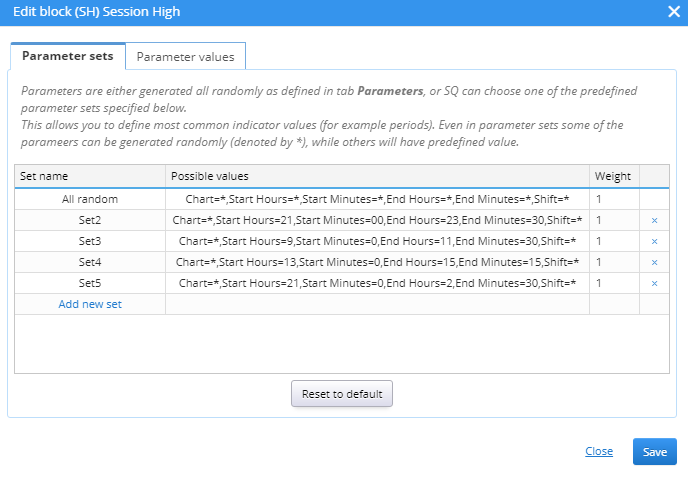

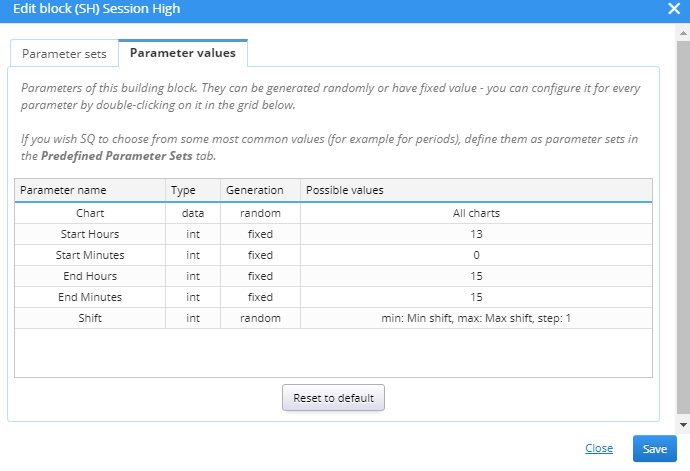

Parameter range set setting does not constrain parameters completely

dev3

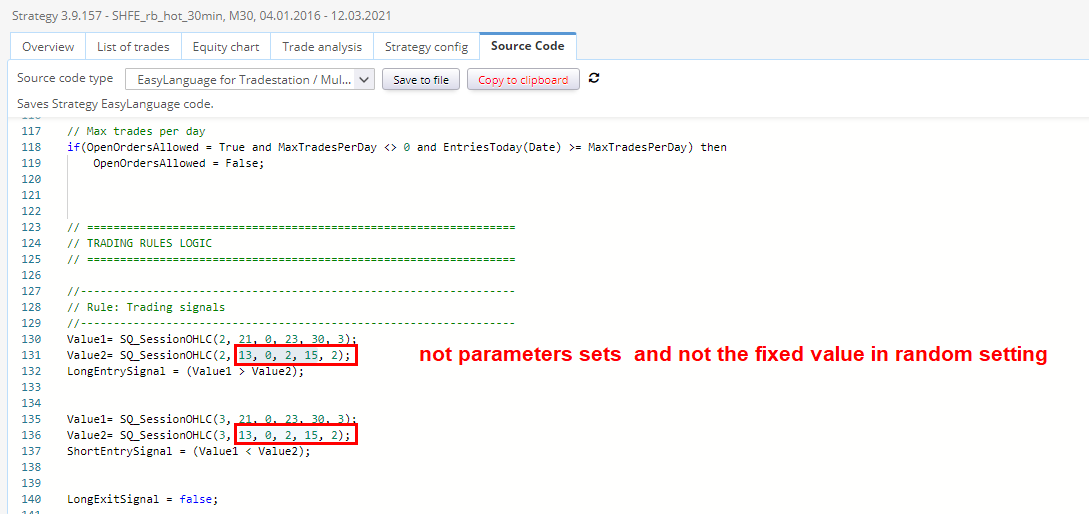

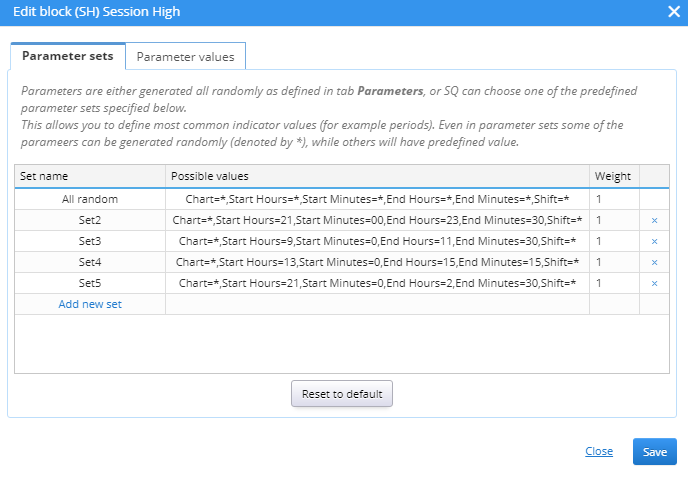

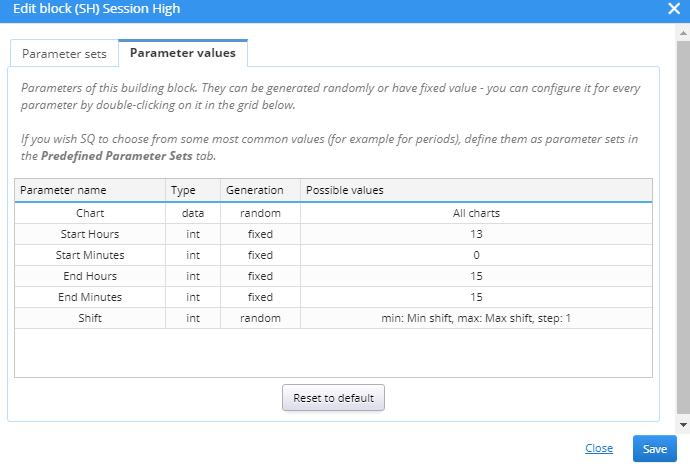

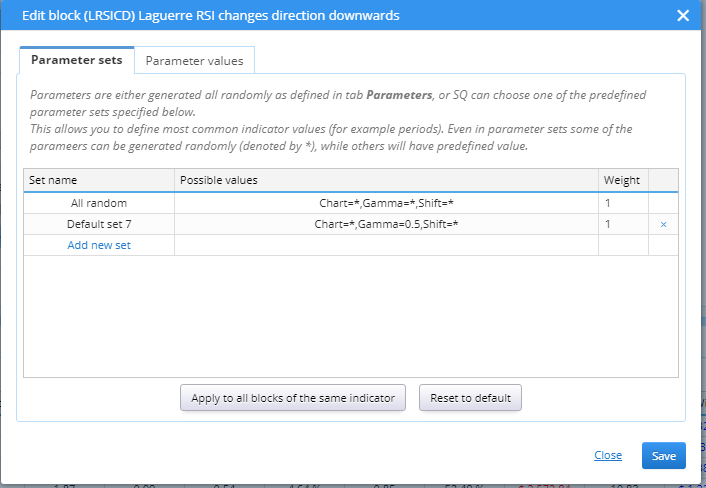

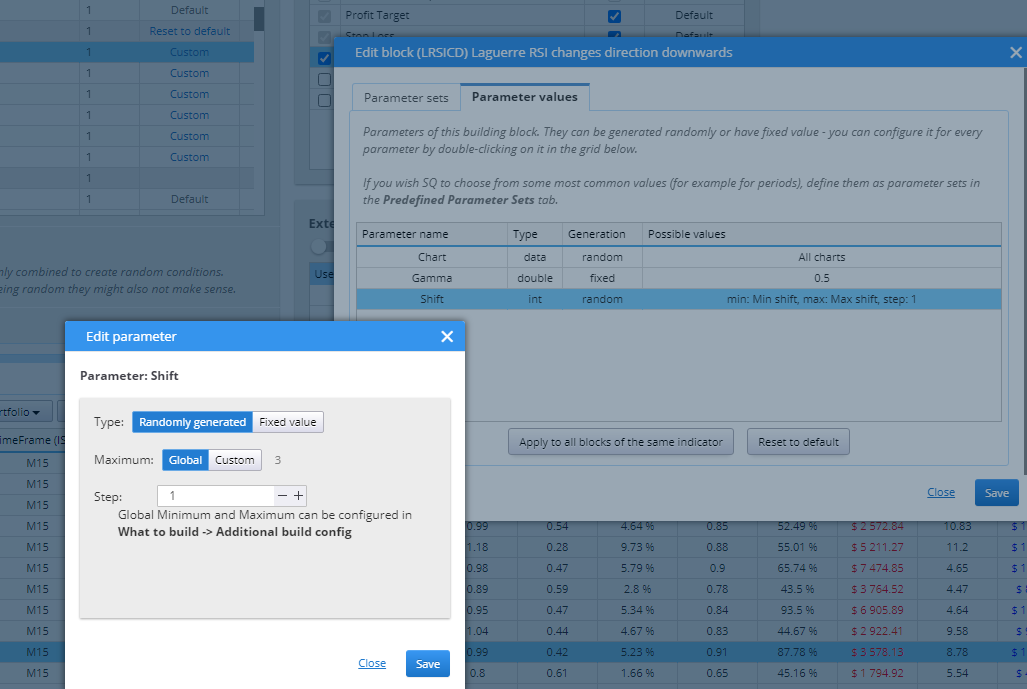

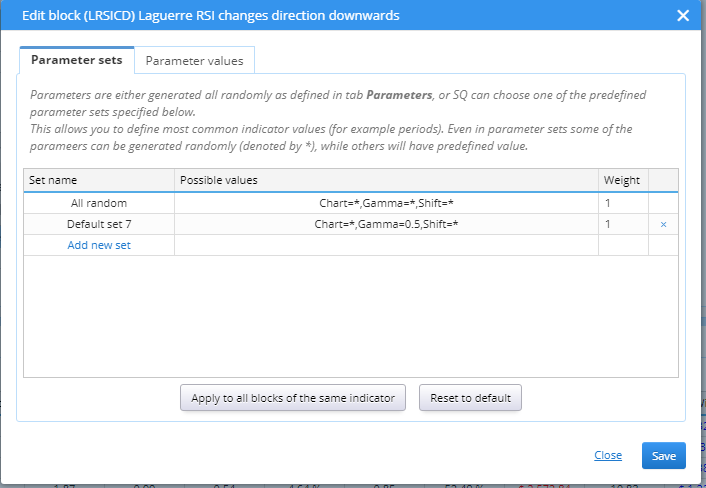

At first, I want to SQ X only pick parameter from the parameter sets, not the random values. But I find no way. So I set the fixed value. picture 2.

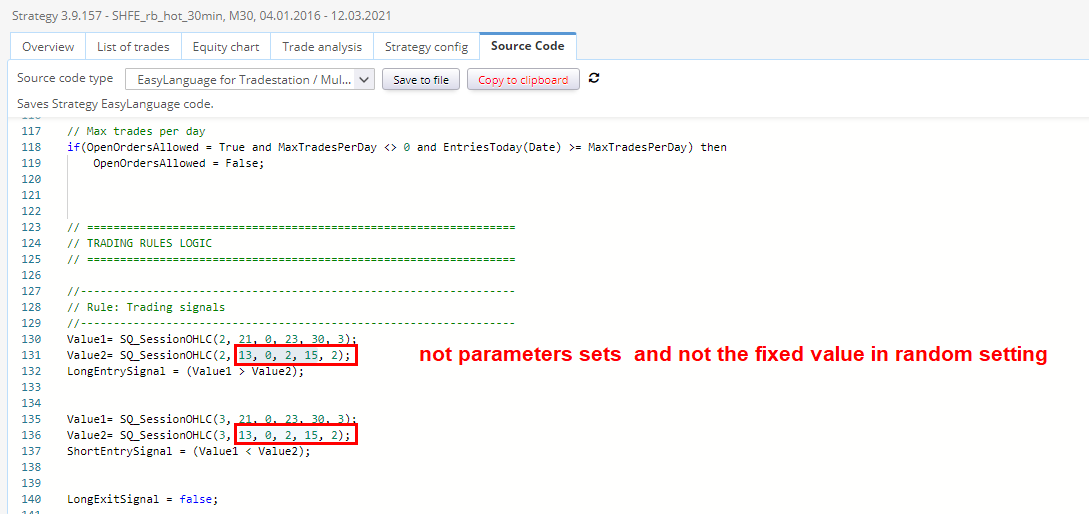

But at last, I found that some parameters are out of the setting.

-

Votes +1

-

Project StrategyQuant X

-

Type Bug

-

Status In progress

-

Priority High

History

eastpeace

16.03.2021 03:03Mark Fric

22.03.2021 12:39Status changed from New to In progress

eastpeace

26.03.2021 13:14Has the issue of session high / low/ close been fixed? I 'm thinking about whether to try dev4.

And I would like to see the session high as indicator showing on the trades charts (trading options). It display HighestInRange, but no session high now.

Thanks.

Mark Fric

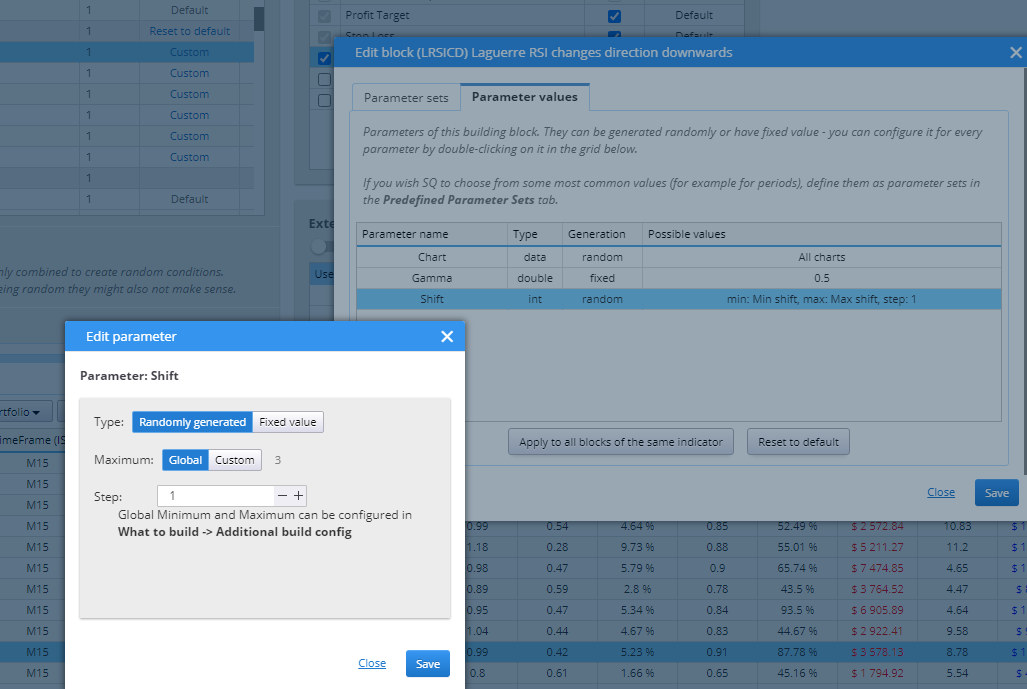

30.03.2021 09:07The problem is in genetic evolution, crossover and mutations don't respect the parameter sets. You'll have it correctly if you'd use Random generation.

eastpeace

31.03.2021 02:05It sounds like a big project, but I believe you and your team can handle it definitely.

The UNION of parameter sets and random parameters is the complete parameter SET for evolution.

Mark Fric

31.03.2021 11:59Priority changed from Urgent to High

So if you want to have it restricetd simply turn crossover to 0.

Mark Fric

31.03.2021 13:18It will have to wait until build 132. For now it will work correctly with Random generation.

eastpeace

28.03.2023 17:10Attachment 2023-03-28 230453.png added

Attachment 2023-03-28 230539.png added

Potential issue/inefficiency with crossover causing various problems - Strategy Quant

[Build 136] not respecting custom parameter levels - Strategy Quant

I found that this issue still exists in B137 dev4, but I remembered the previous feedback. So some related ones.

Some strs in the databank with LRSI parameters,0.6, 0.9 , and I don't want to use those parameters

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Hello, Mark,

There is another similar one.

That is De marker signal. The range of the value should be 0 to 1 according to the formula. And it's right in the default parameter values setting. The level is from 0 to 1, step 0.1.

But SQ always generating some strategy like this,

LongEntrySignal = (DeMarker(Main chart,DEMCrossPeriod)[2] crosses 0.3 downwards); ShortEntrySignal = (DeMarker(Main chart,DEMCrossPeriod)[2] crosses -0.3 upwards);

LongEntrySignal = ((DeMarker(Main chart,DEMPeriod)[3] > 0.4) and (DeMarker(Main chart,DEMPeriod2)[1] > 0.7)); ShortEntrySignal = ((DeMarker(Main chart,DEMPeriod)[3] < -0.4) and (DeMarker(Main chart,DEMPeriod2)[1] < -0.7));

So, there is always no short trades.

And the calibrate indicators may need to be further improved. It give the minimum demarker is 0.29 and the maximum is 0.73.

But I think the range is more appropriate based on the formula, which can avoid the cognitive bias of small data set. And that's for the further testing of other relevant instrument.

And maybe we need set the watershed between for long and short, just like 0 for macd, 50 for rsi, 0.5 for dem. That's is very important when we get the range from the data, not formula.