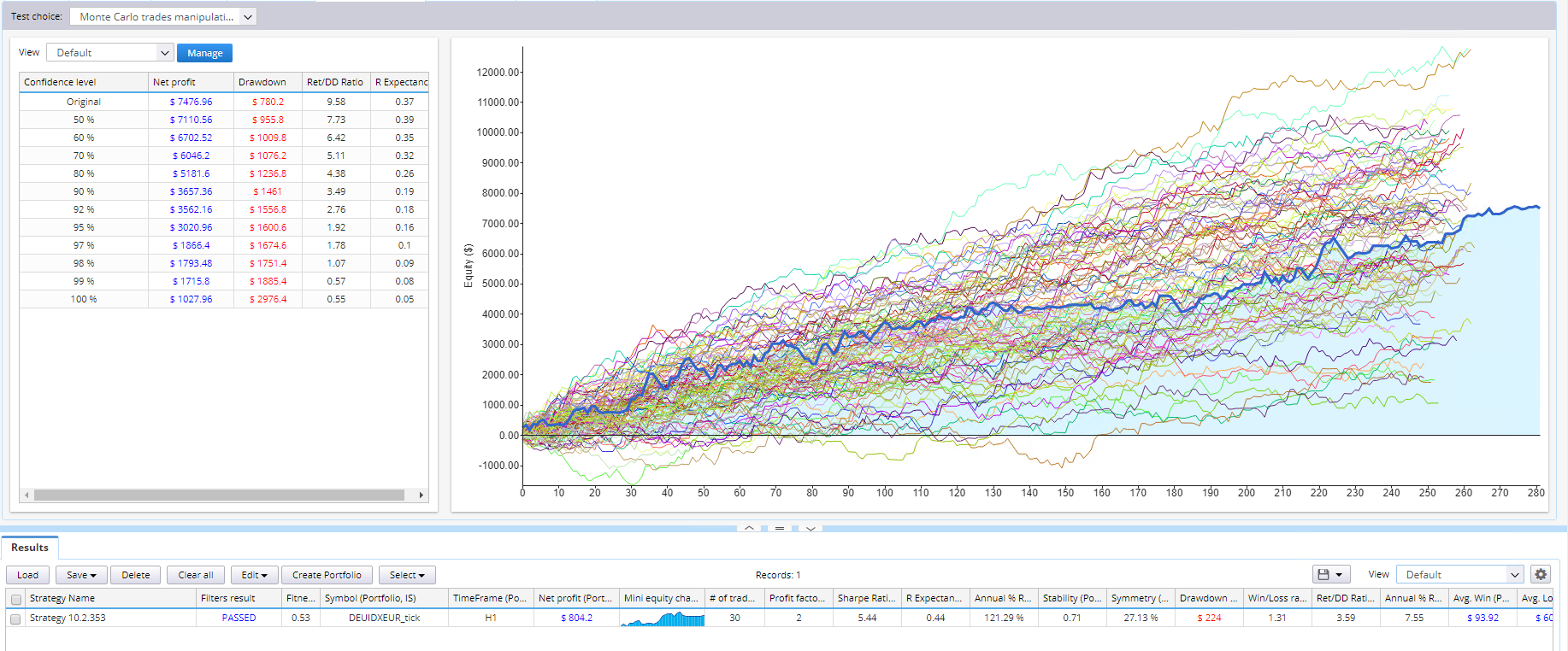

Montecarlo simulation only on all sample

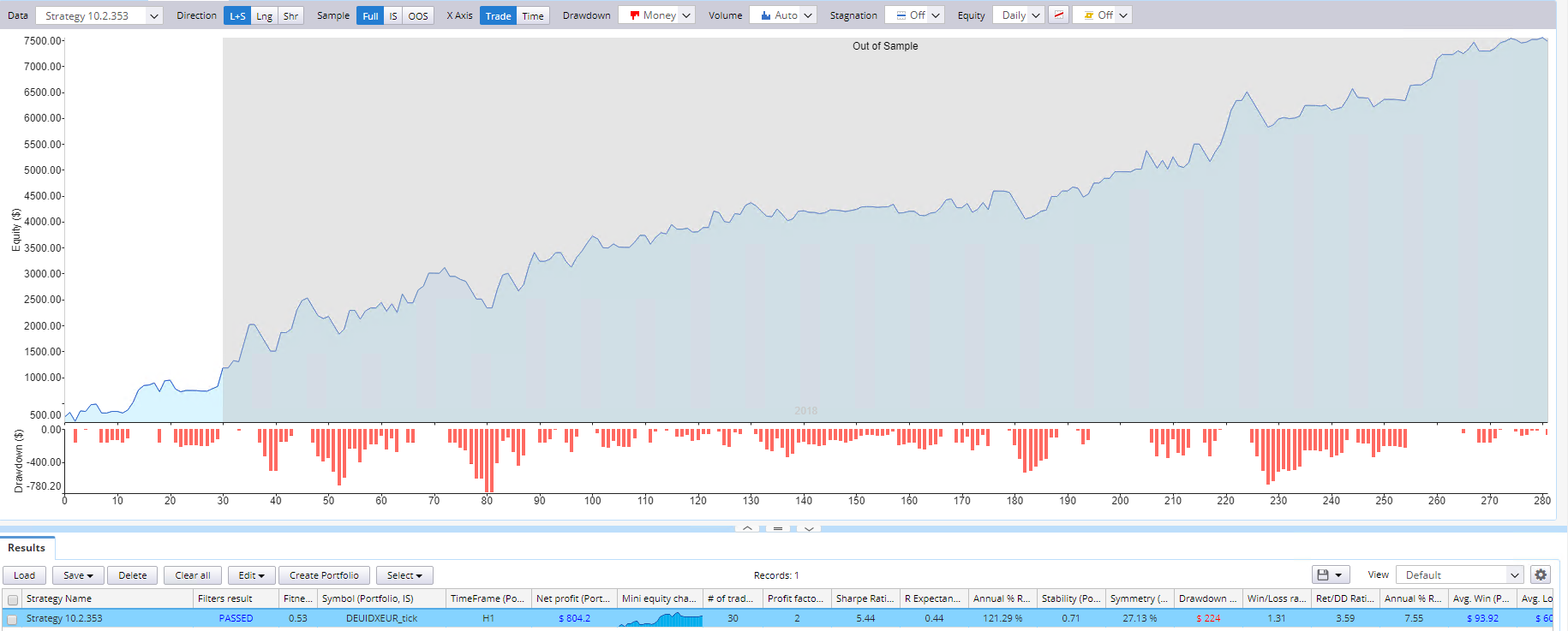

In the attached screenshot you can see an example of normal backtest, with one month in sample and six months out of sample. In the second screenshot you can see the same strategy with the montecarlo simulation. As you can see, Montecarlo uses all the trades, both in sample and out of sample.

So, we can't use the Montecarlo as a robustness test: if we would like to select only the strategies that pass the Montecarlo, it would not be possible: the test uses all the trades, even the out of sample. It would be more logic if the Montecarlo would work only in sample: we could control if the strategies that pass the Montecarlo in sample have a good out of sample.

Otherwise, it would be useful introduce the possibility of select the sample where Montecarlo work.

Thank you for your work,

Giuseppe

-

Votes +5

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Normal

History

hankeys

22.06.2019 11:53not in crosschecks, there is everything made for IS+OOS

Phronesis

21.08.2019 13:16Thanks.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}