Computer crashing after x-thousands of optimizations

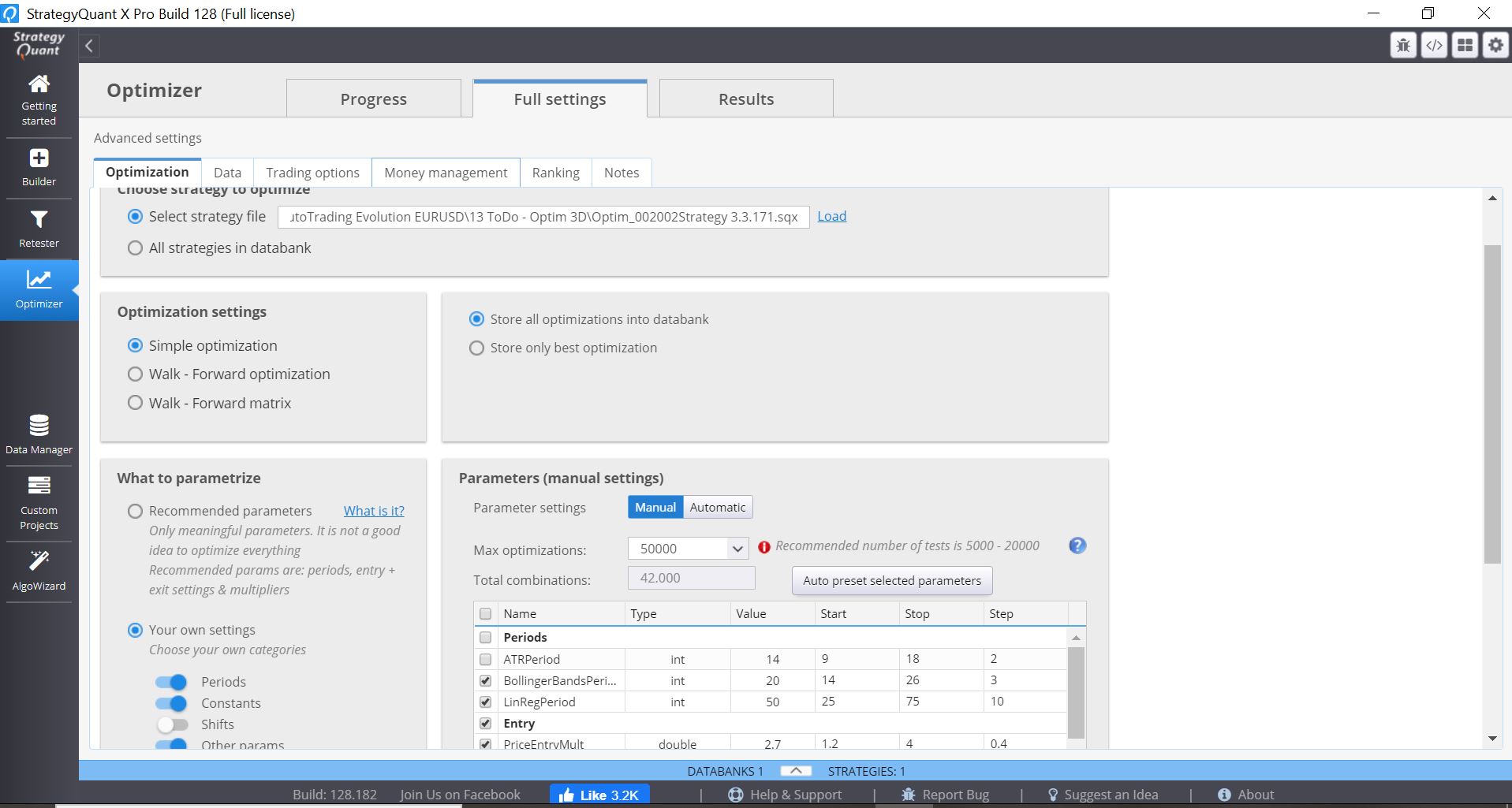

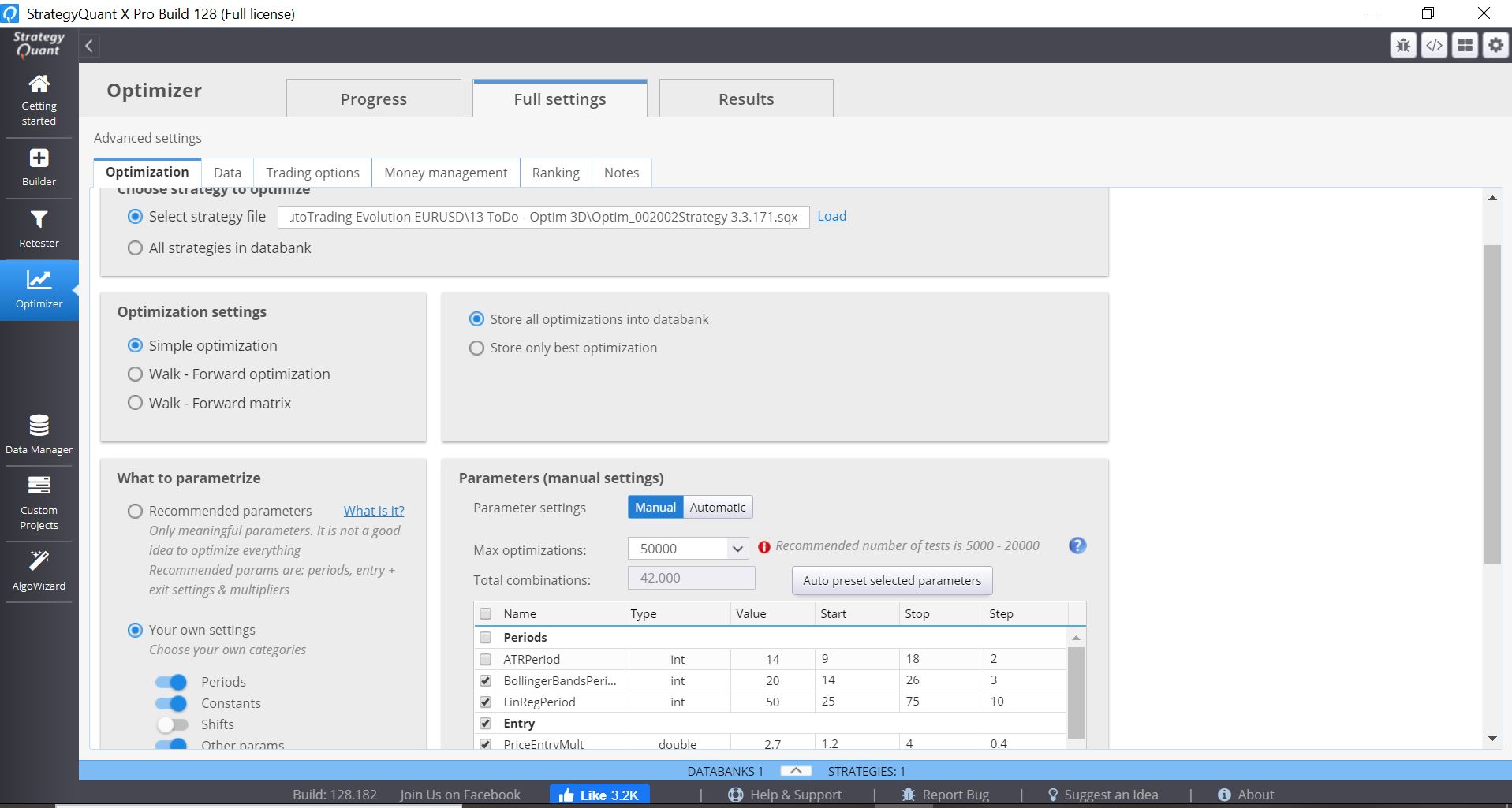

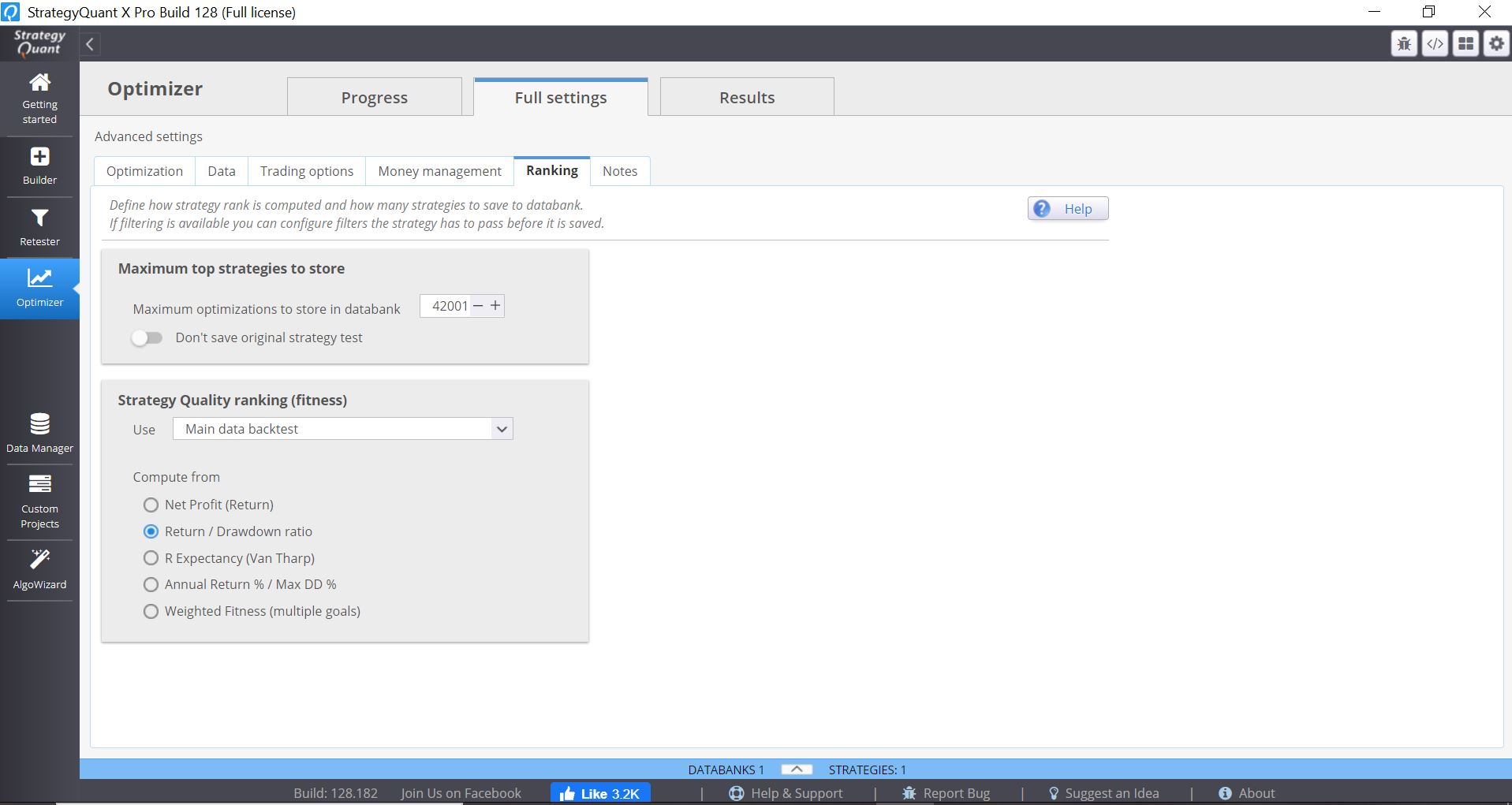

I am performing an optimization of a strategy, with the settings that you can see in screenshots 1 and 2, that is Max optimizations = 50.000,

Total combinations = 42.000, Maximum optimizations to store in the databank = 42.001.

In the files attached you can find: some screenshot, the strategy file, the config file, the log file.

Three times, after 3/4 hours of work, StrategyQuant crashed after 12.000, 13,000 and 14,000 optimizations. The SQX program showed to be completely blocked so that I had to end the Task from the Windows Task Manager.

I made a fourth attempt changing the Data > Test Parameter Precision on "Selected timeframe only" (that is H1), StrategyQuant processed 35.000 optimizations before crashing.

StrategyQuantX, Build 128.182.

My computer is relatively new, with an i7 processor and 32GB of RAM memory.

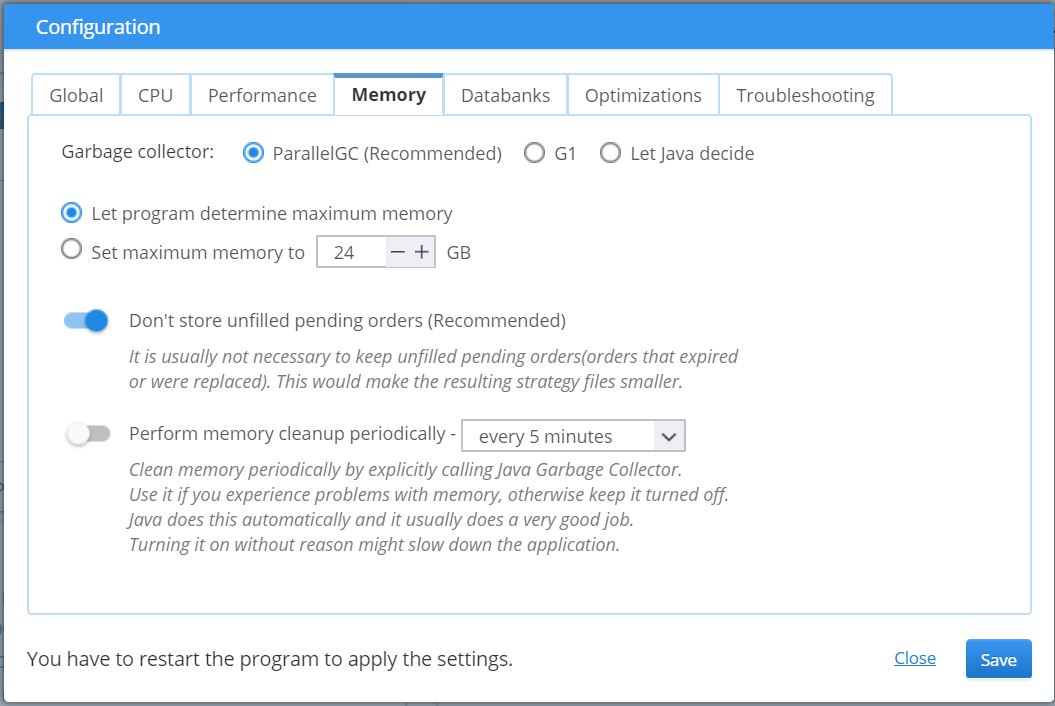

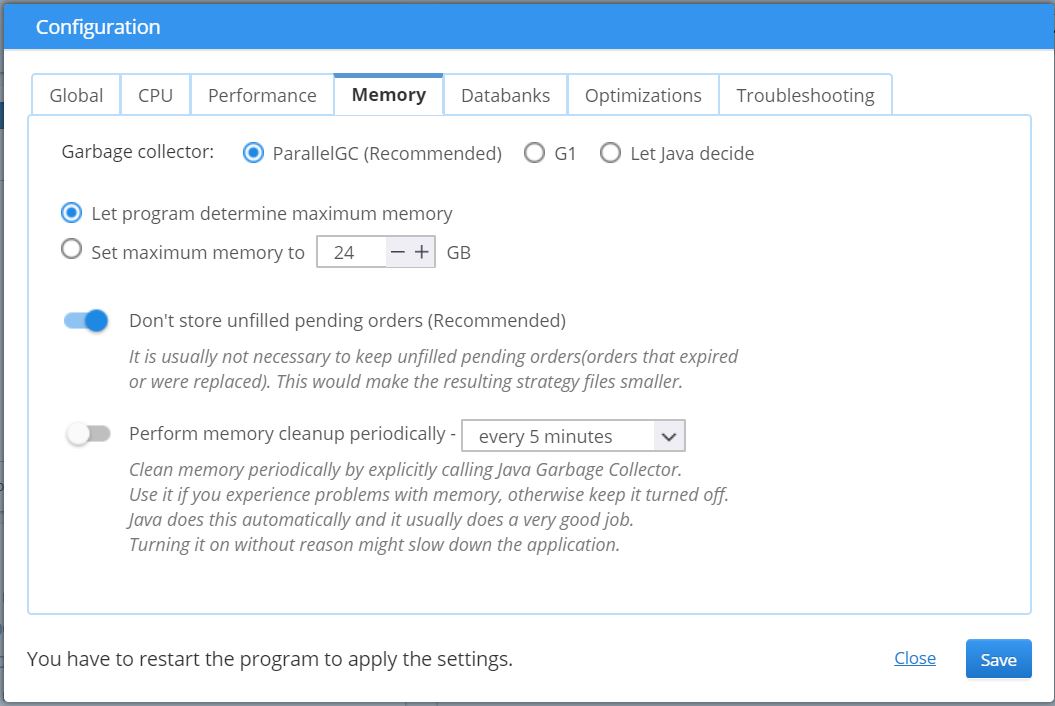

In screenshot 3 you can see the Memory configuration that I set, but I also tested the "Set maximum memory to 24 GB" setting, with the same result.

The log file is incomplete because, as I said, the computer crashed.

-

Votes +3

-

Project StrategyQuant X

-

Type Bug

-

Status Refused

-

Priority Normal

History

Adriano

20.06.2020 09:38I reserved 29 GB of RAM for StrategyQuant. As the program generates optimizations, the RAM tends to be occupied more and more, until around 35,000 optimizations, it runs out and the program crashes.

Isn't there a way to save optimizations to the hard disk and free up RAM?

hankeys

20.06.2020 11:20i am not using optimisations at all, there is a big probability that you overoptimised you parameters, nothing all and in the real you will get nothing, only losses

but its up to you, i am only of the users of SQX and my workflow is different

Adriano

20.06.2020 13:13Thank you for your answer Hankeys.

I use this tool, not as a means of optimization, but as a test to evaluate the solidity of the strategy and its independence from the values of its parameters.

For this purpose I need to evaluate the percentage of profitable strategies, the shape of the profit graphs, the average profit, etc. on a large number of optimizations.

Adriano

20.06.2020 16:07But maybe, I don't need to store a big number of optimizations in the databank in order to get the SPP and the Optimization data.

hankeys

21.06.2020 09:00Mark Fric

24.06.2020 13:32Status changed from New to Refused

I'm going to refuse it, it is caused by exchausted all the memory - the error message in log shows that.

I think using 50.000 Max optimizations is too much, 20.00 should be enough for relevant optimization results.

Also, you should not store all the 42.000 optimized variants to the databank, if you do it only to run SPP or WFM just the best one is enough.

Or if you want to have more there store 100-1000 strategies in databank, not 40k.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}