Build 130: Fit to portfolio

The best solution I think is to compute the correlation only for the strategy generated that already passed all the other filter set by the user (profit factor, # of trades....).

-

Votes 0

-

Project StrategyQuant X

-

Type Bug

-

Status Refused

-

Priority Normal

History

hankeys

15.11.2020 14:06Morningbull

15.11.2020 18:19

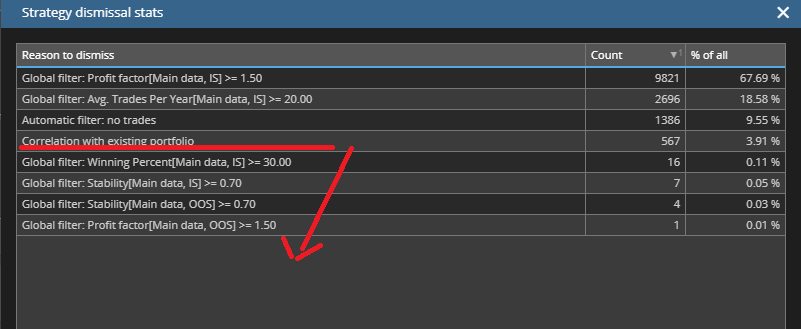

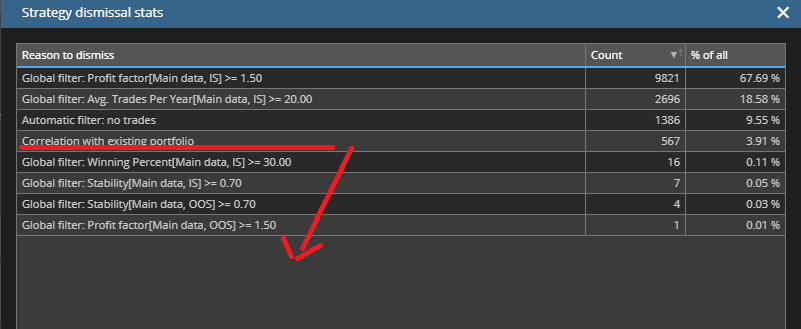

As you can see from dismiss reasons attached, the correlation is computed before of some others (faster) filters, as for example Winning percent or Stability.

To speed up the process I think the correlation should be instead computed at the end of all other filters because it seems to be slower, this modification will not impact in any way the logic of the software.

hankeys

15.11.2020 18:37Tamas

18.11.2020 10:15Status changed from New to Refused

It is not true. First are checked global filters together with auto dismissal rules and then there is a check fitToExistingPortfolio

Morningbull

18.11.2020 21:05hankeys

19.11.2020 10:17Morningbull

19.11.2020 19:06© Copyright. All rights reserved. ProjectPanel.com

{kind=link}