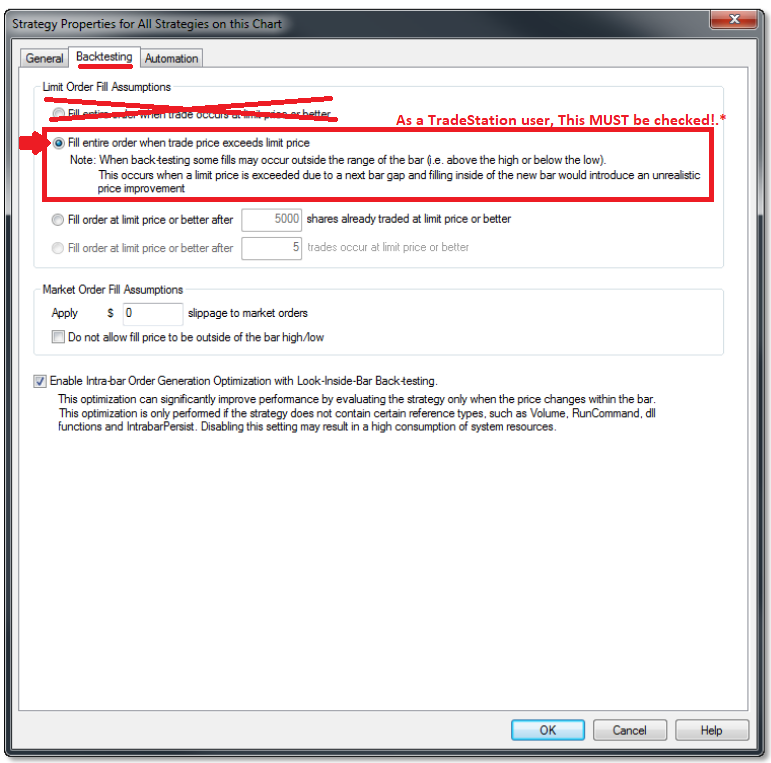

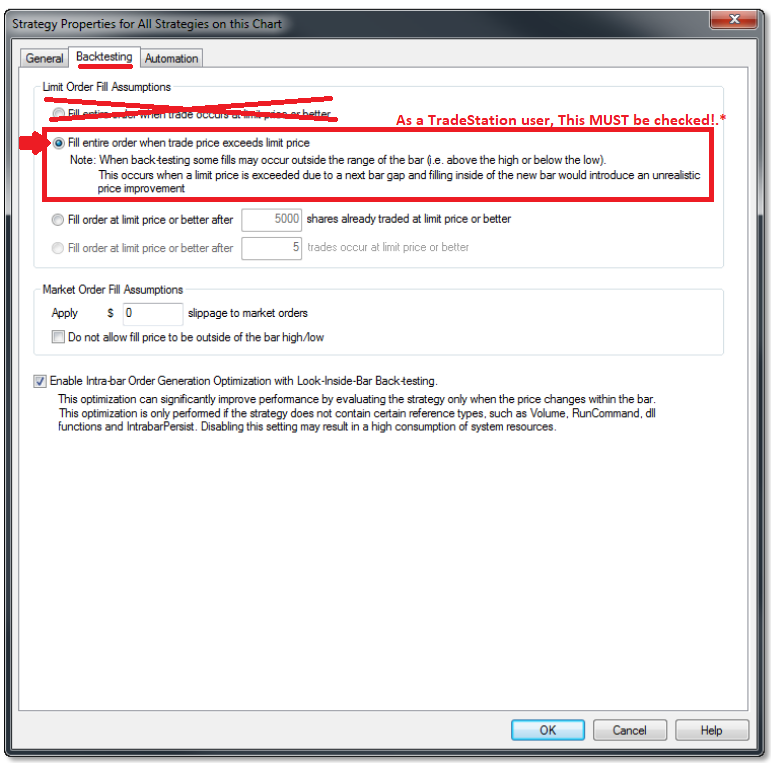

Limit Orders Fill Assumptions (TradeStation like..)

In a historical back-test,a strategy will always assume a perfect fill; market orders are filled immediately at the next available tick and limit orders are filled at the specified limit price. Under real market conditions,this may not always be the case. To provide a more realistic order fill, you may set limit orders to fill only when the limit price has been exceeded.

-

Votes +4

-

Project StrategyQuant X

-

Type Feature

-

Status New

-

Priority Normal

History

mabi

29.09.2020 10:59Karish

29.09.2020 14:51@MABI, If its already built-in thing using TradeStation, it should be integrated to SQ to have similar results in the backtests/forward results.

Besides that SQX's TradeStation Engine must have the same results between both SQX vs TradeStation overall, So it must have a quality backtesting engine that match TS.

Its its not 100% then 110%, because we must achive the same results, thats the whole point of the software anyways, to finds something that we can just export and run on TS or any other execution software,

but if the SQ backtests does not match the TS backtest, something is wrong here,

and if the backtest are wrong, the forward trading results would be wrong as-well, those are just facts.

Karish

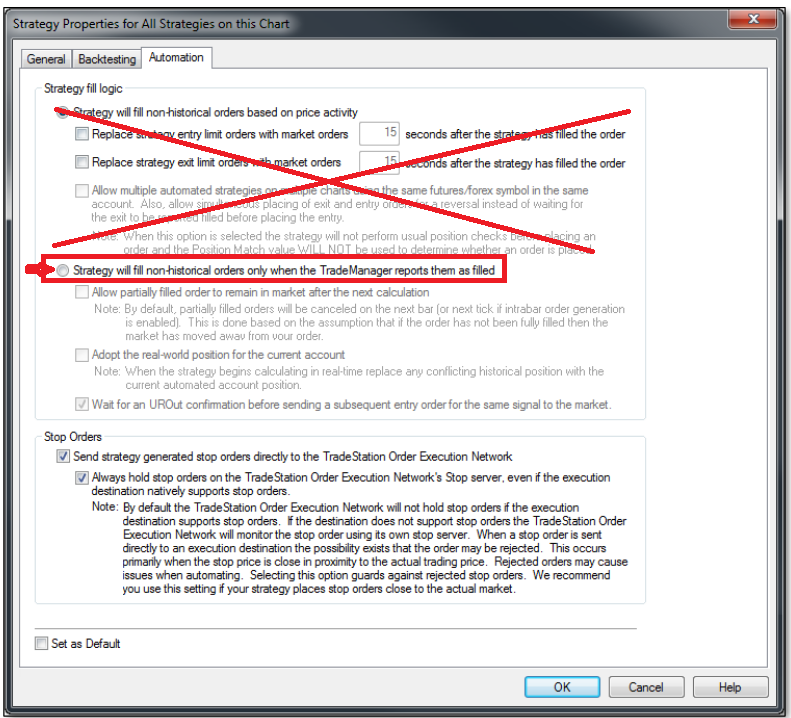

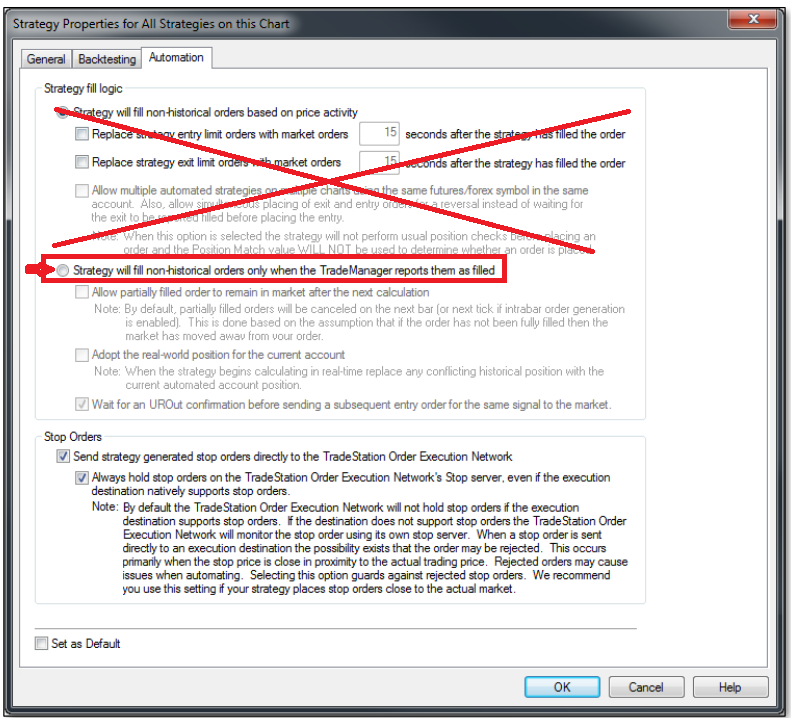

02.10.2020 10:15Attachment Screenshot_1.png added

Attachment Screenshot_2.png added

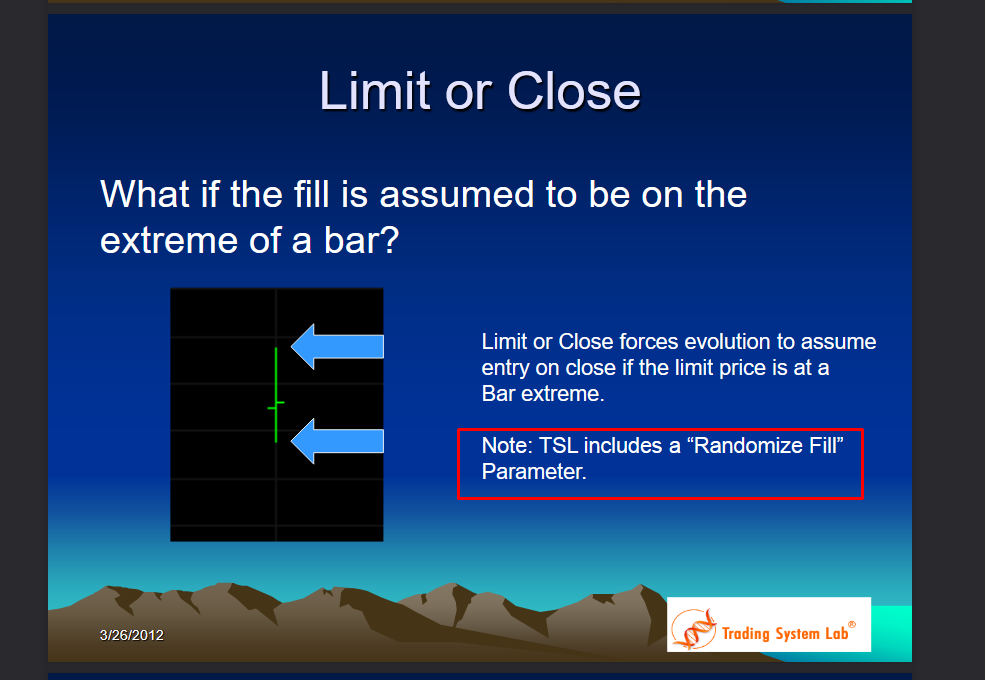

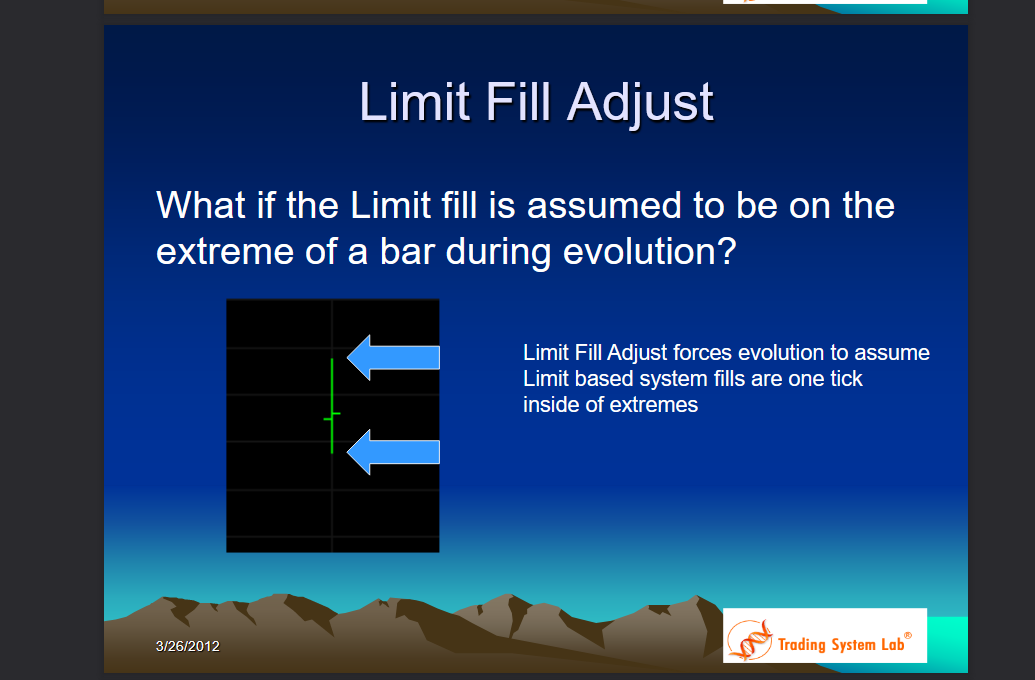

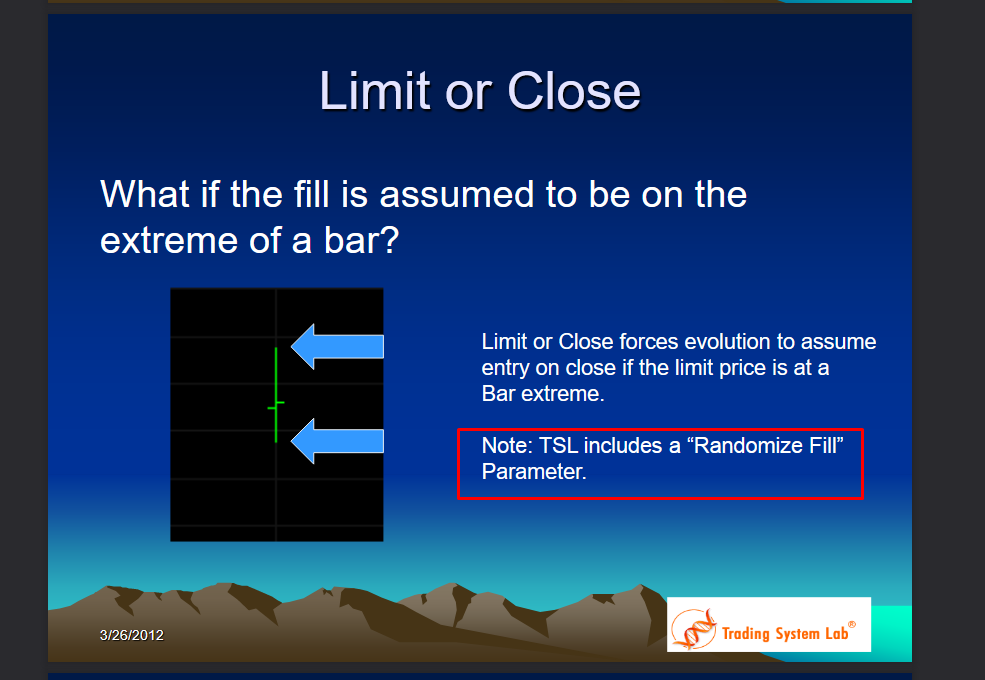

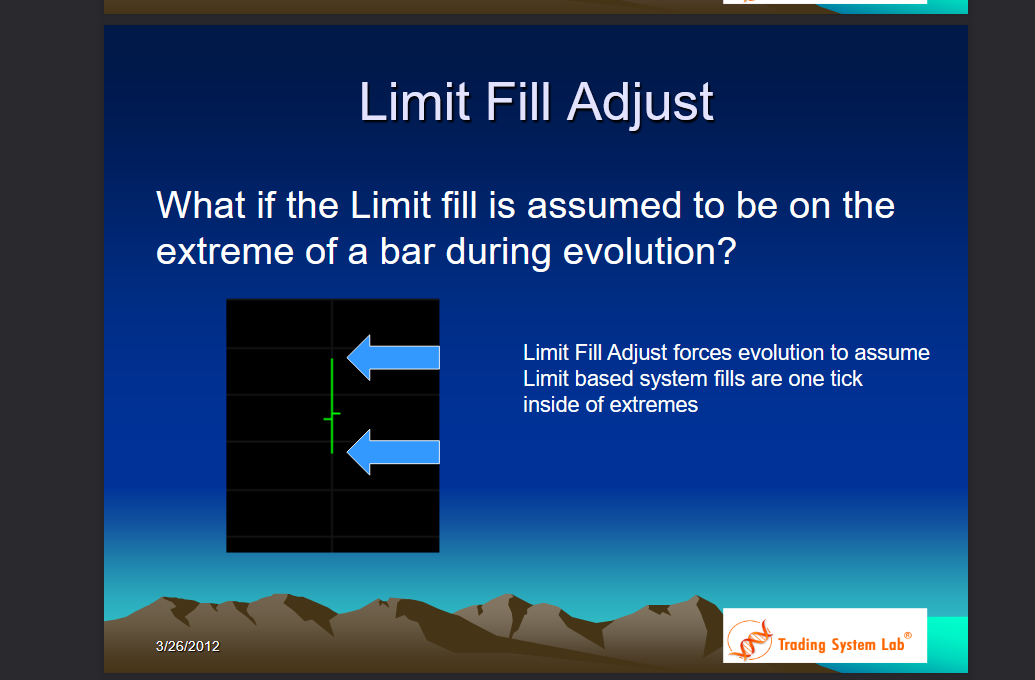

TSL (Alternative to SQX) got it built in to the engine,

Besides that they have some kind of a "Fill Randomization", it seems to be kinda same thing like MonteCarlo's Slippage Randomization maybe..,

Anyway, the point is that SQX's backtesting engine using limit orders mostly fails to show accurate results in the TradeStation Backtester..,

If the SQX Dev team sort out the problem of the synchronization of the backtesters, problem solved.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}