Strategies that Passes "SeqOpt" after parameters changed shows very different results after a Retest.

after i found some strategies i am using a different task "Optimize" and with the use of "SeqOpt" i am optimizing the strategies,

i notice that now (on build 133) the new stable parameters applied to the strategies that pass the "SeqOpt" optimization,

so thats alright,

BUT!, the problem is that when i take those strategies that pass the "SeqOpt" with the new parameters applied into the "Retest" task,

I retest all those strategies on the same exact settings, data, period, TF, etc, But the results before & after the retest are very odd looking and do not make any sense!

-

Votes +11

-

Project StrategyQuant X

-

Type Bug

-

Status Fixed

-

Priority Urgent

History

Karish

09.07.2021 16:13Karish

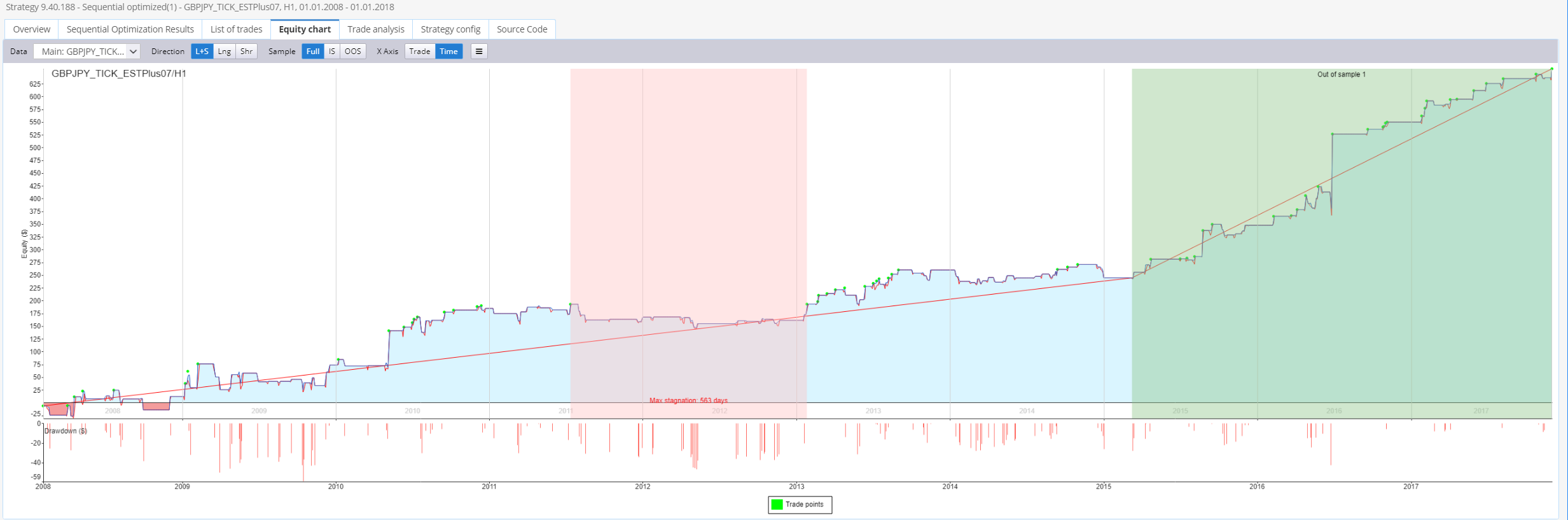

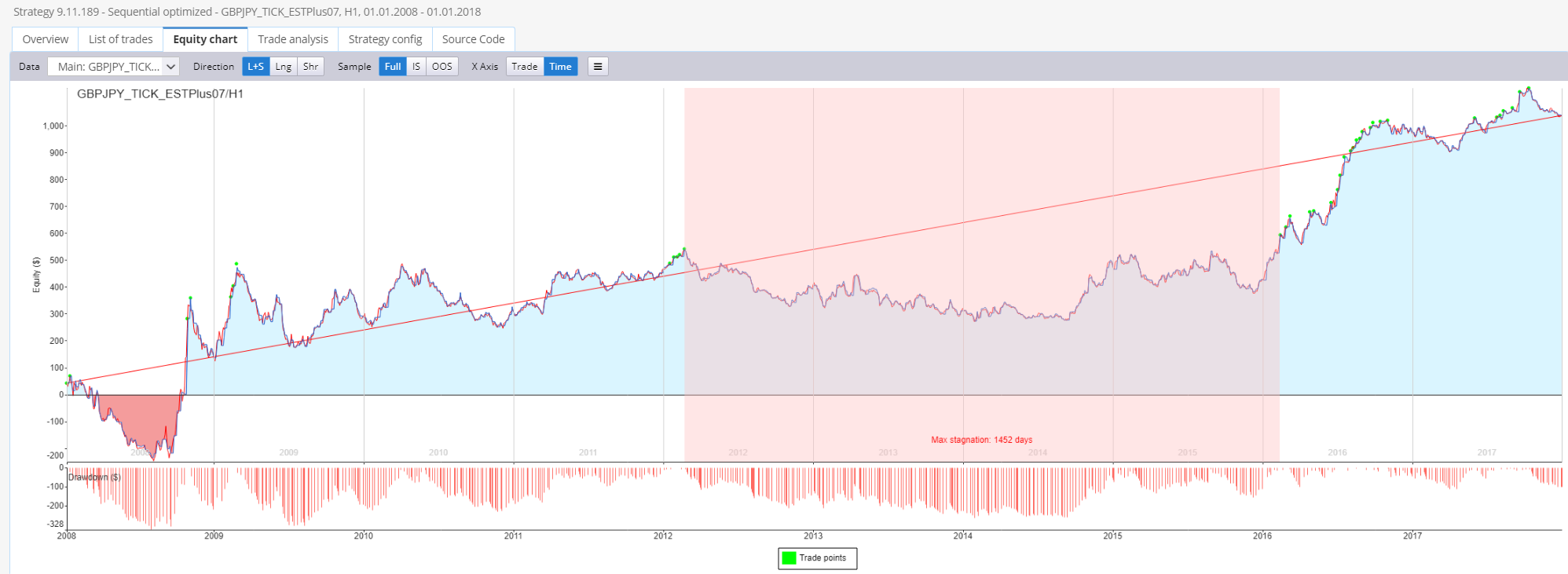

09.07.2021 16:15Attached Screenshot of one of many strategies that got the same problem,

Strategy's SQX file is also attached.

Thanks.. waiting for any reply that confirms if that is a bug or not..

anuffi

27.07.2021 06:42Karish

30.07.2021 14:19From what @Hankeys from Discord "SPP - basic thing doenst work - used params from SPP making totally different backtest"

Please note that one in too..

Mark Fric

09.08.2021 08:34Status changed from New to In progress

Priority changed from Normal to Urgent

What you see in databank in Builder is a result of the first (main) backtest that was performed on an originally generated strategy BEFORE the seq. optimization was performed.

So the main backtest was made on original set of parameters.

If you chose to apply params to strategy in seq. opt. crosscheck config the parameters are changed after the crosscheck, and so when you retest this strategy in Retester the results will be different - because the strategy already has new optimized parameters.

I'm not sure what exactly should be done here - perhaps we should replace the main backtest results with the result of backtest after seq opt change of parameters was applied.

Or, we could accept that it behaves like this, that it is not a bug.

What would you prefer?

Karish

09.08.2021 17:13rather than using the Original Strategy's results after the SeqOpt already applied the new parameters...,

Kinda make sense :) and this is what i thought was buggy.

Karish

09.08.2021 17:20Thats ok, waiting for the new update ASAP......!, its been a long time that i was hand cuffed with it,

cannot continue my projects without it so im kinda stuck currently.., hope you understand, thanks for the reply.

hankeys

10.08.2021 07:25Karish

10.08.2021 11:11I agree with @hankeys about that the SeqOpt feature should respect the "Trading Options" values.

We should checkout the new Beta or the Official release of the new 134 build with the fixed SeqOpt to really make sure it works as it should,

Cause right now on the current build something very odd happens,

How it should really work:

User performs SeqOpt on an Original strategy (*With auto-apply new parameters),

The strategy should show us the updated results not of the Original strategy but rather the results of the UPDATED strategy and it should save the results into that strategy,

like if we take that updated strategy into a re-tester or any other place in SQX the results of the UPDATED strategy should be taken into account,

Currently i dont know why, SQX still takes into account the Original results of the strategy EVEN THOUGH we clearly performed SeqOpt and it did apply the new parameters and showed us the updated results, and after all that if we take that updated strategy into the re-tester and perform a retest it suddenly shows us the results of the Original strategy as if the SeqOpt and the new parameters have not been performed at all...............

And thats a problem.

Karish

10.08.2021 11:15What you see in databank in Builder is a result of the first (main) backtest that was performed on an originally generated strategy BEFORE the seq. optimization was performed.

So the main backtest was made on original set of parameters.

If you chose to apply params to strategy in seq. opt. crosscheck config the parameters are changed after the crosscheck, and so when you retest this strategy in Retester the results will be different - because the strategy already has new optimized parameters.

I'm not sure what exactly should be done here - perhaps we should replace the main backtest results with the result of backtest after seq opt change of parameters was applied.

Or, we could accept that it behaves like this, that it is not a bug.

Mark Fric

10.08.2021 12:21Seq opt in Builder or Retester should be used only as cross check, cross checks should verify only strategy robustness, but they should not modify the original strategy.

Replacing the main result with result after sequential optimization is possible, but it will bring other problems - all cross checks that were performed before Seq. Opt. crosscheck were performed on the original strategy with original parameters. So they are no longer valid if you change parameters in Seq. optimization crosscheck.

To repeat - I think strategy generated in Builder backtest process should be immutable, it shouldn't change in the middle of cross checks.

If you want to perform seq opt on a strategy you should do it later, in step after build.

You can make a simple custom project with a few steps for this, where you configure it the way you want.

As for respecting Trading options - it works as same as all other optimizations. Min/Max SL/PT options are respected during backtest, but they don't influence how your parameters are set in optimization.

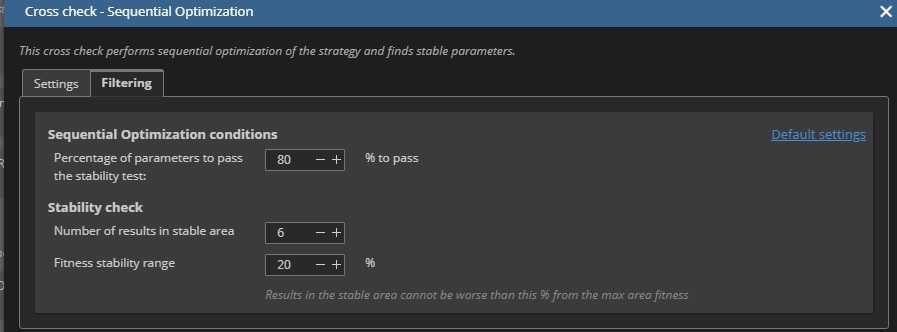

What Seq opt filtering mean - strategy passes if a given % of parameters has stable areas. If parameter has no stable area it means that the results fluctuate very much with every step in the parameter value, which is probably not good. We did not measure yet how good/bad this is as a robustness test, it is something I plan to do.

Look at the doc for better explanation: https://strategyquant.com/doc/strategyquant/sequential-optimization/#how-the-stable-value-of-a-parameter-is-chosen

Karish

10.08.2021 12:38With all the respect @Mark you are wrong on that last reply.

This is non-sense,

All my project depends heavy on SeqOpt and that problem to be fixed,

This is the best way around it:

User use SeqOpt and prompted with 2 choices like it already is right now on build 133 = Auto-apply new parameters (ON/OFF),

• If ON, this WILL change the parameters of the strategy regardless of other things, SQX from now on ALWAYS take into consideration those new parameters and throw out the Original values!.

• if OFF, this WILL NOT change the parameters of the strategy, and the SeqOpt feature will act as a Test rather than a Test & Act.

This will solve the problem.

I dont see a reason why a user that use SeqOpt IN ORDER to find new parameters for his strategy (using Auto-apply new parameters==ON) will take that new strategy with those new updated parameters and make other tests in SQX and SQX will calculate everything based on the Original parameters of that same strategy again..., this is just non-sense!,

Hence if a user chose to use "Auto-apply new parameters=ON" it should do what it should do. (perform as a test & action to change parameters.)

and if the user chose to use "Auto-apply new parameters=OFF" it should do what it should do. (perform just as an test.)

My whole project depends on this fix, and the whole feature purpose of SeqOpt was initially to change parameters of the strategy and continue the development with that new updated strategy parameters in consideration on other steps and tasks.

Mark Fric

10.08.2021 13:55Don't you see what's the problem? Crosschecks are executed one after another, the process is as follows:

1. Strategy is generated and backtested (first, main backtest)

2. (optional) What If simulations crosscheck

3. (optional) MC trades manipulation crosscheck

4. (optional) Higher backtest crosscheck

5. (optional) Additional markets crosscheck

6. (optional) MC Retest crosscheck

7. (optional) Seq. Opt. crosscheck <- here you'll change the strategy parameters in Apply, so points 1.-6. will be no longer valid, because the strategy has changed.

Even if we'll replace the main backtest (point 1.), the rest of them (2.-6.) will be still invalid.

I don't see what kind of project you have that relies on this, but I'd say you are using it incorrectly. You can use Seq. optimization also in Optimizer.

It is simple to create a custom project workflow where you'll first build your strategies, then optimize them, then optionally retest and reevaluate them again.

If you need help with this kind of project I can help you, but I really don't think it should change the way you want in crosscheck.

I'm looking forward to see what others think about this.

Karish

10.08.2021 14:14But what if the work flow is something along those lines:

1. Strategy is generated and backtested (first, main backtest)

2. (optional) Seq. Opt. crosscheck

3. (optional) What If simulations crosscheck

4. (optional) MC trades manipulation crosscheck

5. (optional) Higher backtest crosscheck

6. (optional) Additional markets crosscheck

7. (optional) MC Retest crosscheck

In simple words, we created a strategy, we used SeqOpt we used Auto Apply new parameters, now we got a new strategy with new parameters that we want to continue those following steps with it:

3. (optional) What If simulations crosscheck

4. (optional) MC trades manipulation crosscheck

5. (optional) Higher backtest crosscheck

6. (optional) Additional markets crosscheck

7. (optional) MC Retest crosscheck

BUT!, the problem is that SQX will IGNORE the new parameters EVEN THOUGH the new parameters clearly applied to the strategy (Check "Source Code" Tab you will see those new parameters),

so SQX will IGNORE the new parameters and keep on using the Original parameters rather than the new parameters of that strategy,

so all those following tasks:

3. (optional) What If simulations crosscheck

4. (optional) MC trades manipulation crosscheck

5. (optional) Higher backtest crosscheck

6. (optional) Additional markets crosscheck

7. (optional) MC Retest crosscheck

Are IRRELEVANT!

Mark Fric

10.08.2021 14:22If you want to do it in the order you explained then why don't you do it in custom project?

Task 1 - Build, no crosschecks

Task 2 - Optimize with Seq Opt

Task 3 - Retest, apply all the remaining crosschecks on strategies with Seq Opt optimized parameters

You have no option to change the order of crosschecks in Builder, and I don't think it is a good idea to put Seq. Opt. As a relatively slow crosscheck to the first place.

Karish

10.08.2021 14:24Again, Like i mentioned here on post #24: https://roadmap.strategyquant.com/tasks/sq4_8212/edit#comment-94132

The very simple solution to this problem should be a selection that will consider the following:

• Apply new parameters to the strategy.

• DO NOT apply new parameters to the strategy.

If the user will select ("Apply new parameters to the strategy.") the following will happen:

1. Strategy is generated and backtested (first, main backtest)

2. (optional) Seq. Opt. crosscheck

3. (optional) What If simulations crosscheck **Taking the Parameters into account rather than the Original Parameters.

4. (optional) MC trades manipulation crosscheck **Taking the Parameters into account rather than the Original Parameters.

5. (optional) Higher backtest crosscheck **Taking the Parameters into account rather than the Original Parameters.

6. (optional) Additional markets crosscheck **Taking the Parameters into account rather than the Original Parameters.

7. (optional) MC Retest crosscheck **Taking the Parameters into account rather than the Original Parameters.

8. (optional) Retests etc........... **Taking the Parameters into account rather than the Original Parameters.

-------------------------------

If the user will select ("DO NOT apply new parameters to the strategy.") the following will happen:

1. Strategy is generated and backtested (first, main backtest)

2. (optional) Seq. Opt. crosscheck

3. (optional) What If simulations crosscheck **Original Parameters.

4. (optional) MC trades manipulation crosscheck **Original Parameters.

5. (optional) Higher backtest crosscheck **Original Parameters.

6. (optional) Additional markets crosscheck **Original Parameters.

7. (optional) MC Retest crosscheck **Original Parameters.

8. (optional) Retests etc........... **Original Parameters.

Simple as that, It should like so already in this current 133 build,

Problem solved........

Waiting for your confirmation Mark, Thanks.

Karish

10.08.2021 14:27I got you, but the order of crosschecks is the way I wrote it, it cannot be changed. It is ordered from fastest to slowest.

If you want to do it in the order you explained then why don't you do it in custom project?

Task 1 - Build, no crosschecks

Task 2 - Optimize with Seq Opt

Task 3 - Retest, apply all the remaining crosschecks on strategies with Seq Opt optimized parameters

You have no option to change the order of crosschecks in Builder, and I don't think it is a good idea to put Seq. Opt. As a relatively slow crosscheck to the first place.

Ill check it again and give you my feedback, i remember i tried many ways, give me few minutes..

Karish

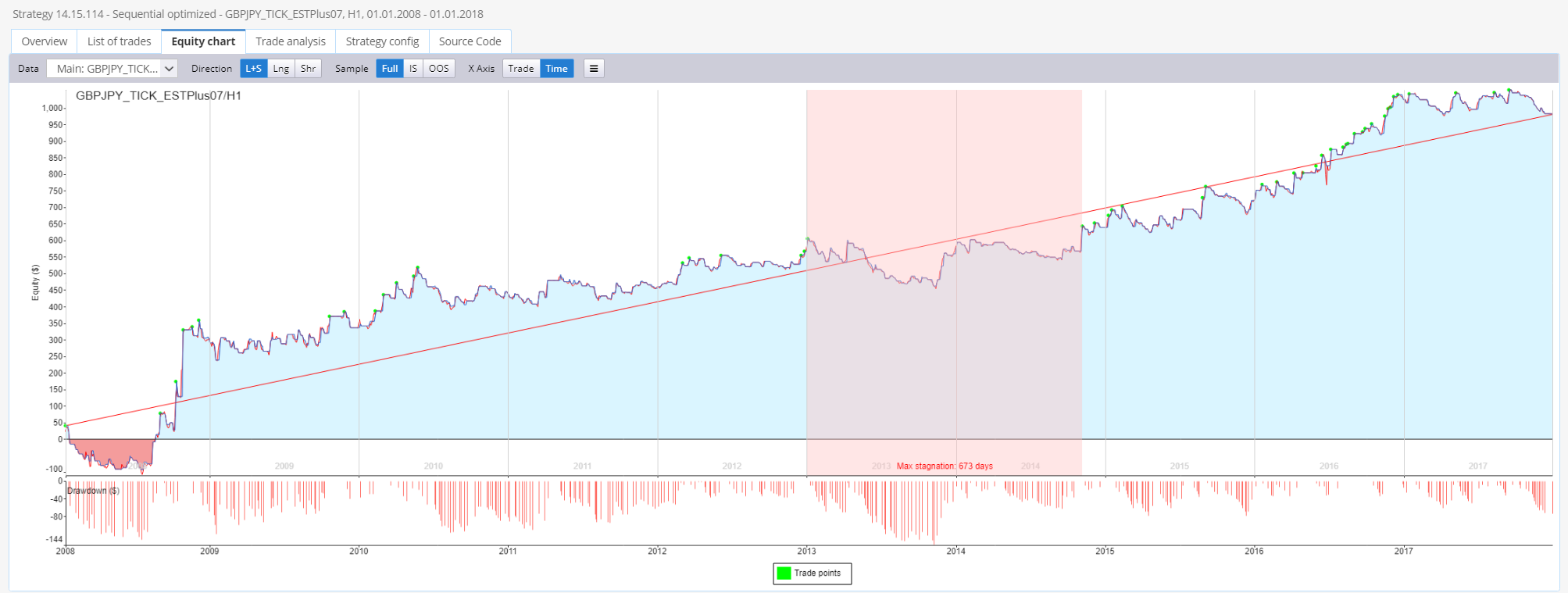

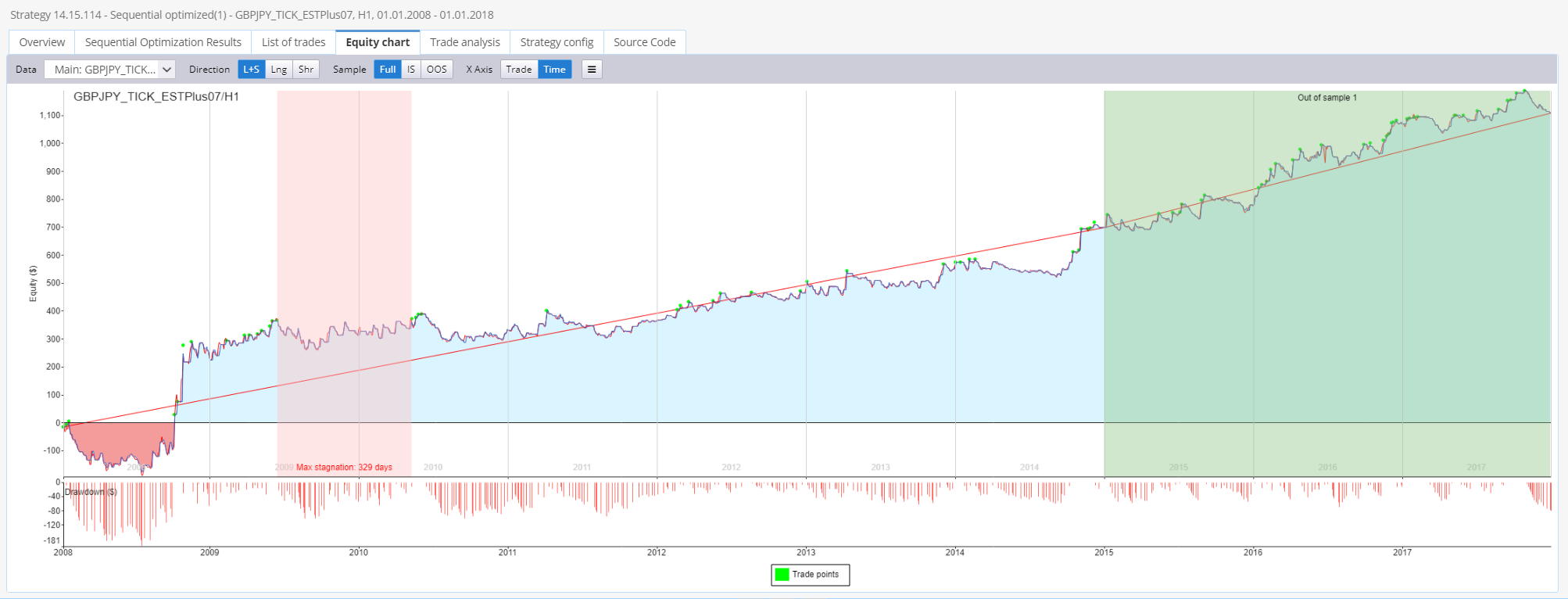

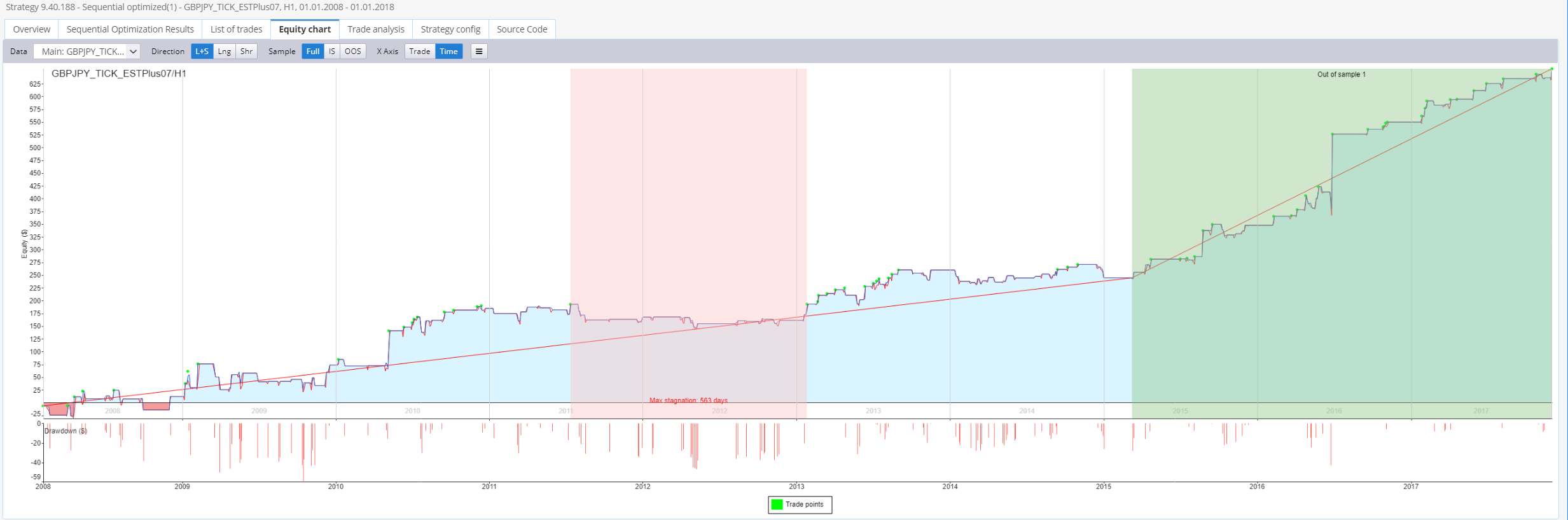

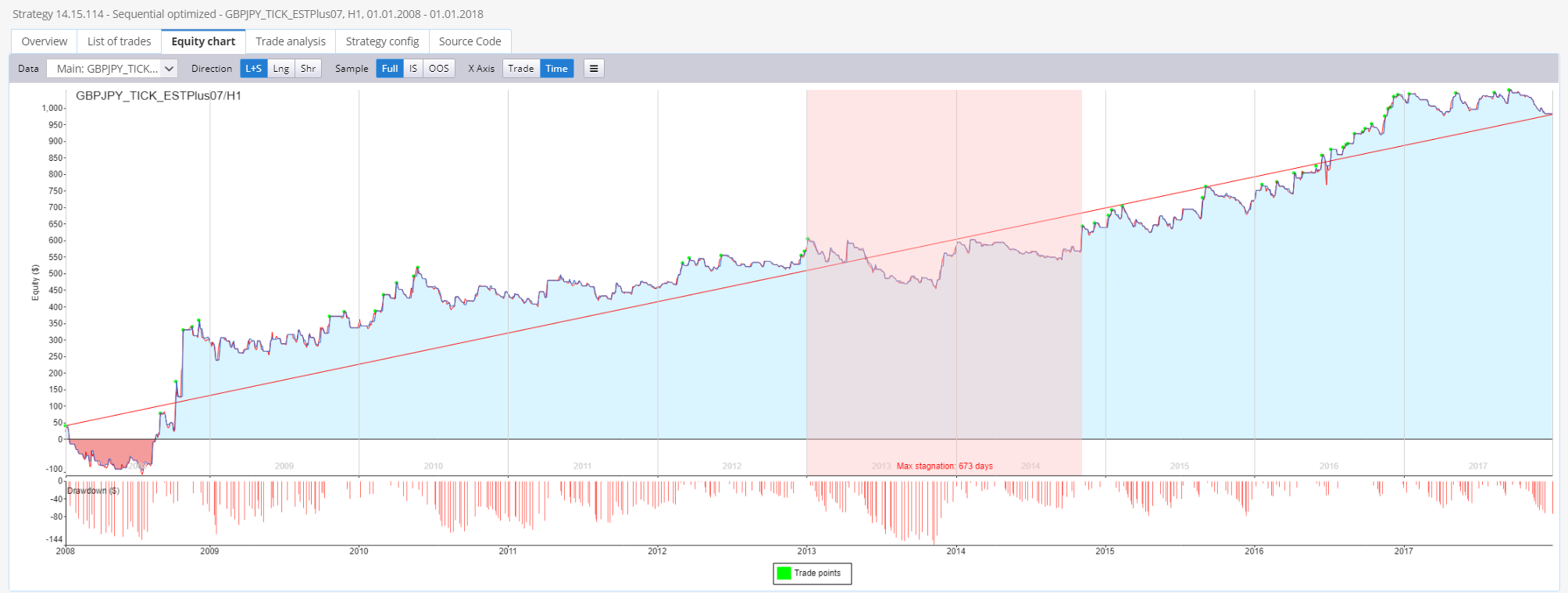

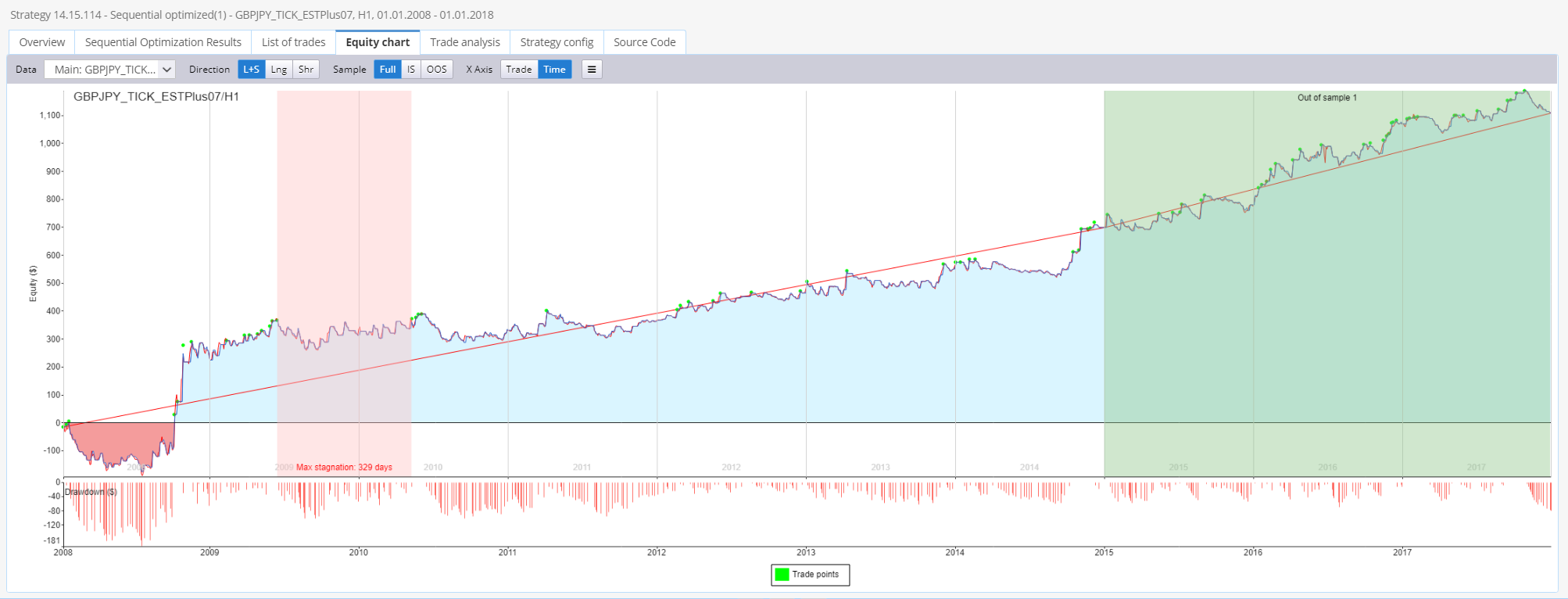

10.08.2021 15:12Please check out the following (Attached..)

I dont know what causing this issue......

Karish

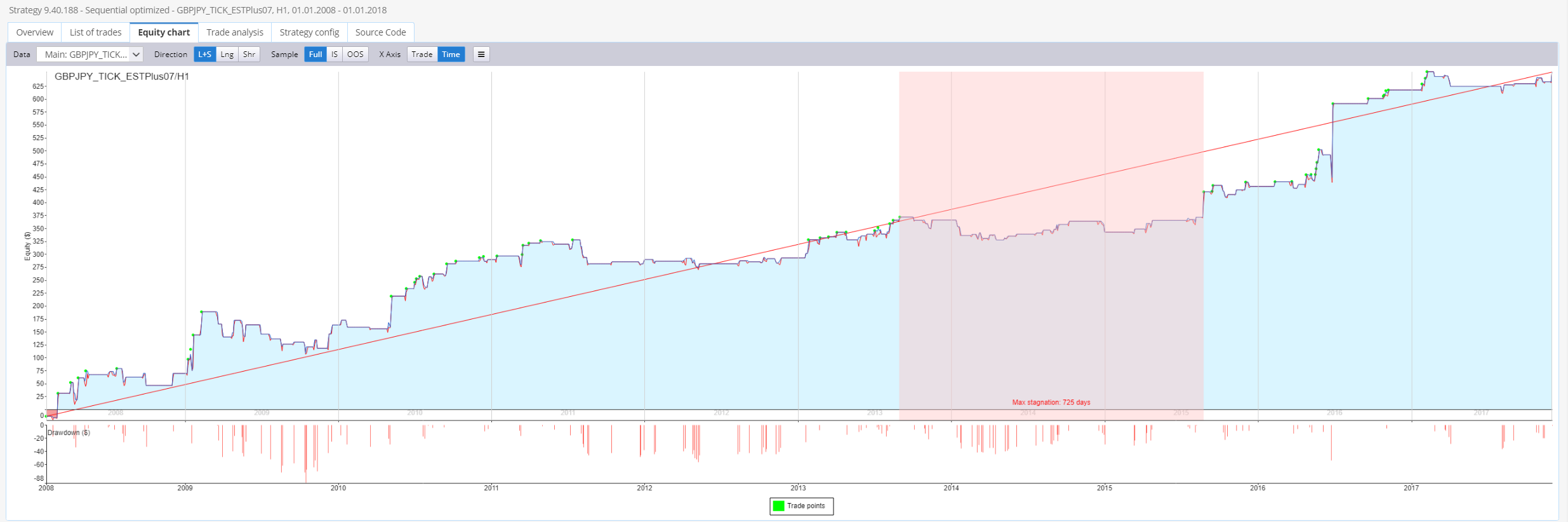

10.08.2021 16:24Attachment SeqOpt.png added

Attachment SeqOpt strategy after re-test.png added

Here is another example, Judge by the Name of the screenshots.

Why does it shows different results, what actually changed from taking a strategy that passed SeqOpt with new parameters, taking the same strategy with the same data, period, TF, and just re-test it, and waaaammm its just went all crazy wrong and different. What the hell..., i dont know what's going on behind the scenes there in SQX but something is deffently not right, Hence i cannot continue my project like that, because i just take that same strategy after SeqOpt and just perform a re-test, doing nothing more than that, and its all go crazy on me

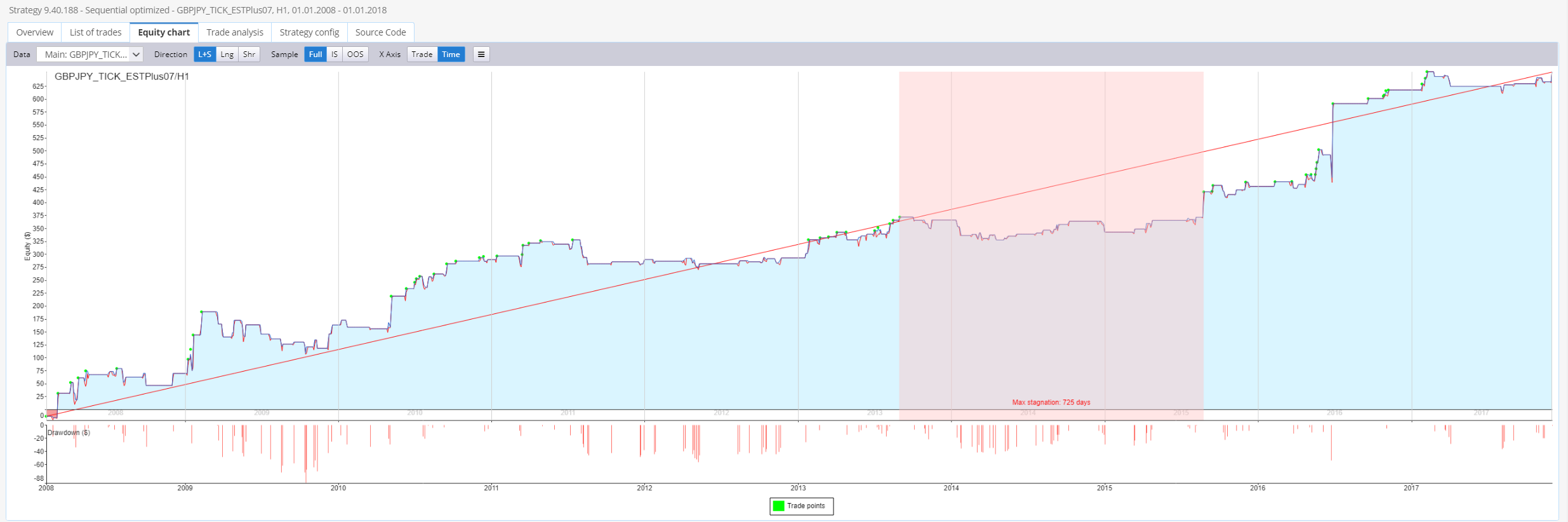

Karish

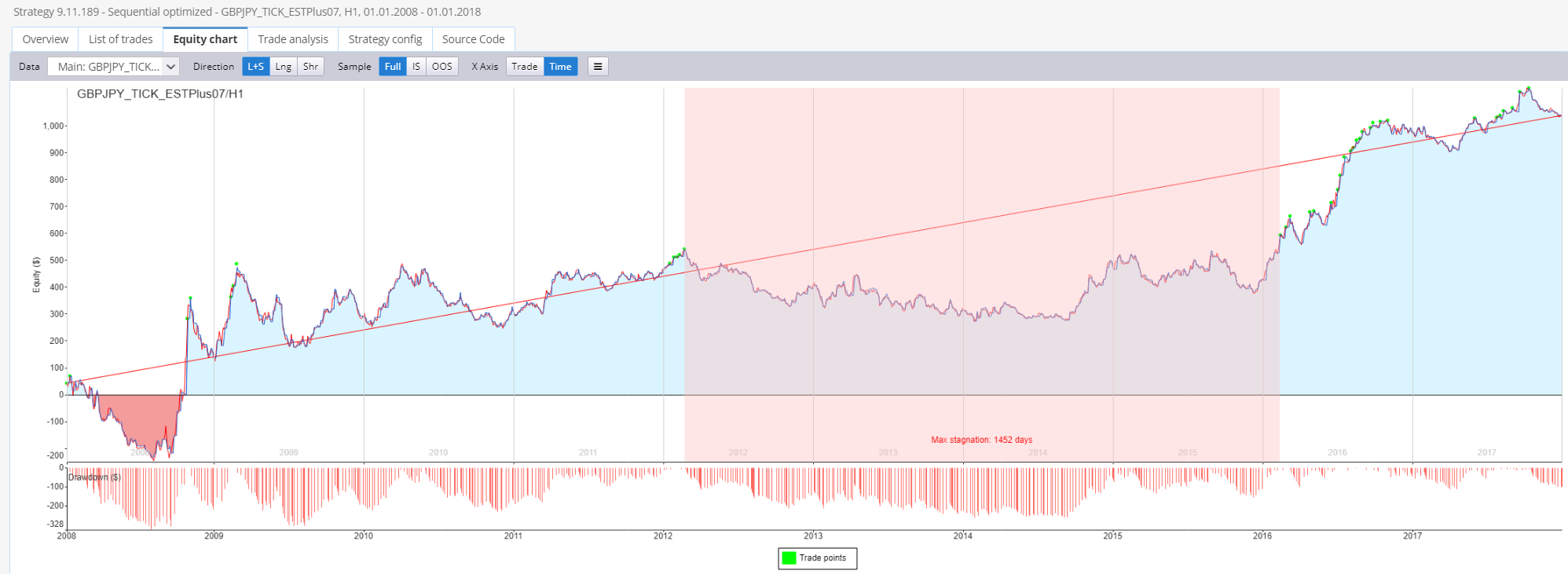

10.08.2021 16:37Attachment SeqOpt.png added

Attachment SeqOpt after retest.png added

Karish

10.08.2021 16:40

• Build

• Optimization Task (With SeqOpt)

Then i just use Automatic retest.

Mark Fric

11.08.2021 08:55Mark Fric

11.08.2021 11:25Status changed from In progress to Fixed

Essentially the sequential optimization was not worked as supposed, it always optimized one parameter against the original strategy, instead of progressively updating strategy parameters one by one after each optimization step.

Karish, thank you for pointing this out and for your persistence on the matter.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}