normalise strategy drawdowns

i want to run automatic retest and normalize the drawdown to the "same" value - so if i set, that i want to normalize the drawdown to 1000 USD, some strategy will have 3.33x bigger position, and strategy with highest drawdown will have half position

can this be added to for example automatic retest task?

-

Votes +11

-

Project StrategyQuant X

-

Type Feature

-

Status Refused

-

Priority Normal

History

Mark Fric

11.09.2020 12:19Status changed from New to Refused

hankeys

11.09.2020 12:55and its simple - add another MM method in automatic retest which will recompute the original used MM to best match to some drawdown value nad retest all strategies

Martin

11.09.2020 18:10hankeys

11.09.2020 19:18if i want to normalize the DD to 1000 - i will change the fixedsize for the 1. strat 2x, 2. strat /2, 3. strat /1.5 - simple, why not?

and the same for fixed money - everything i need to do is compute the ratio and make new backtest

Insanity82007

24.11.2020 08:13Attachment Normalise DD chat 1.png added

Attachment Normalise DD chat 2.png added

Attachment Normalise DD chat 3.png added

Attachment Normalise DD chat 4.png added

Attachment Snippets.zip added

Attachment WhatIfBulk.java added

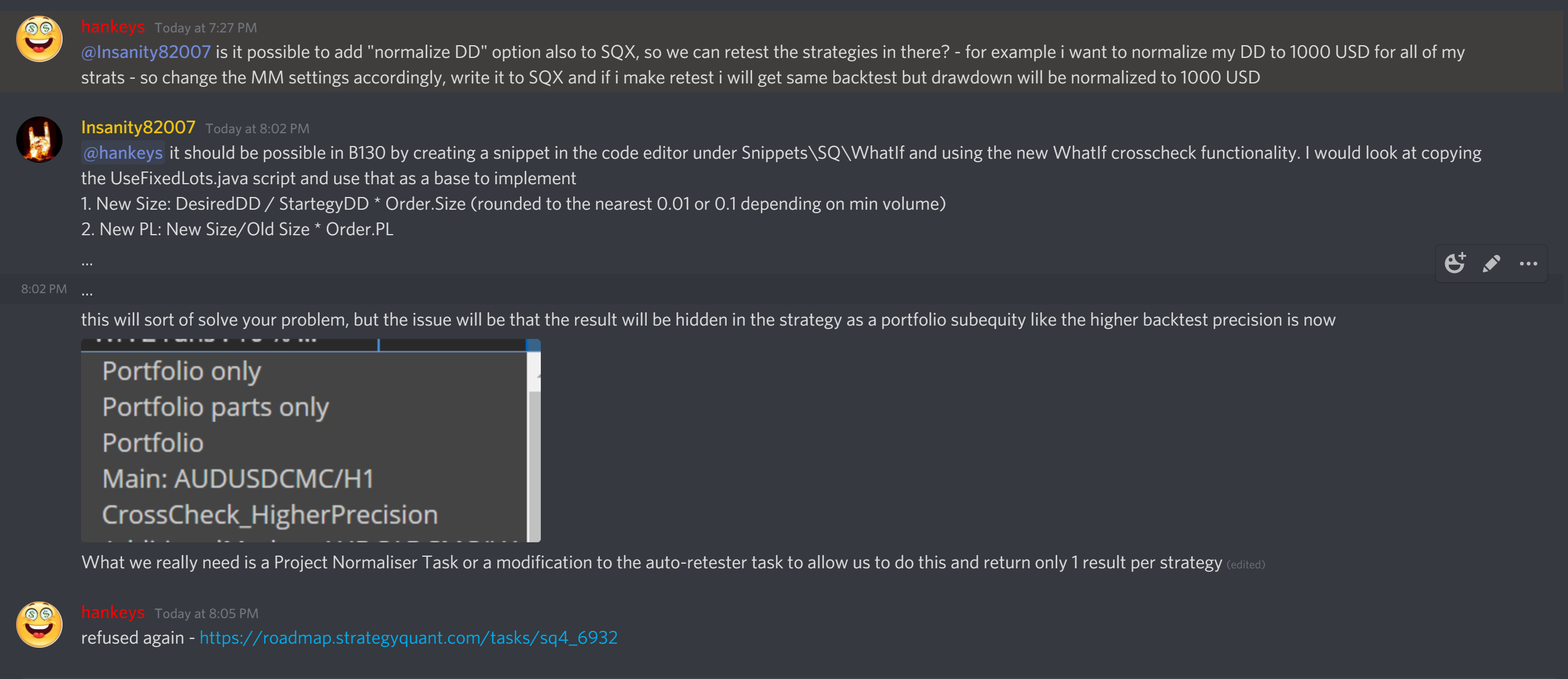

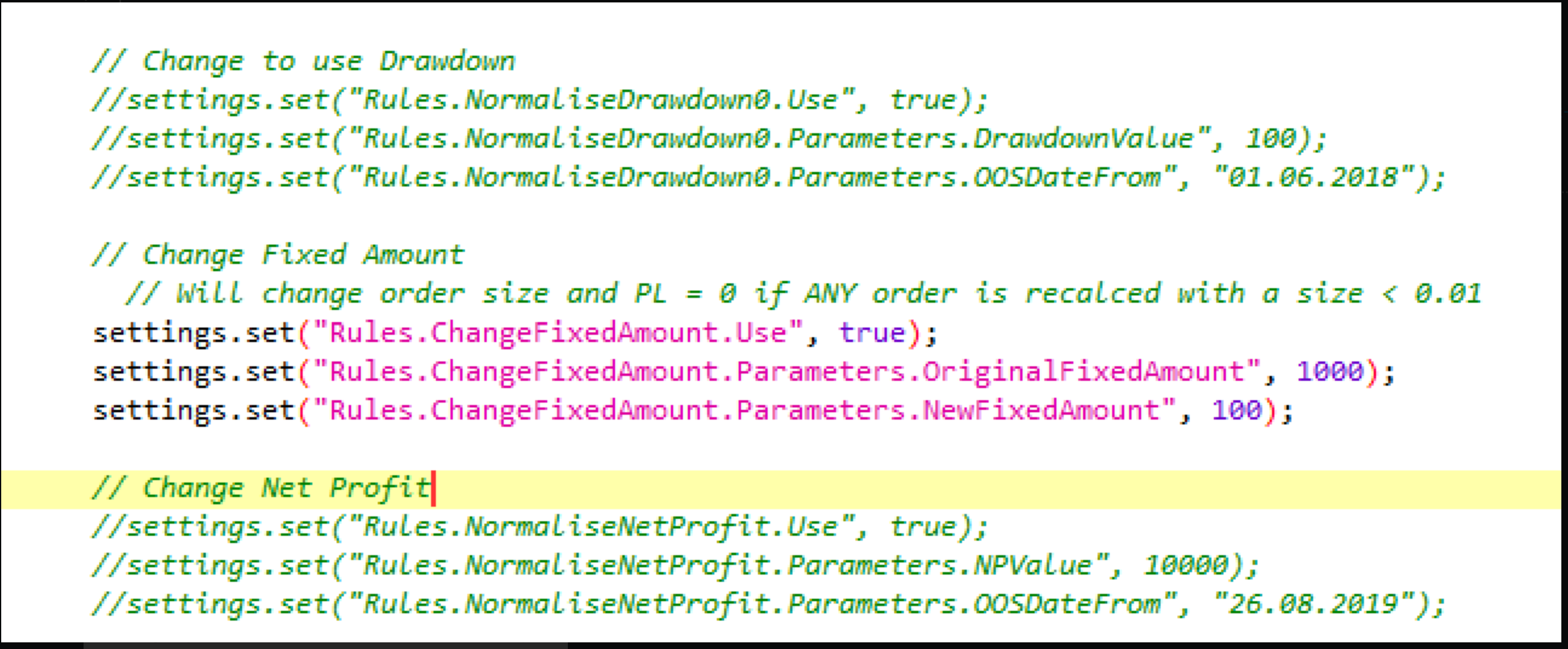

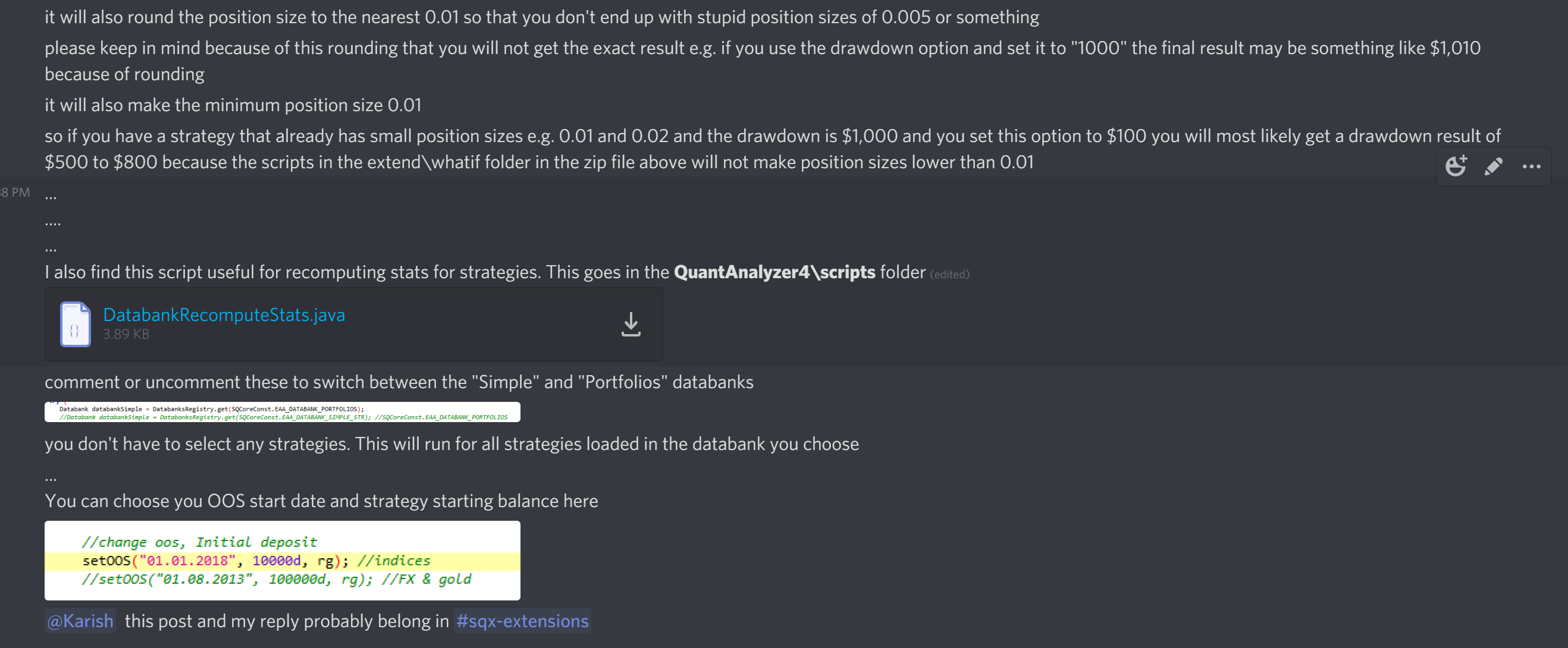

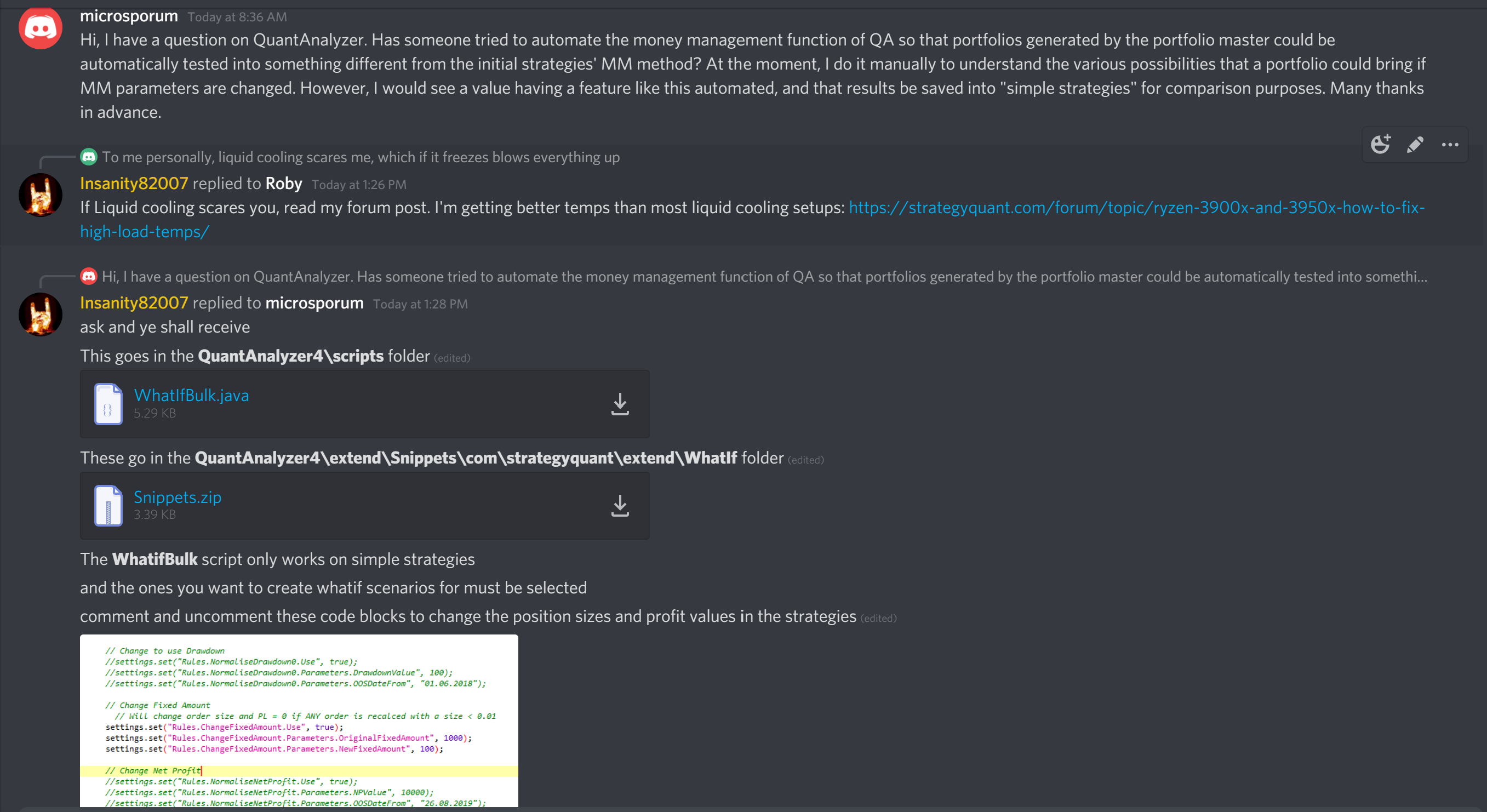

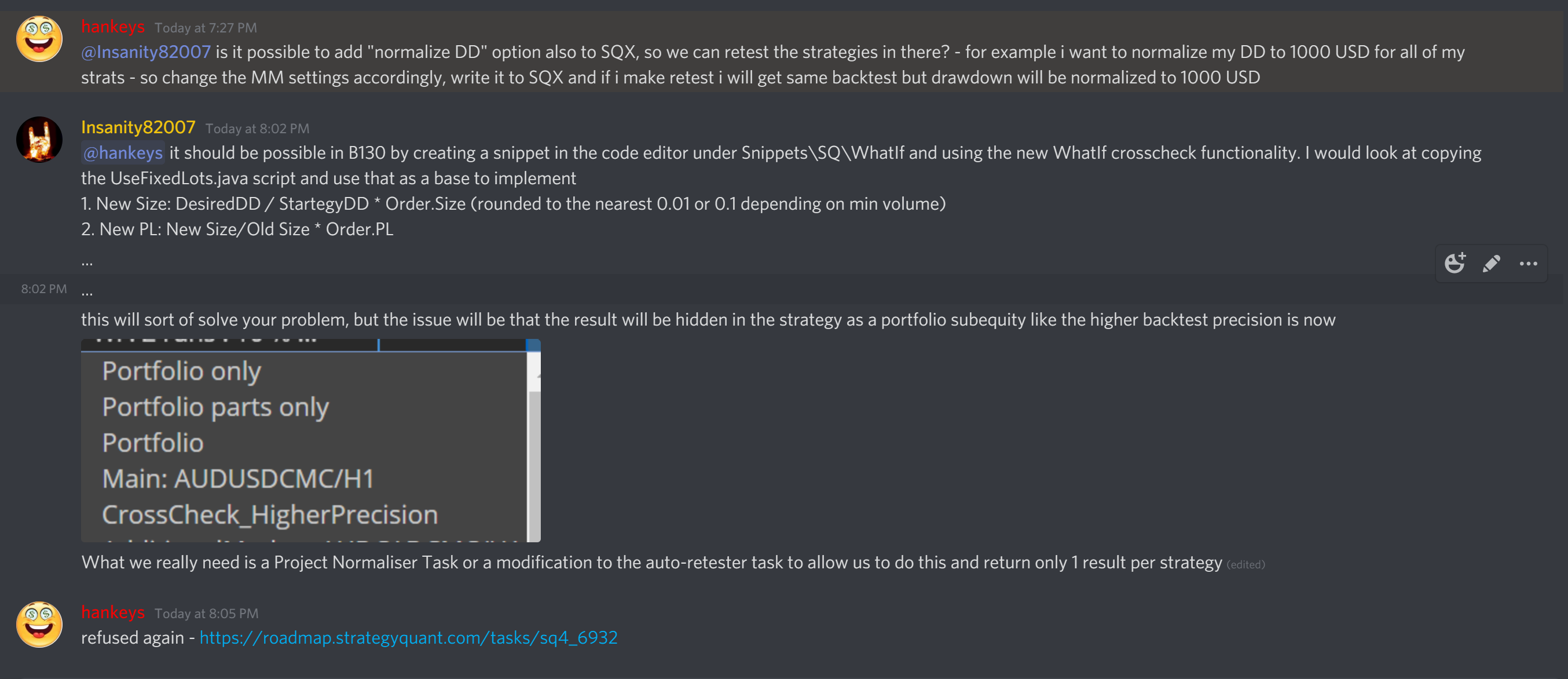

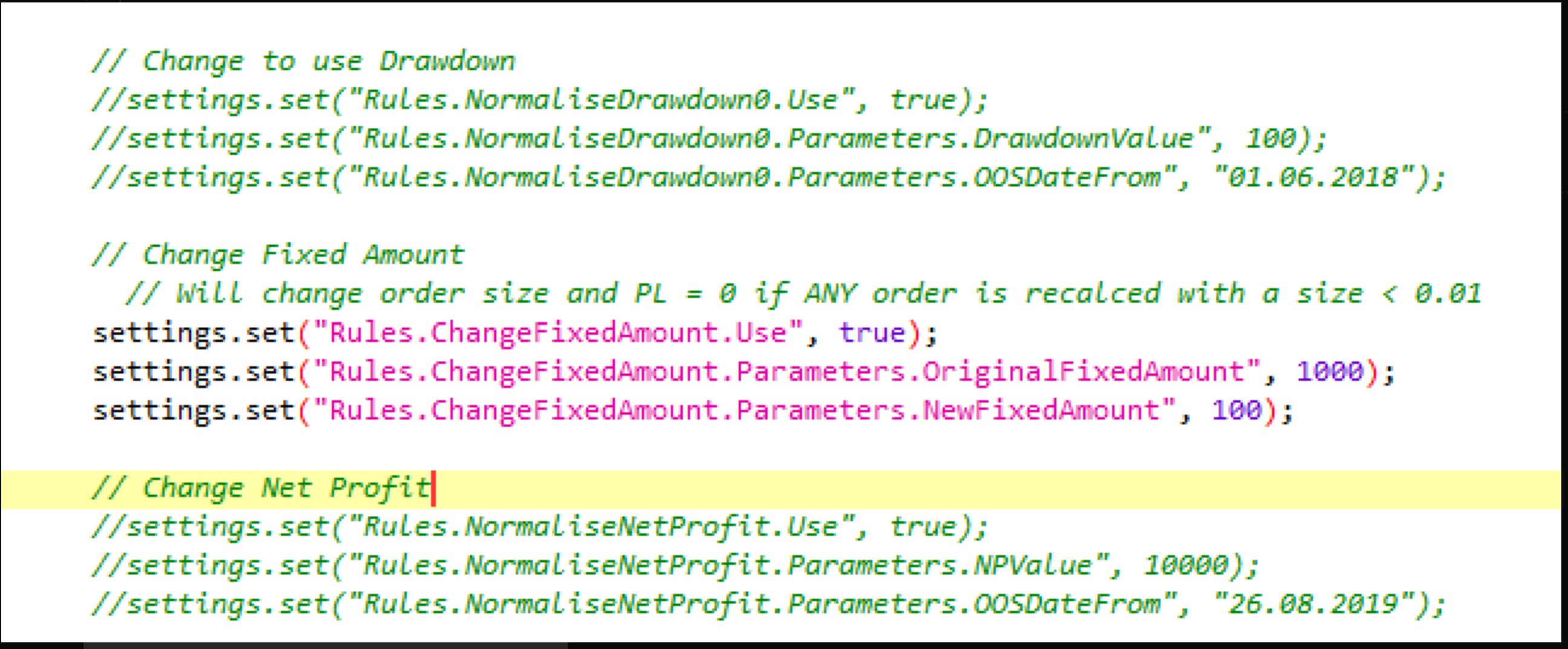

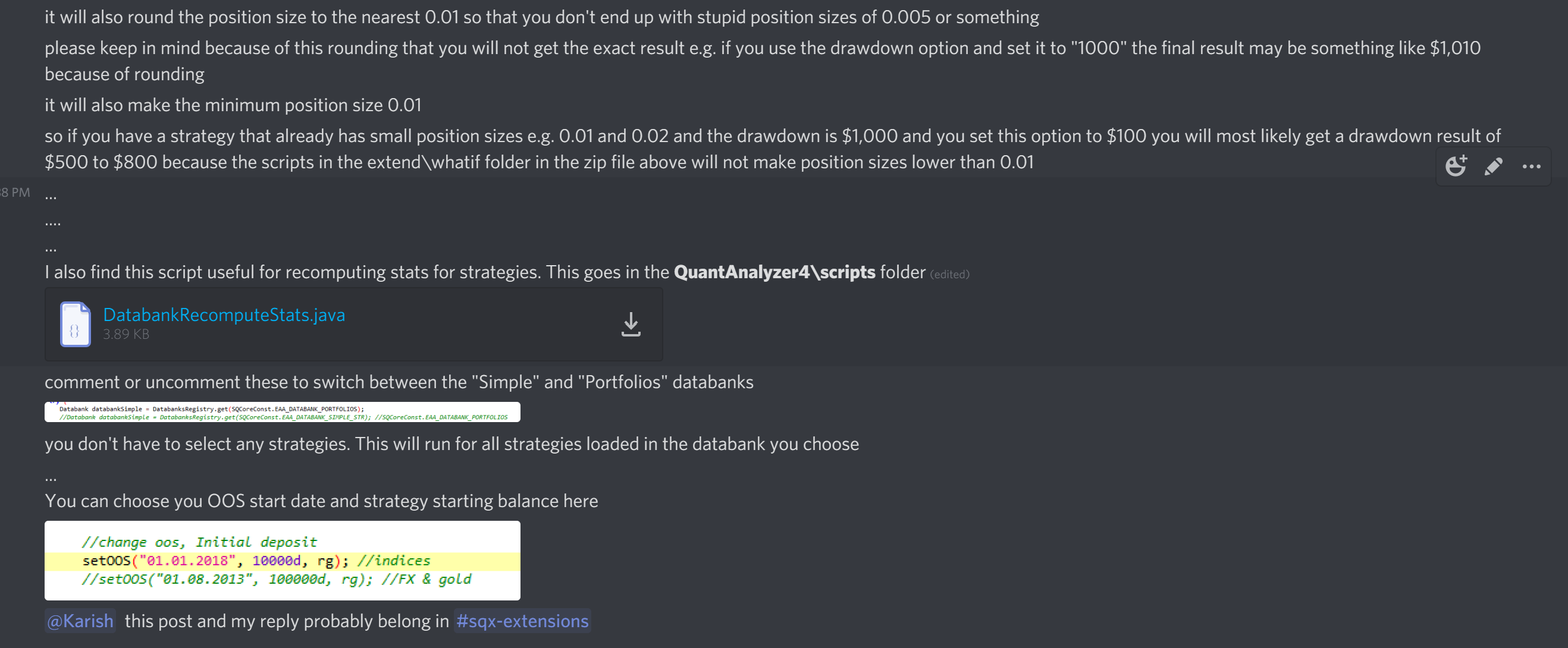

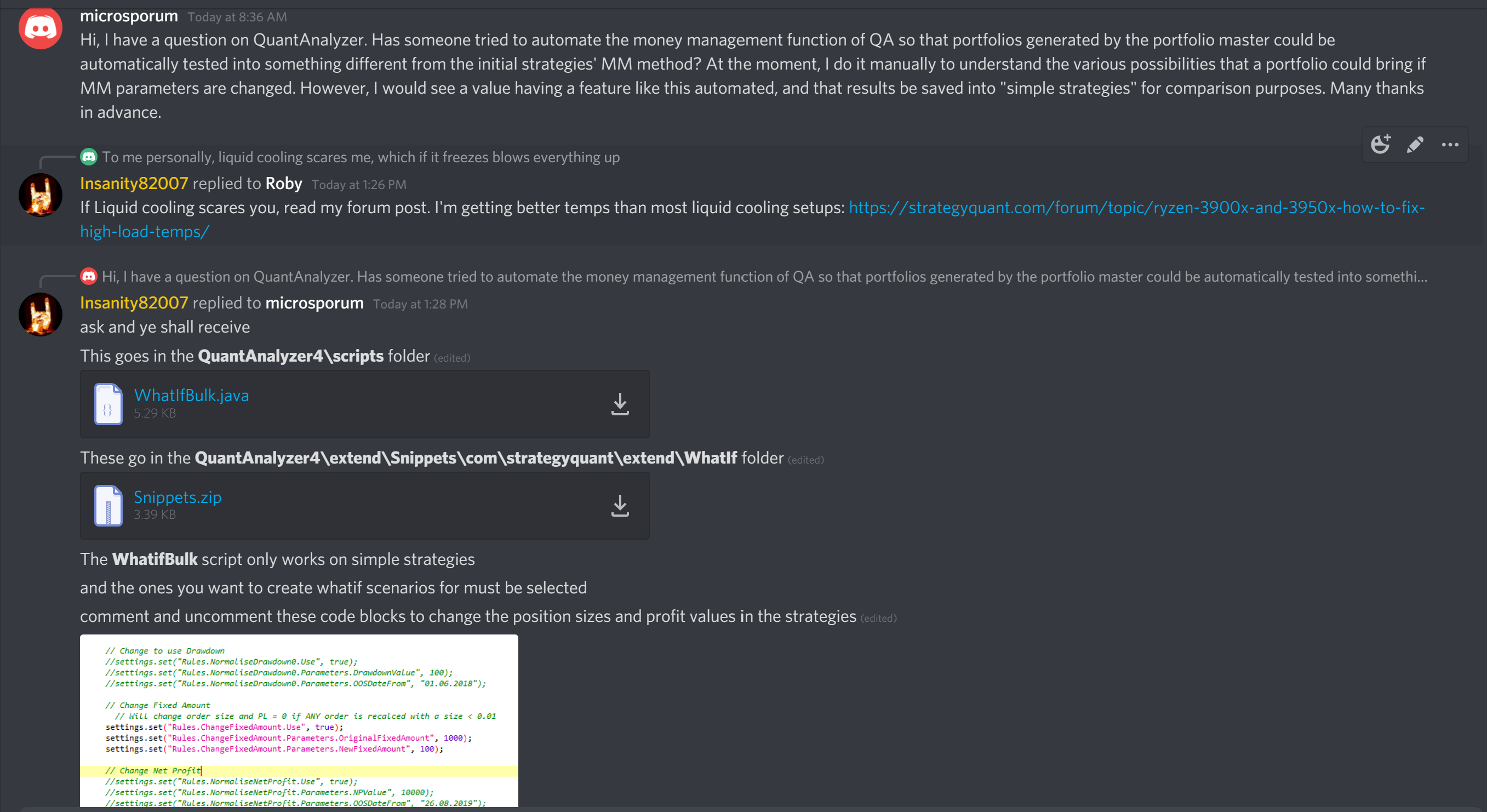

I've already written snippets / scripts that do this in Quant Analyzer (attached).

I've also written VBA code in Excel to modify the exported MQL4 scripts to change the MM settings in each MQL4 file depending on my calculated MM for each normalised strategy.

SURELY this can be done in SQ without too much trouble!

Mark Fric

25.11.2020 09:00Anything can be added to SQ, but I don't see this as a part of SQ core functionality, it should be done by some other tool, or maybe by a custom made plugin.

hankeys

25.11.2020 10:11how many votes and how many users using for example martingale MM which was added some time ago...

Mark Fric

25.11.2020 10:28I don't know any other software developer who listens to their customers as much as we do.

Resources are always limited and there are many other things that we want to develop. I simply think there are bigger priorities than this.

fm663

25.11.2020 13:07bentra

25.11.2020 17:33

Although, maybe it could be calculated and put in the code when this drop down is changed ie a new option here called "from strategy DD." A crude normalizing calc is not hard something like new_risk_size = last_risk_size * (Target_Max_DD/Last_Test_Max_DD)

bentra

25.11.2020 20:48© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}