"Max Global Indicators Period" + "Global Lookback Period (Shift)" & "Reserved Bars (At Trading Options Tab)", No Sense!, They Must Sync!

if i use EMA(400)[10] this means i need even 410 bars to calculate the data.**

-

Votes +1

-

Project StrategyQuant X

-

Type Bug

-

Status Refused

-

Priority Normal

History

Karish

25.09.2020 22:22And Another important thing!,

After some research and testing that i made concerning this issue,

i came to a conclusion,

if i want to build strategies on my whole data that i got for @MES for example: 1997.09.11 ~ 2020.01.01,

And the "Reserved Bars (At Trading Options Tab)" is set to "410",

And the "Max Global Indicators Period" set to "400" & "Global Lookback Period (Shift)" set to "10"

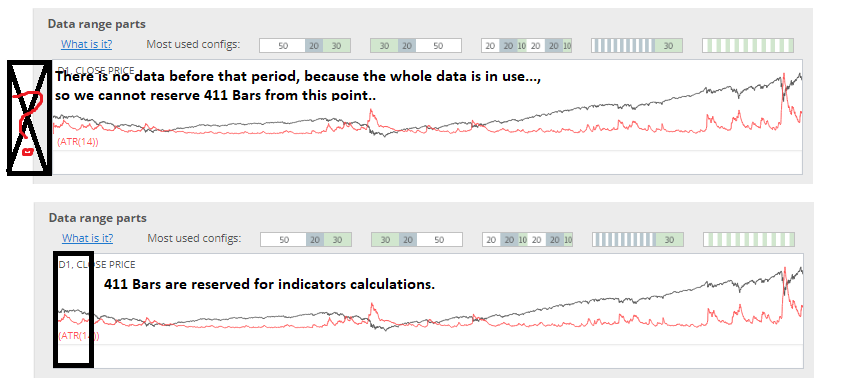

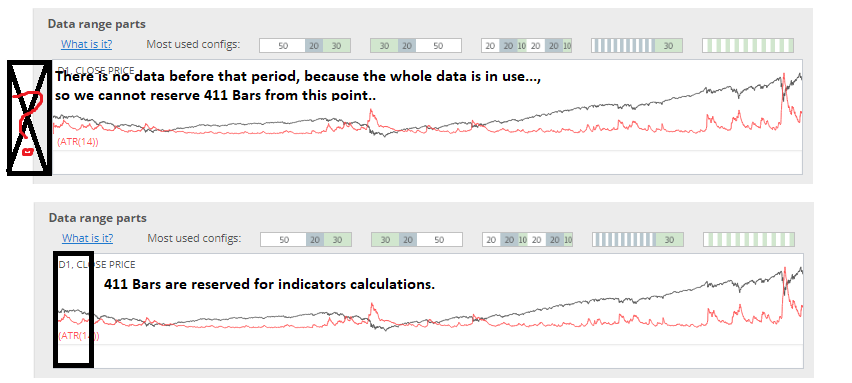

Hence i need 410 reserved bars AT-LEAST in order to calculate the indicator/s for the backtest/retest etc..,

When i build/retest etc my strategies i do not get the same results, I get different results in terms of the equity curve etc..*,

Because i do not have those 410 reserved bars from before the date: 1997.09.11,

which means that i need to reserve those 410 bars manually ahead of time...,

because SQX wont do that by itself....

BUT

When i do this thing instead....:

EXAMPLE:

My whole data is from 1997.09.11 ~ 2020.01.01,

But i will reserve at-least 410 bars now ahead of time,

i dont know what exact date should i begin with but for this example i will use those dates for my building: 2000.01.01 ~ 2020.01.01,

Now i know i got at least 410 bars (Daily Bars) to get accurate results when building/retesting etc..

__

The solution must be as follows:

If the user sets:

"Max Global Indicators Period" to "400" & "Global Lookback Period (Shift)" to "10",

SQX should automatically reserve at-least 410 bars of that same TimeFrame the user is about to build/retest/etc on *(i would say 411 bars in reserve is even better, just in case.),

The "Reserved Bars (At Trading Options Tab)" wont longer be needed from this point on-wards.. because SQX will do everything automatically.

Karish

25.09.2020 22:28

Mark Fric

29.10.2020 10:52Status changed from New to Refused

Moreover, you can want to set reserved bars much bigger than max indicators period

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}