I hope the number of trades in fitness function can be maximized

The more the total number of closed trades (# of trades) during the trading period, the more the statistical significance, so I want to maximize the number of trades (# of trades) in training fitness.

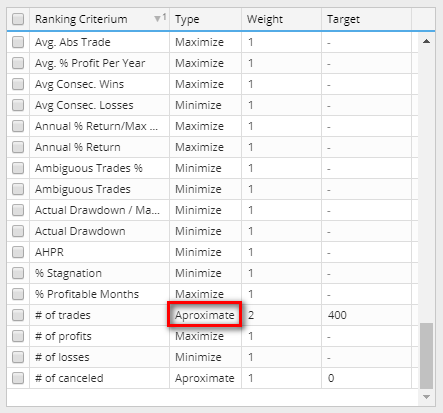

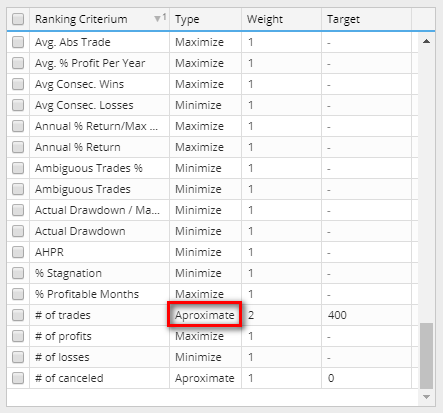

However, the (# of trades) in the Strategy Quality ranking (fitness) only show the type "Aproximate" and cannot be changed to "Maximized".

I suggest that SQX can add another type for (# of trades), and the average number of trades per day/month/year...etc. So that user can use this option in Custom filters. It's will be very useful by setting like this( trades pre days >= 0.2).

-

Votes +3

-

Project StrategyQuant X

-

Type Feature

-

Status Refused

-

Priority Normal

History

Randy

15.09.2020 10:33I hope you can understander the intraday strategy in the futures trading.

If the program can build an intraday trading strategy which includes commission + spread + slippage, and it still makes money, why don't I maximize the number of trades?

Why I say this is because the number of trades in my build strategy by the software is relatively small.

That's why I'm asking if you can help me maximize the number of trades.

I know that I can set the parameter to 1000000 as the target, but this is related to the fitness function. I don't know if the program use normalizes in the initial population.

And I suggest that the program can use the metrics "trades per day" >0.2 is because we expect there is at least one open trade in a week.

It's different to put 10000000 as the target, especially in genetic programming.

Karish

29.09.2020 00:15Randy is totally right, i'm in for maximizing the # Trades,

The model developed by Renaissance for Medallion and Medallion with barrier options makes predictions that are profitable only slightly more often than not. Moreover, the predicted price movements can be easily overwhelmed by external events. To compensate for these factors, the model generates a large number of recommendations, so that by virtue of the mathematical principle known as the law of large numbers, the variability of the returns produced by the model is greatly reduced.

Renaissance searched for “overlooked” edges and joked about a 50.75% win rate while utilizing the law of large numbers to win in the long-run.

“We’re right 50.75 percent of the time… but we’re 100 percent right 50.75 percent of the time. You can make billions that way”

Often times we get caught up searching for the holy grail or the perfect entry/exit for our trading or strategy development. But even with all these PhDs, RenTech was excelling trading a nearly 50% winning system to generate such astronomical returns. Much more can be gained by combining and adding unique smaller edges together than wasting time hunting for the perfect holy grail strategy!

If the mighty Simons says so, we should be all in for that. :)

Randy

14.10.2020 08:36It seems that they will not look back after rejecting this task.

Should I open a new task for this?

Strangely, SQX uses genetic programming to create trading strategies.

The algorithm should not limit any ideas, but the system settings will limit non-traditional ideas.

I don't know what logic this is.

Mark Fric

14.10.2020 08:59It will work correctly also in genetic evolution.

I believe you misunderstood the meaning of that quote. We should have some number of trades to make results statistically significant, and if you have over 50% success you'll make money in the long run, but he doesn't say the goal is to have as many trades as possible. Each trade costs you in slippage and commission.

Randy

14.10.2020 10:01Dear Mark

Thanks for your reply, I try to explain some practical problems.

In my understanding, goals, and constraints are different in the algorithm. Constraints are usually necessary restrictions in practice.

I think it will be a problem to set a large value as the target.

For example, The number of 1000000000000 trades is out of reach for the number of trades in one or ten years.

This will have no effect on the objective function unless your objective function is normalized by the initial population.

This means that I have to reset every time I change the training data range.

I tend to use the normalized initial population to maximize the number of trades, and also constrains the number of trades per day to be greater than 0.1 or 0.2 (for example), I think this is more reasonable.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

As for avg trades per day/month etc. it is already there, but it is set to be minimized. I don't see a scenario when it is better to have more trades than less - if there are enough trades to be statistically significant. Every trade means additional comission + spread + slippage, this is why their number should be minimized.