Anti-Martingale Money Management (Roulette Trader eBook)

-

Votes +10

-

Project StrategyQuant X

-

Type Feature

-

Status New

-

Priority Normal

History

Dave-S8

30.09.2020 11:57Subject changed from Reversed Martingale Money Management (Reduce size after a loss, Increase size after a profit) to Anti-Martingale Money Management

Lumen2730

01.11.2020 12:37Subject changed from Anti-Martingale Money Management to Anti-Martingale Money Management (Roulette Trader eBook)

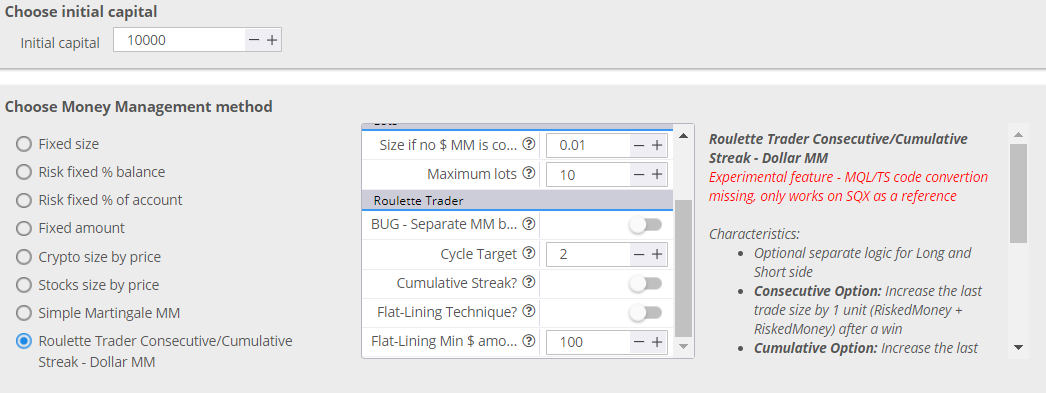

Description changed:

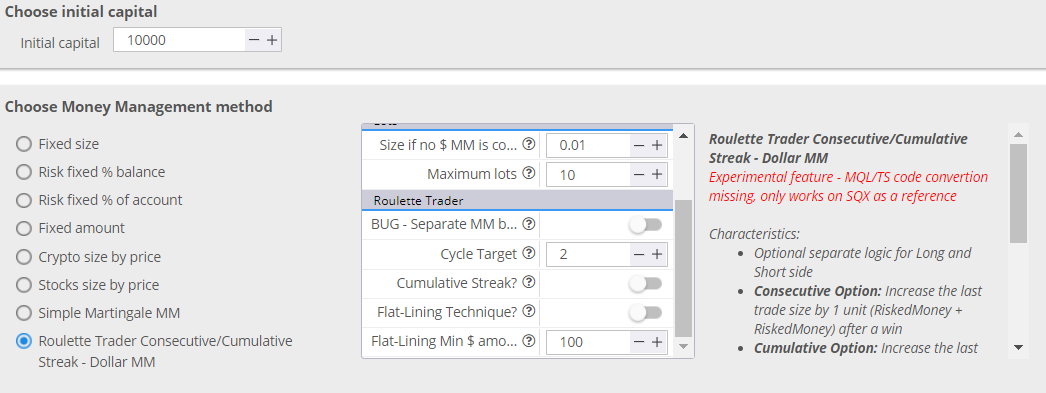

Attachment RouletteTraderConsecutiveCumulativeStreakDollarMM.java added

Lumen2730

01.11.2020 15:33

anonymous

02.11.2020 23:13Michael Bryant talks about "trade dependencies" Where tradeable patterns exist in the equity curve of a strategy. Some more ideas in this context maybe in that interview near the 20 minute mark.

-increase/reduce MM above/bellow a MA of the equity curve

-reduce sizing if x losses occur in a row.

-increase sizing if y wins occur in a row.

I don't know about resetting at a certain point but maybe a cap and floor.

Karish

10.11.2020 22:48hankeys

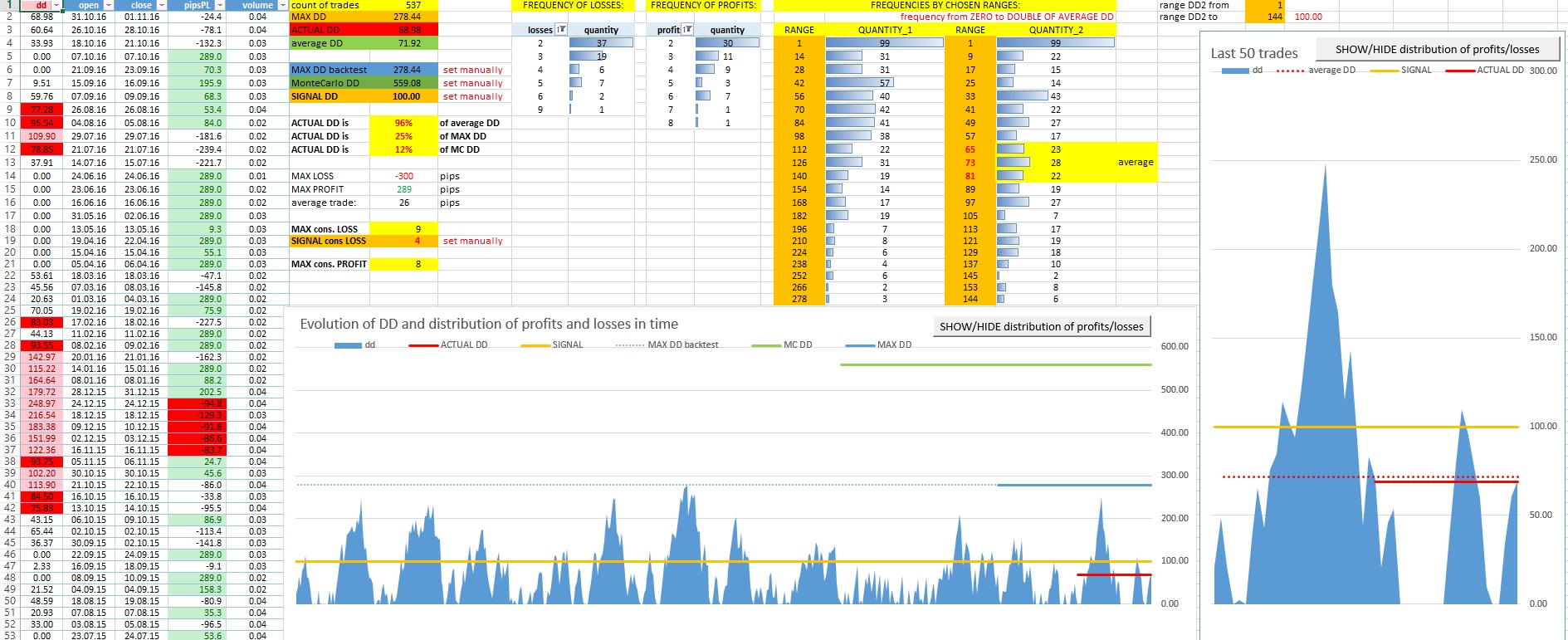

11.11.2020 09:32Attachment drawdown_distribution.jpg added

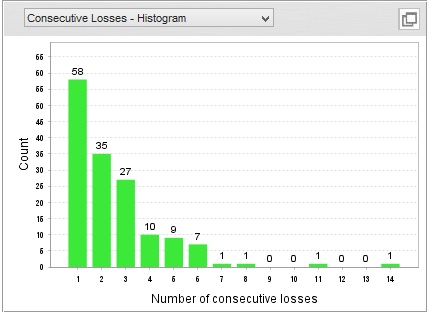

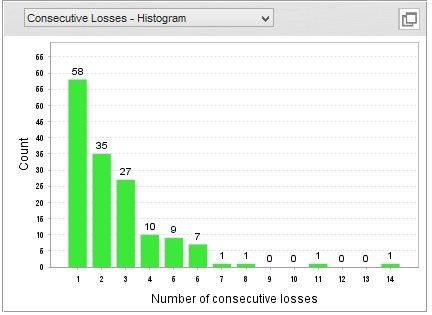

Attachment histogram of consec losses.jpg added

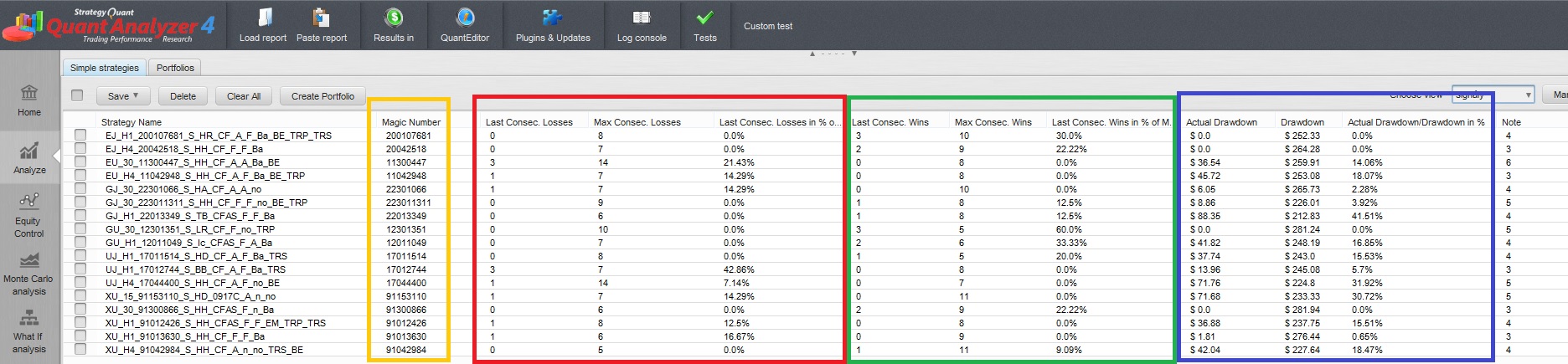

Attachment new QA columns.jpg added

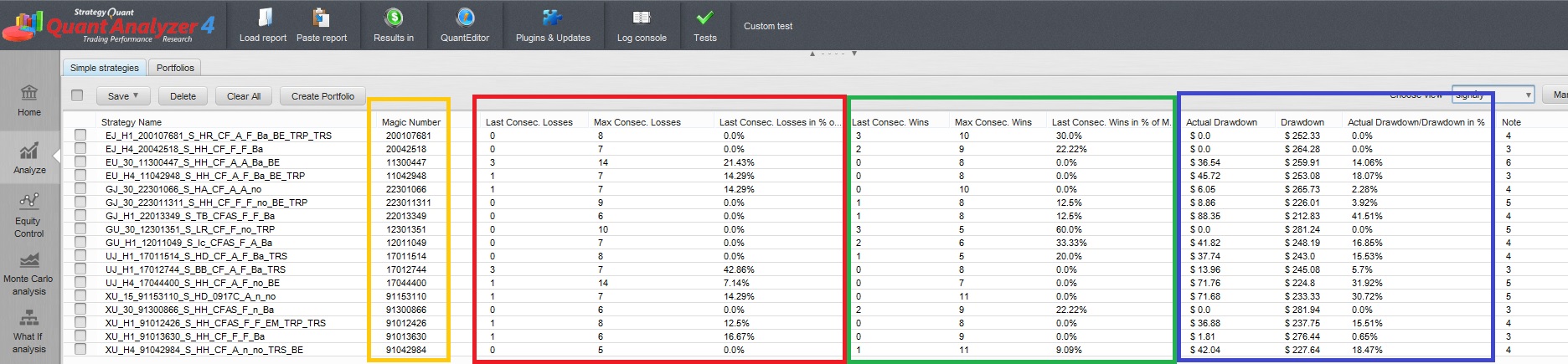

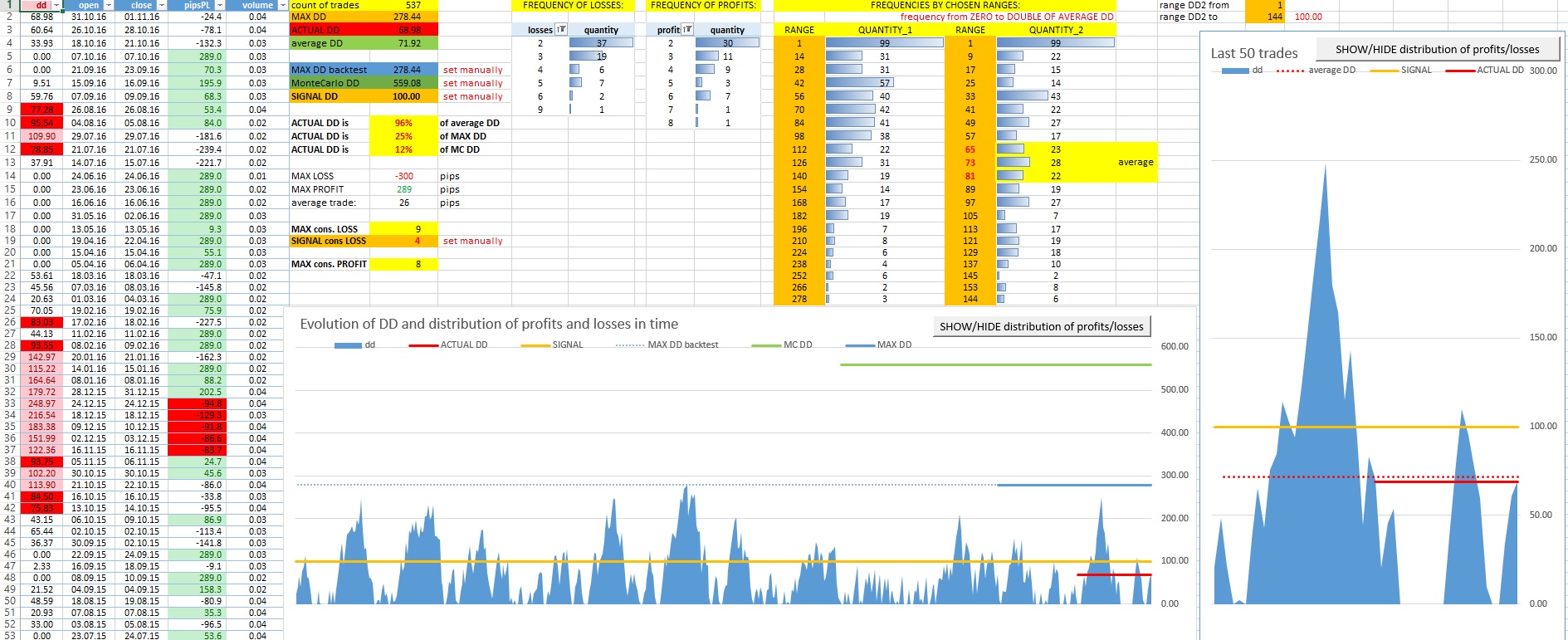

reminds me my early times with SQ3 in 2016 when i have made snippets to QA analysing consec losses and profits and trying to find optimal values where to add or remove from positions - yes there were times when everything works, but very soon came periods when it mostly ended in bigger losses

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}