Build to existing portfolio, correlation calculation bug

-

Votes 0

-

Project StrategyQuant X

-

Type Feature

-

Status New

-

Priority Low

History

Mark Fric

26.02.2021 11:16Status changed from New to Waiting for information

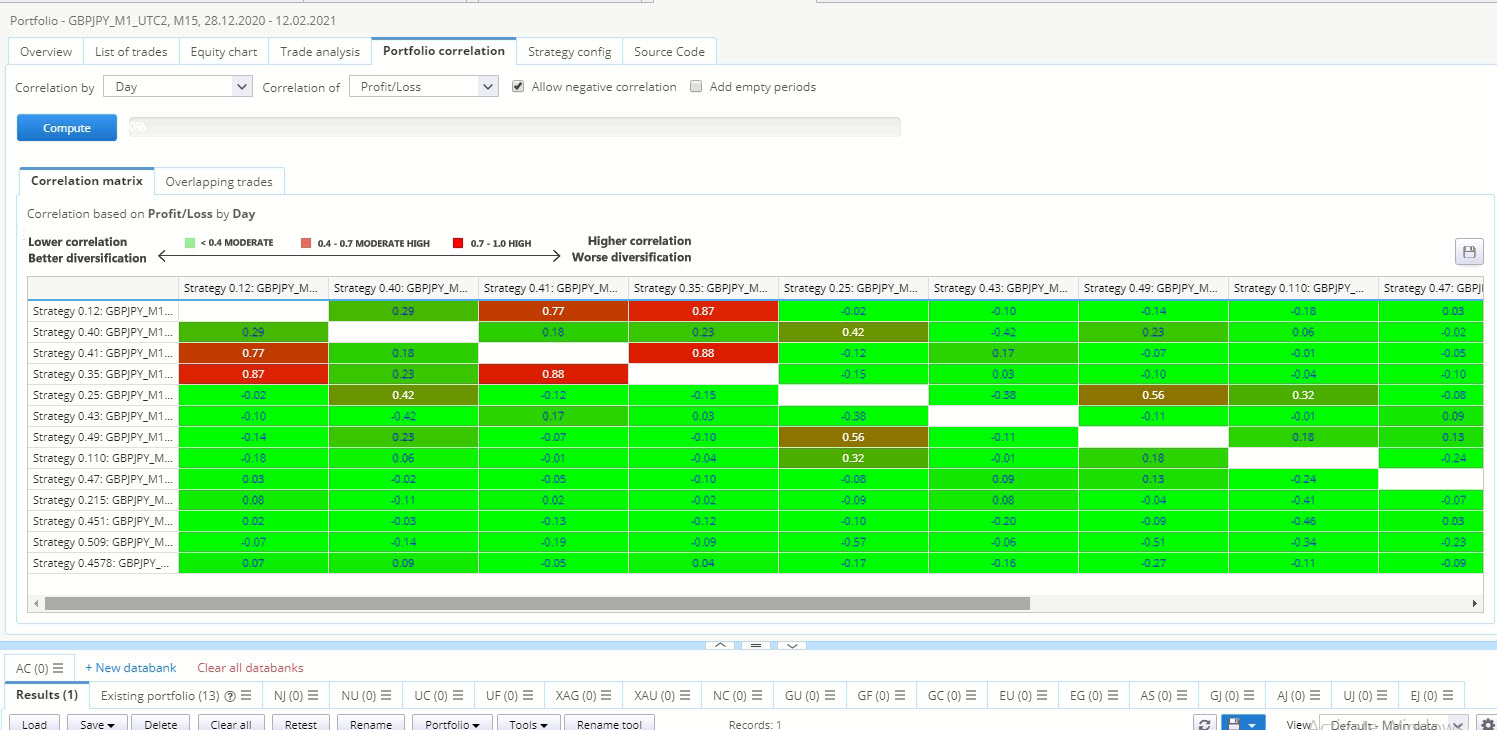

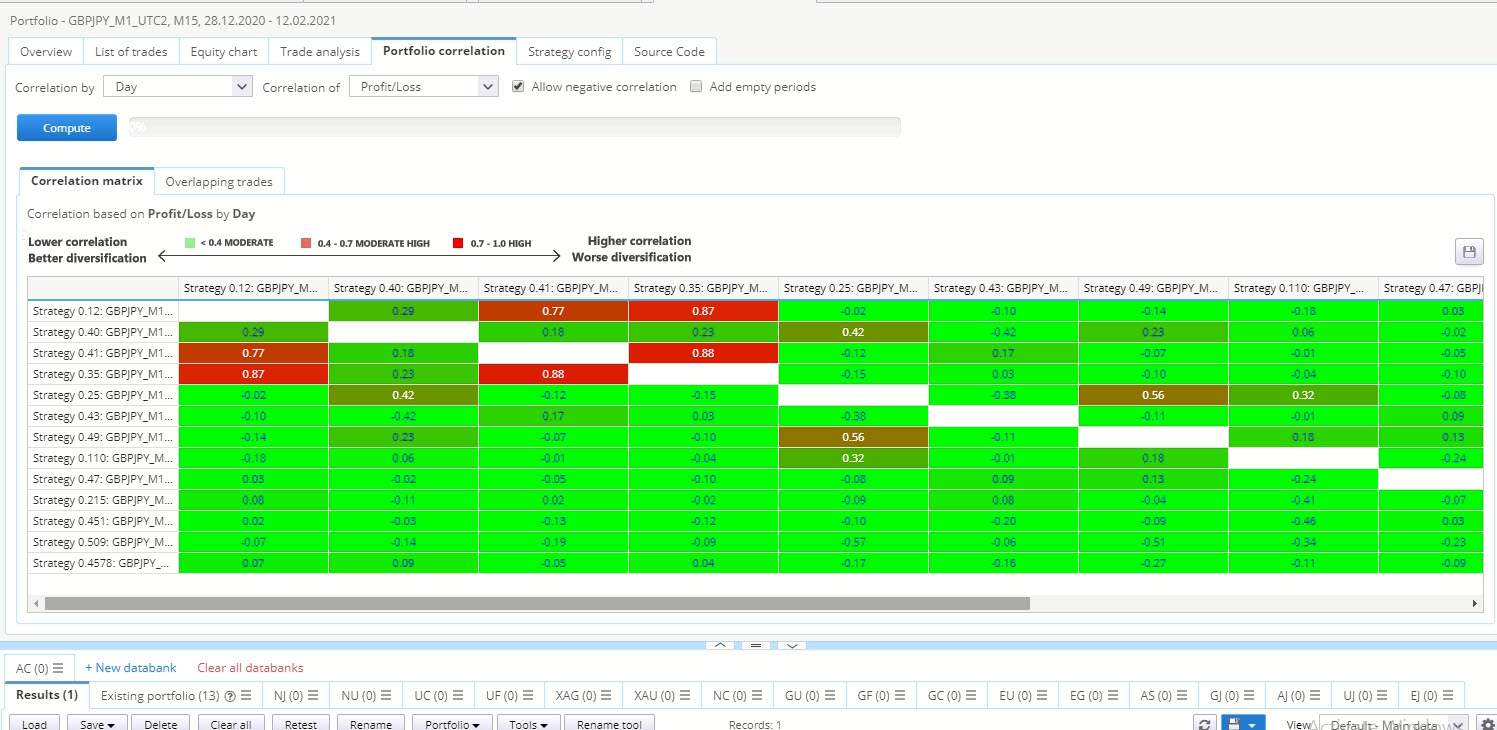

It tests correlation of newly generated strategies with the ones from Existing portfolio databank, not between generated strategies themselves

mabi

26.02.2021 12:12Mark Fric

26.02.2021 13:29Status changed from Waiting for information to Refused

mabi

27.02.2021 01:01

Mark Fric

01.03.2021 12:23Status changed from Refused to Waiting for information

I don't see from your screenshot what is wrong. Fit to portfolio compares generated strategy with strategies in Existing portfolio databank and filters only the generated strategies.

It does nothing with the strategies in Existing portfolio databank.

mabi

01.03.2021 23:57I am also trading them on a real account this week well been doing it for 8 weeks now building new ones evry weekend. And indeed they are very correlated. At the moment i have 3 buy on XAG that are supposed to be uncorrelated all 3 taken within acouple of pips. It is probably better to not rely on this and check the code instead manually.

Mark Fric

02.03.2021 10:41Type changed from Bug to Feature

Status changed from Waiting for information to New

Priority changed from Normal to Low

That's creative, but we didn't intend it to be used this way. It will not work correctly because the existing strategies are cached before the build for quick computation of correlation.

We could make it work, but it is a feature request, and I'm afraid it is low on our list of priorities right now.

mabi

03.03.2021 22:56© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

https://strategyquant.com/doc/strategyquant/fit-strategy-to-existing-portfolio/