Impossible Trade Multicharts

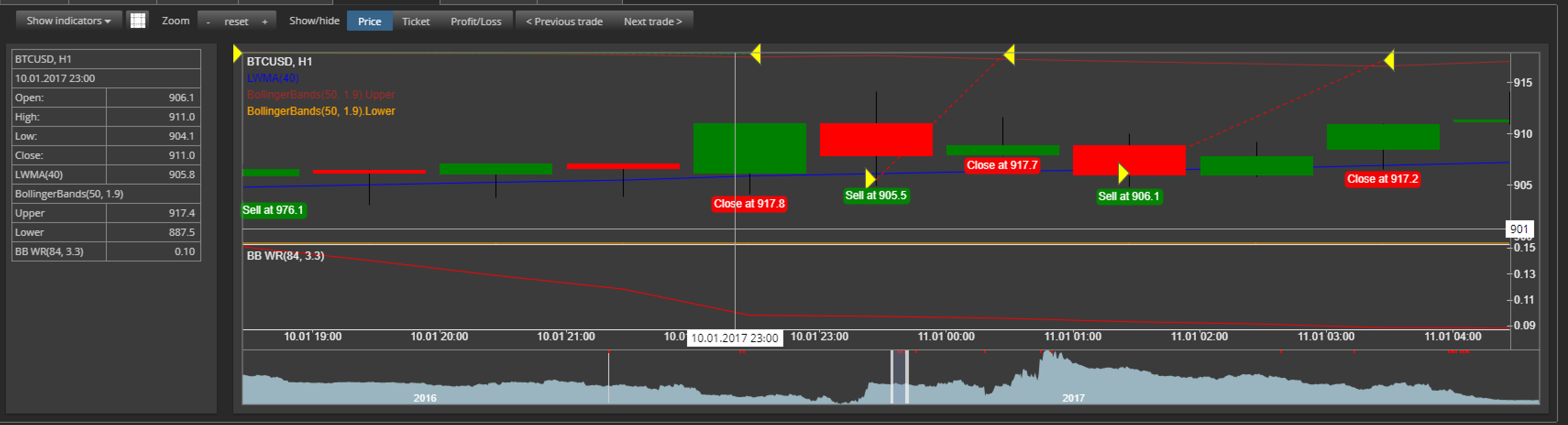

I 'm referring to trade that happened at 10.01.2017 23:00.

-

Votes 0

-

Project StrategyQuant X

-

Type Bug

-

Status Refused

-

Priority Normal

History

CooleRnax

07.11.2019 01:32Description changed:

I 'm referring to trade that happened at 10.01.2017 23:00.

CooleRnax

07.11.2019 14:39Attachment 4.png added

Here is the data and settings

https://www.dropbox.com/s/d1txbk8znicllnq/btcusd.csv?dl=1Tomas Brynda

07.11.2019 15:27Status changed from Waiting for information to In progress

Mark Fric

08.11.2019 12:49Status changed from In progress to Refused

Bid price at 10.01.2017 23:00 is 911.0, spread is 8, so Ask price is 911 + 8 = 919.

You see Bid prices on chart, not Ask prices.

I think your definition of instrument is wrong. Spear id in pips, so if you have Pip/Tick size = 1, then spread=8 means 8 full points. That doesn';t seem correct to me.

And Pip/Tick Step is also incorrrect I think, I can see that the minimal move in your data file is 0.01, and this should be your Pip/Tick step.

CooleRnax

08.11.2019 14:35My exchange uses 5 significant digits size for bitcoin and there no such thing as step.

It looks like this as price grows:

1.1111 - min movement is 0.0001

11.111 - min movement is 0.001

111.11 - min movement is 0.01

1111.1 - min movement is 0.1

11111 - min movement is 1

I can't backtest old data (before 2016) because tick size between old data and new data is too different and strategy quant uses static instrument size.

I have chosen this sizer 1111.1 - min movement is 0.1 as the most relevant.

I expected spread to be in steps instead of sizes.

Mark Fric

08.11.2019 14:54Spread is in pips, not in minimal steps

CooleRnax

08.11.2019 15:56Attachment 5.png added

Attachment 5.png deleted

Attachment 5.png added

This is my new settings.

Does it look ok for you?

CooleRnax

08.11.2019 16:33Because it is combined data.

So from my point of view :

bid should be imported - spread / 2

ask should be imported + spread / 2

CooleRnax

08.11.2019 17:50Attachment 5.png added

CooleRnax

10.11.2019 23:44And to use it only in single spread robustness test.

I would like to hear you feedback about this.

The way it is implemented right now seems wrong to me.

Because it can cause such impossible trades.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

Hi CoolerNax,

I tried to retest your strategy on BTCUSD data downloaded from coinbase. I used exactly the same settings, but got different results.Can you attach your history data or specify which data sources you used?

Best regards,

Tomas