Return to Draw Down Ratio for Portfolio incorrect OR portfolio graph incorrect

-

Votes 0

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority High

History

hankeys

22.07.2019 07:18bentra

22.07.2019 07:52Attachment Annotation 2019-07-22 015041.png added

bentra

22.07.2019 08:00bentra

22.07.2019 08:03Subject changed from Return to Draw Down Ratio for Portfolio incorrect... to Return to Draw Down Ratio for Portfolio incorrect OR portfolio graph incorrect

bentra

22.07.2019 08:10Attachment Annotation 2019-07-22 020845.png added

Mark Fric

22.07.2019 14:24Status changed from New to Waiting for information

bentra

22.07.2019 16:44Attachment Retest-bugged.cfx added

Attachment bugged-portfolio-line-y 0907.sqx added

Mark Fric

23.07.2019 10:22Drawdown % is computed from Initial capital + Net profit.

In case of Portfolio, its Initial capital is the sum of Initial capitals of all its components.

So if each test has initial capital of 10.000, and there are 10 strategies in portfolio, its initial capital will be 10x10.00 = 100.000.

That's why Drawdown % can look big on equity chart, but is small in %.

Making it configurable is a possible low priority feature, I created a task for it: https://roadmap.strategyquant.com/tasks/sq4_5139

bentra

23.07.2019 10:59Attachment Annotation 2019-07-23 052041.png added

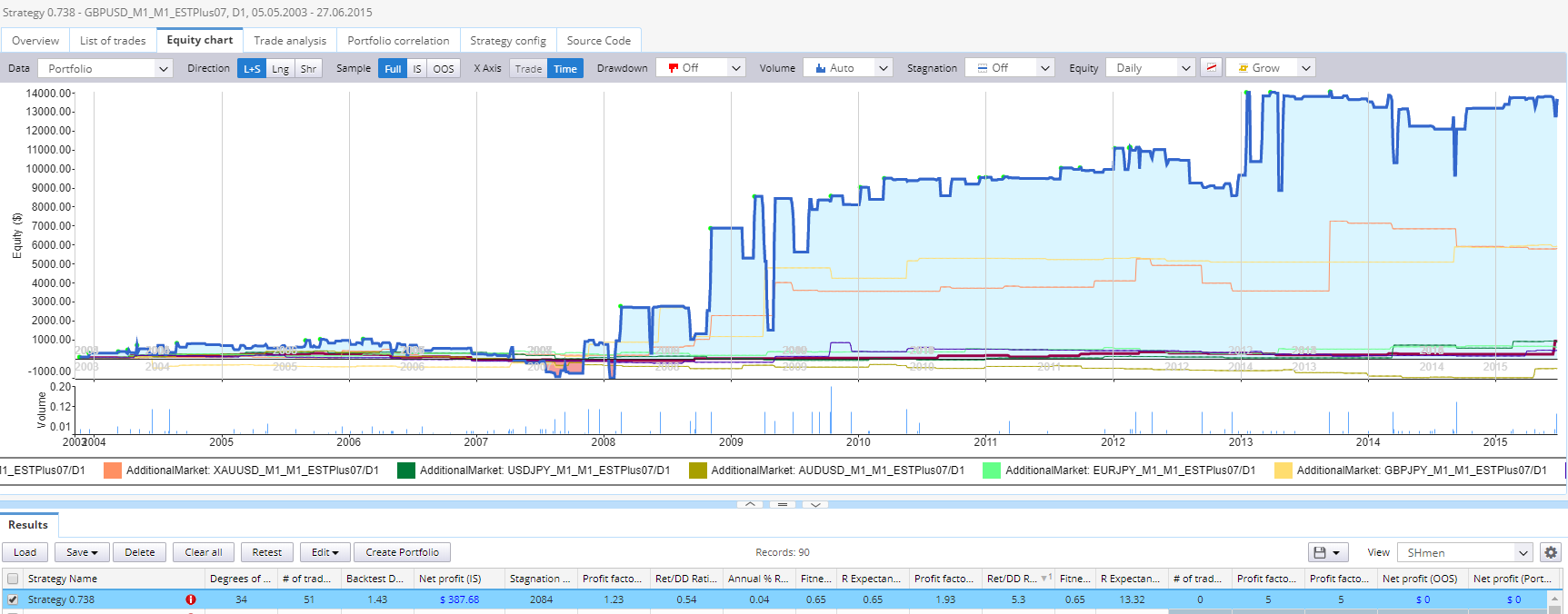

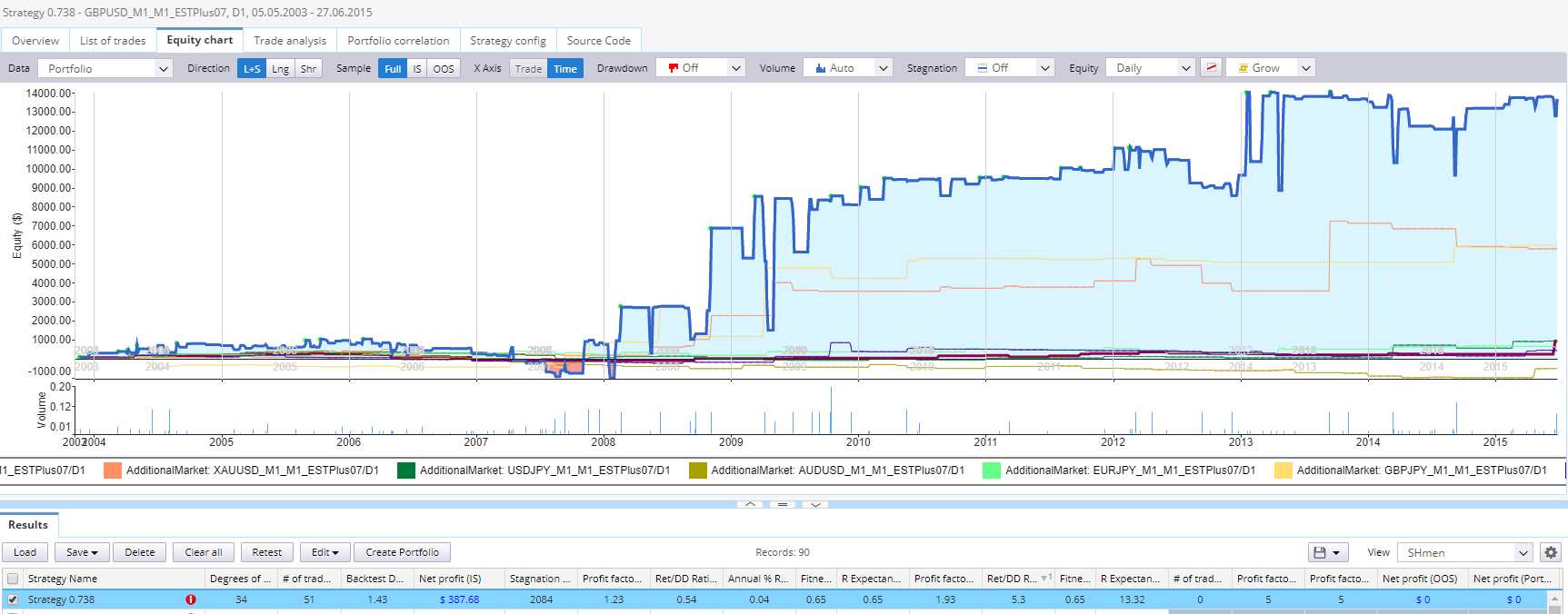

In fact, the portfolio curve doesn't match the portfolio parts very well at all, drawdowns by the portfolio line where no drawdowns are shown for the portfolio parts lines.

Mark Fric

23.07.2019 11:34Priority changed from Normal to High

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}