Need more exit types.

I am not sure this issue is proper here, or in SQ X programing.

The trailing stop in SQ X with atr is

Close ± N * ATR (Multicharts code)

Please add new some exit typee.

1, It's like this. In long position, I want the trailing stop is always the highest value, and in the short position, the trailing stop is always the lowest one.

// EL code

LongTrailingStop = close - N*ATR;

if LongTrailingStop < LongTrailingStop[1] then // in longpostion, the trailing stop is always the highest value

LongTrailingStop = LongTrailingStop [1]

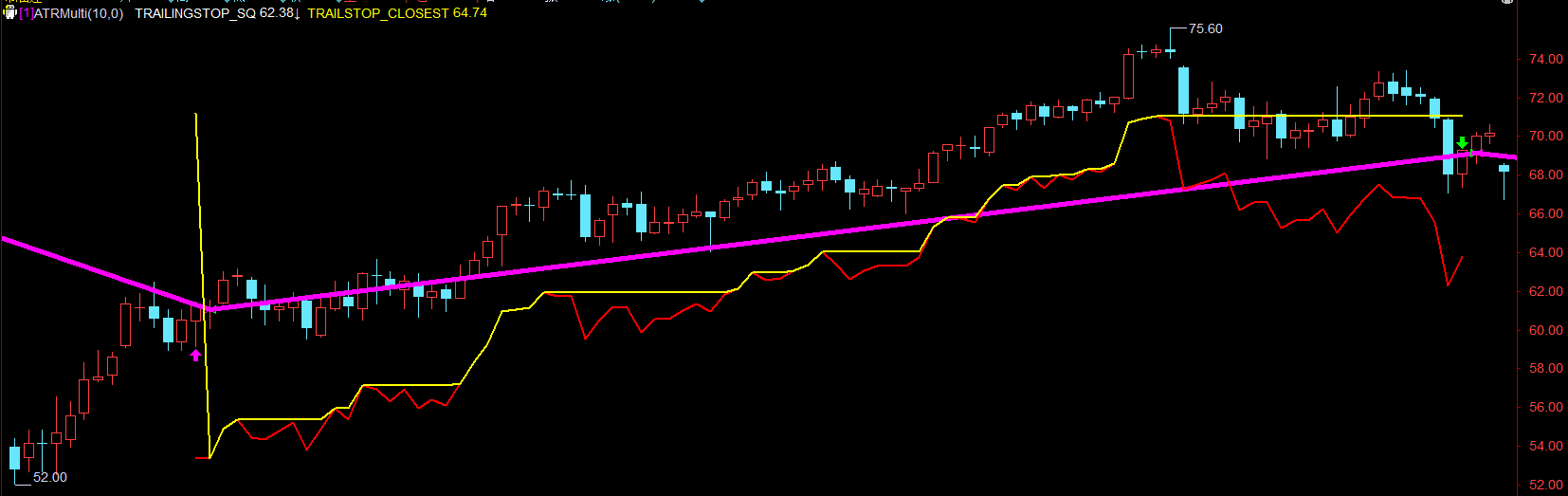

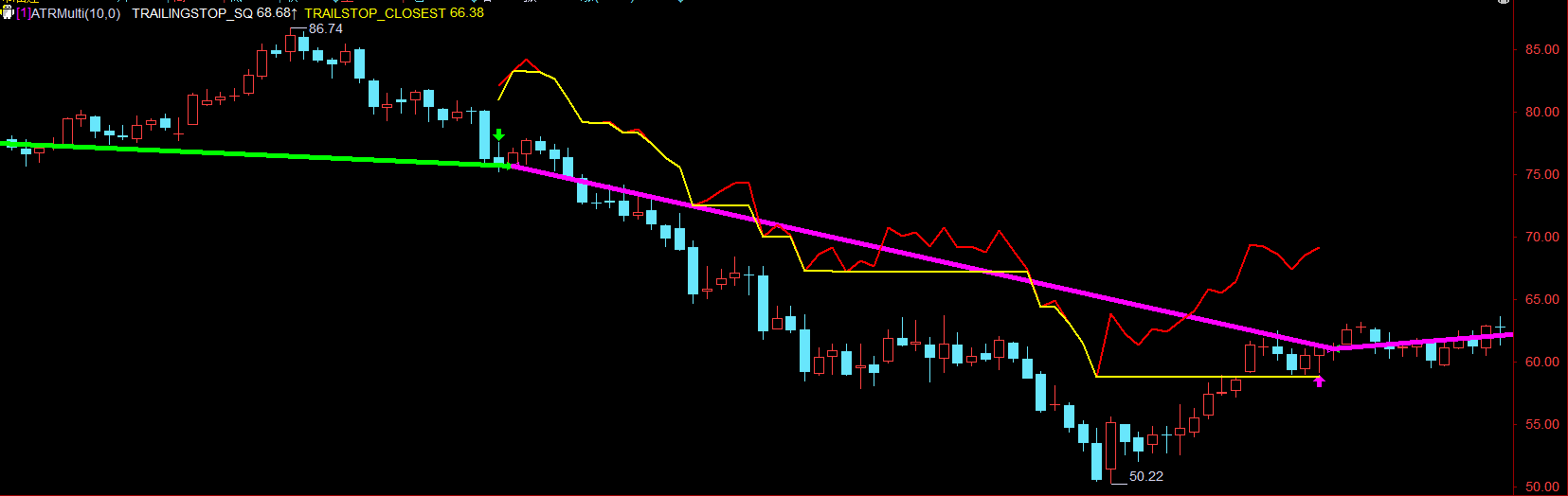

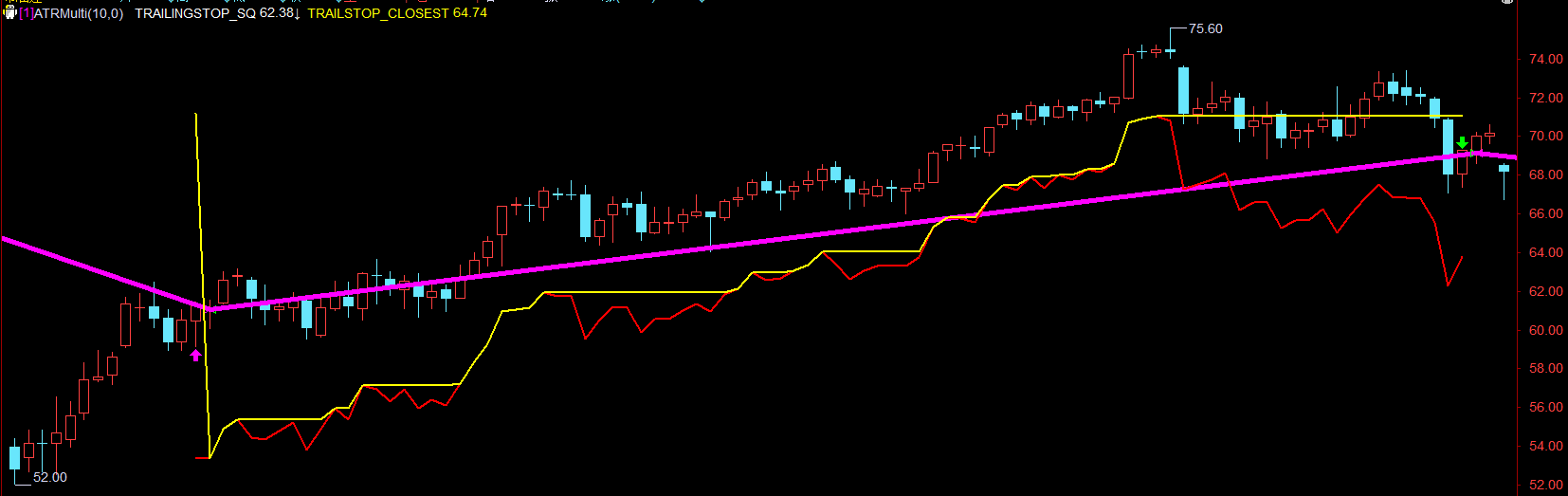

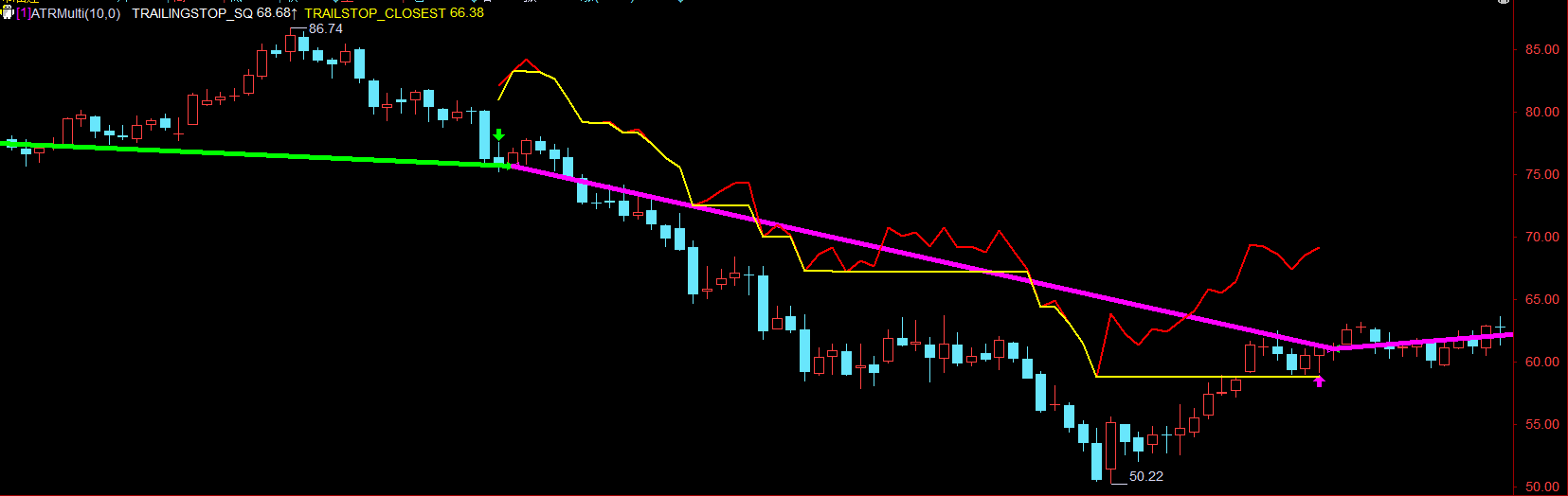

Like the picture below.

2, And is it possible that allow us to choose the price for tracking? I want to use high when in long position, and low in short postion.

if marketposition = 1 then begin

LongTrailingStop = High - N* ATR;

end;

if marketposition=-1 then begin

ShortTrailingStop = Low + N*ATR;

end;

3, Maybe it's allowed using average of standard deviation, or bar range instead of ATR value in trailing stop or stop loss.

-

Votes 0

-

Project StrategyQuant X

-

Type Feature

-

Status Archived

-

Priority Normal

-

Assignee None

History

eastpeace

22.09.2019 12:21Description changed:

I am not sure this issue is proper here, or in SQ X programing.

The trailing stop in SQ X with atr is

Close ± N * ATR (Multicharts code)

Please add new some exit typee.

1, It's like this. In long position, I want the trailing stop is always the highest value, and in the short position, the trailing stop is always the lowest one.

// EL code

LongTrailingStop = close - N*ATR;

if LongTrailingStop < LongTrailingStop[1] then // in longpostion, the trailing stop is always the highest value

LongTrailingStop = LongTrailingStop [1]

Like the picture below.

2, And is it possible that allow us to choose the price for tracking? I want to use high when in long position, and low in short postion.

if marketposition = 1 then begin

LongTrailingStop = High - N* ATR;

end;

if marketposition=-1 then begin

ShortTrailingStop = Low + N*ATR;

end;

3, Maybe it's allowed using average of standard deviation, or bar range instead of ATR value in trailing stop or stop loss.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}