MT5 SQ Ticksize does not work correctly - PLEASE FIX!

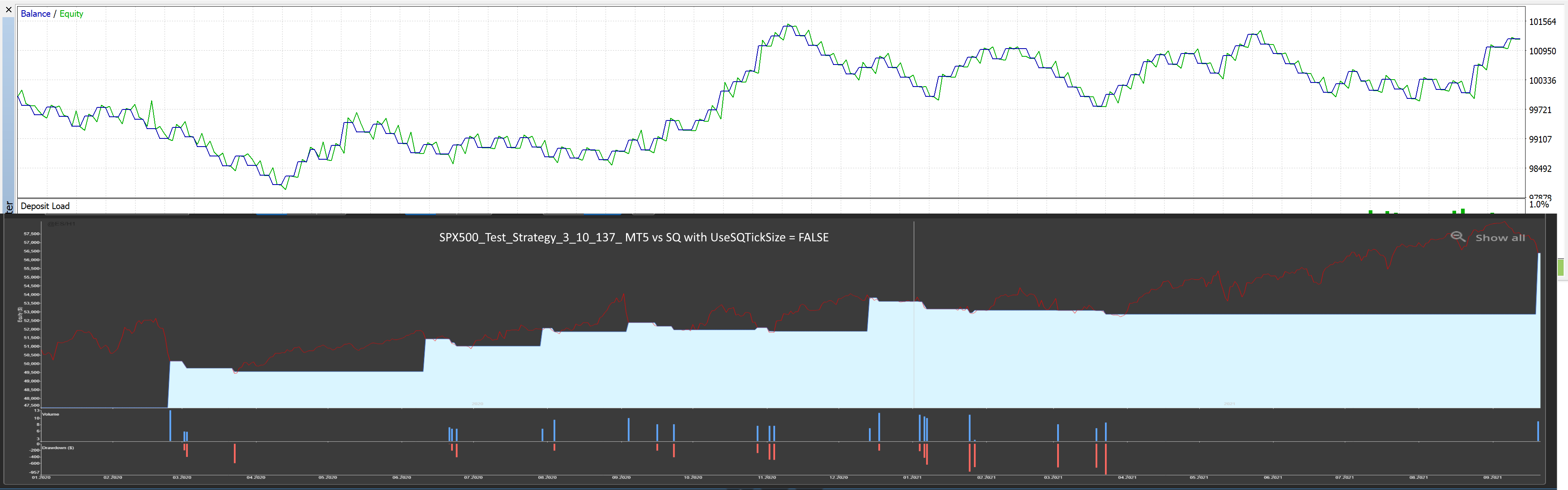

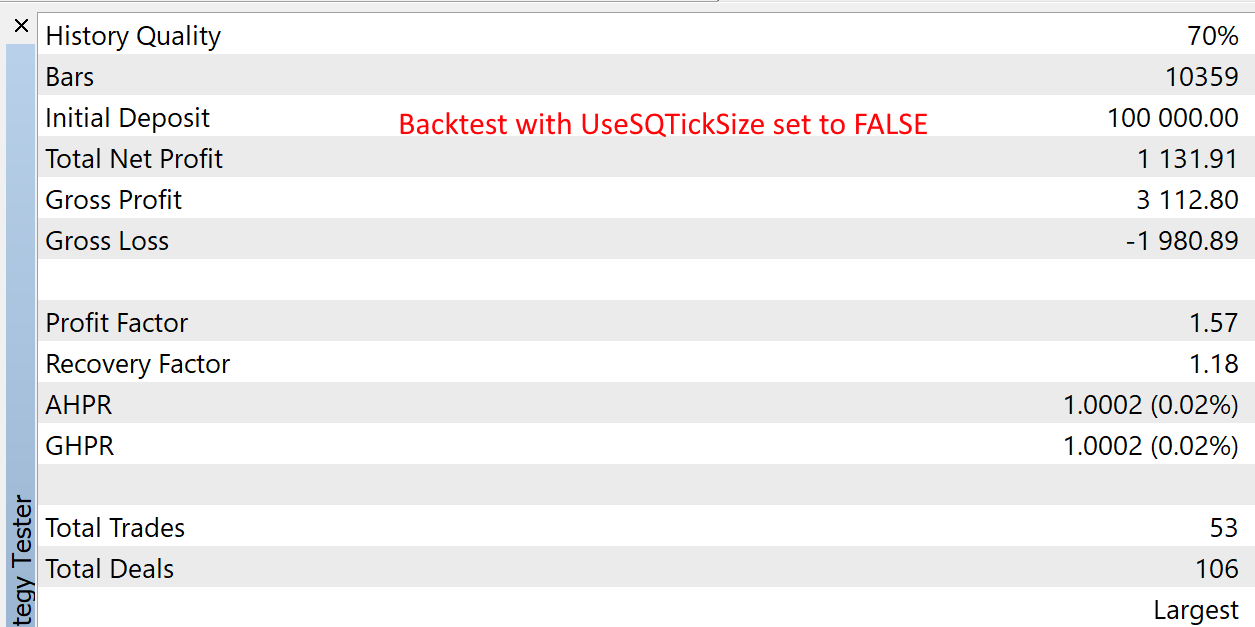

I'm CONSTANTLY running into issues with strategies not back testing correctly in MT5 for indices and it seems to relate to the SQ Ticksize setting.

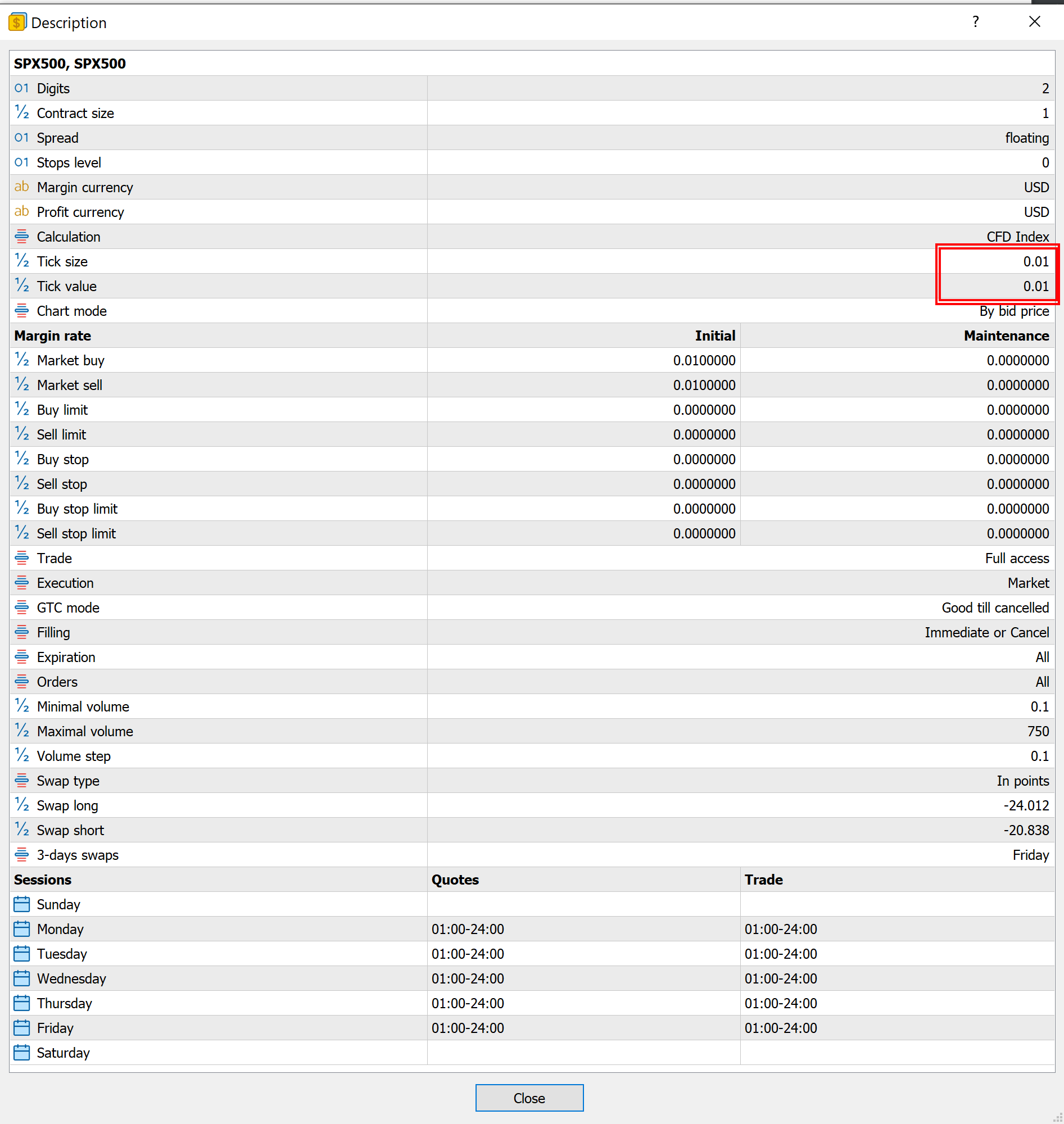

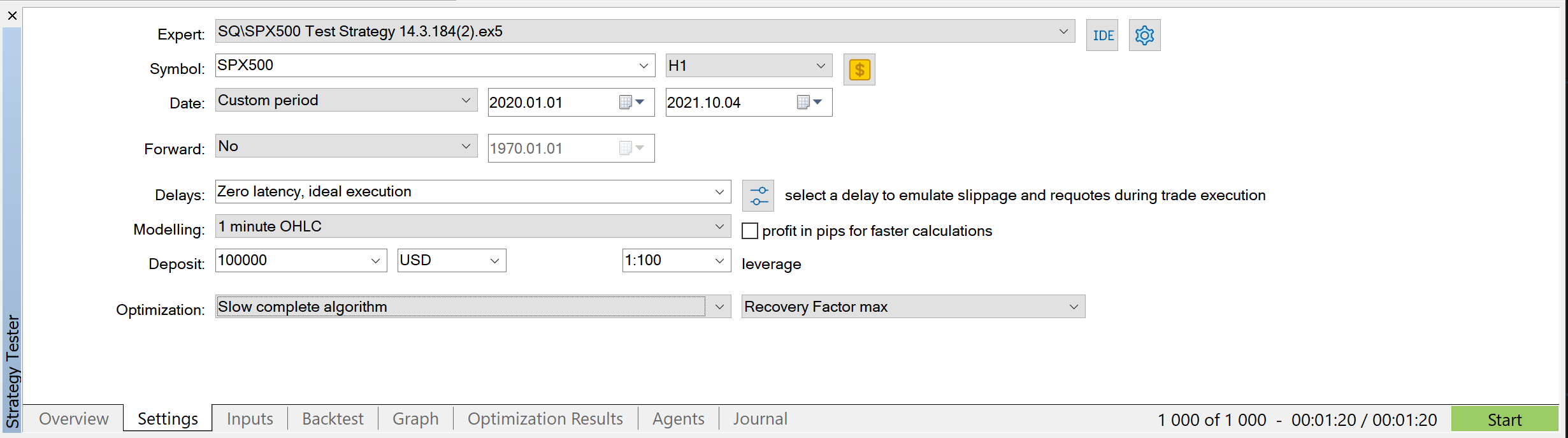

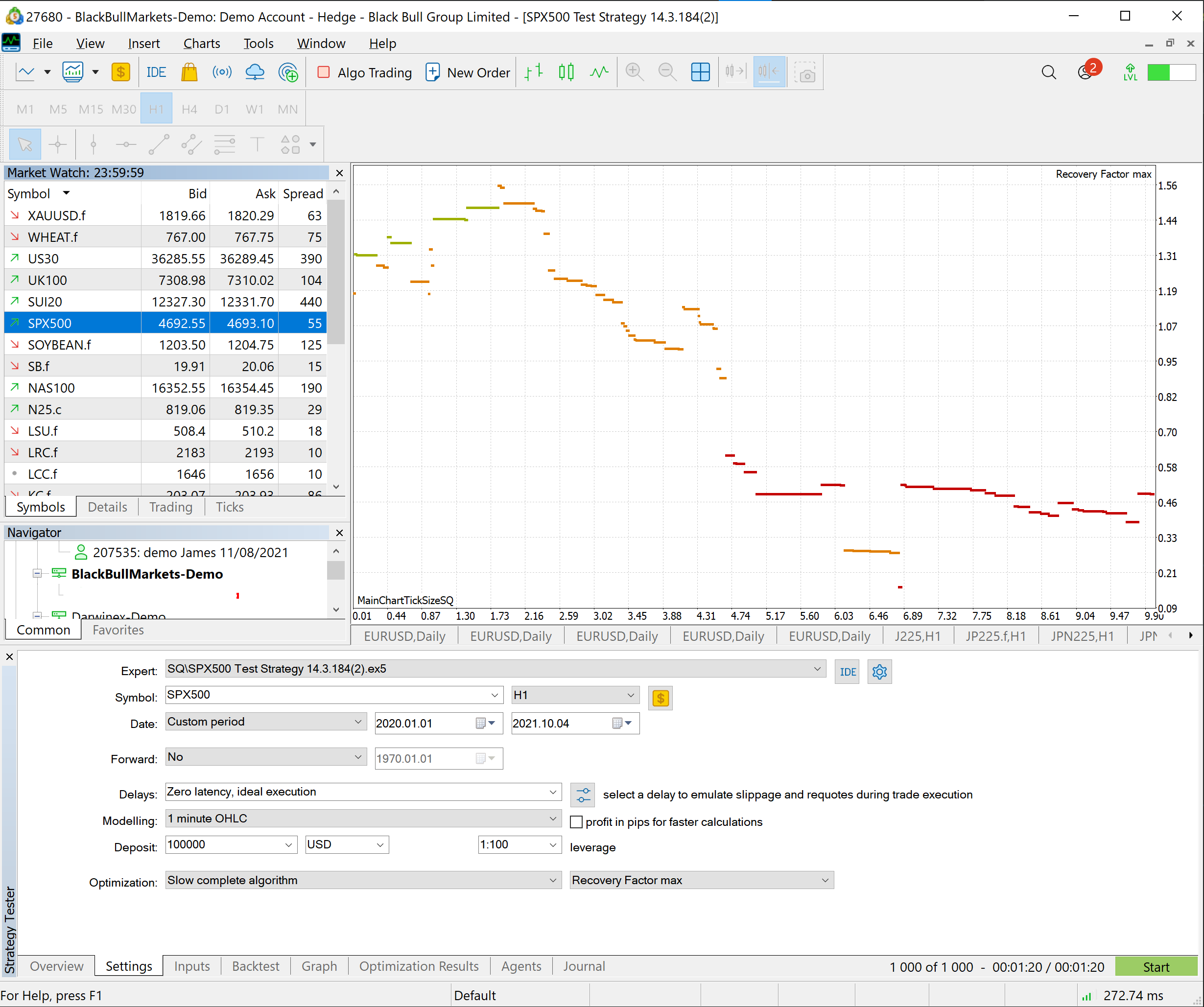

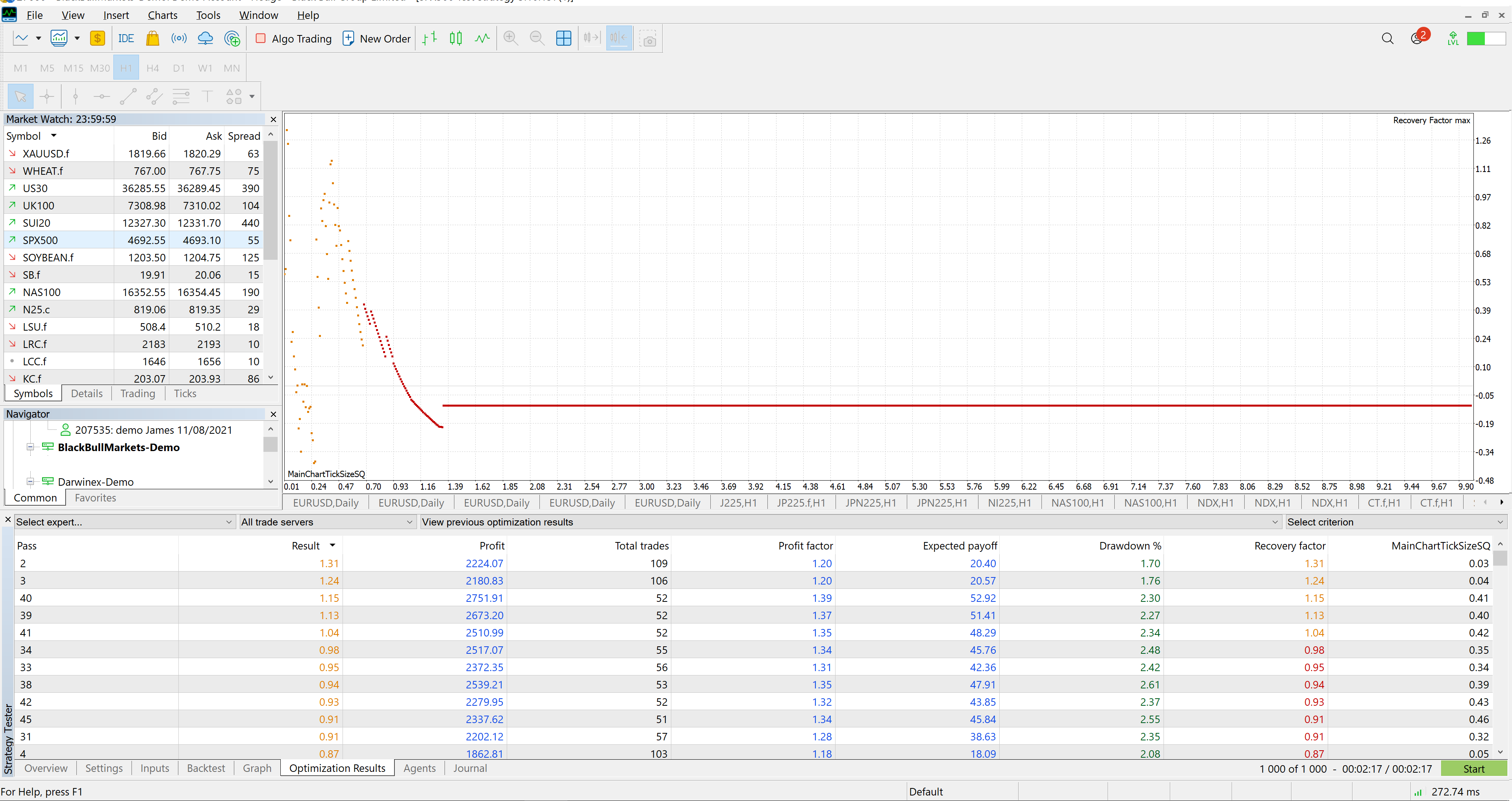

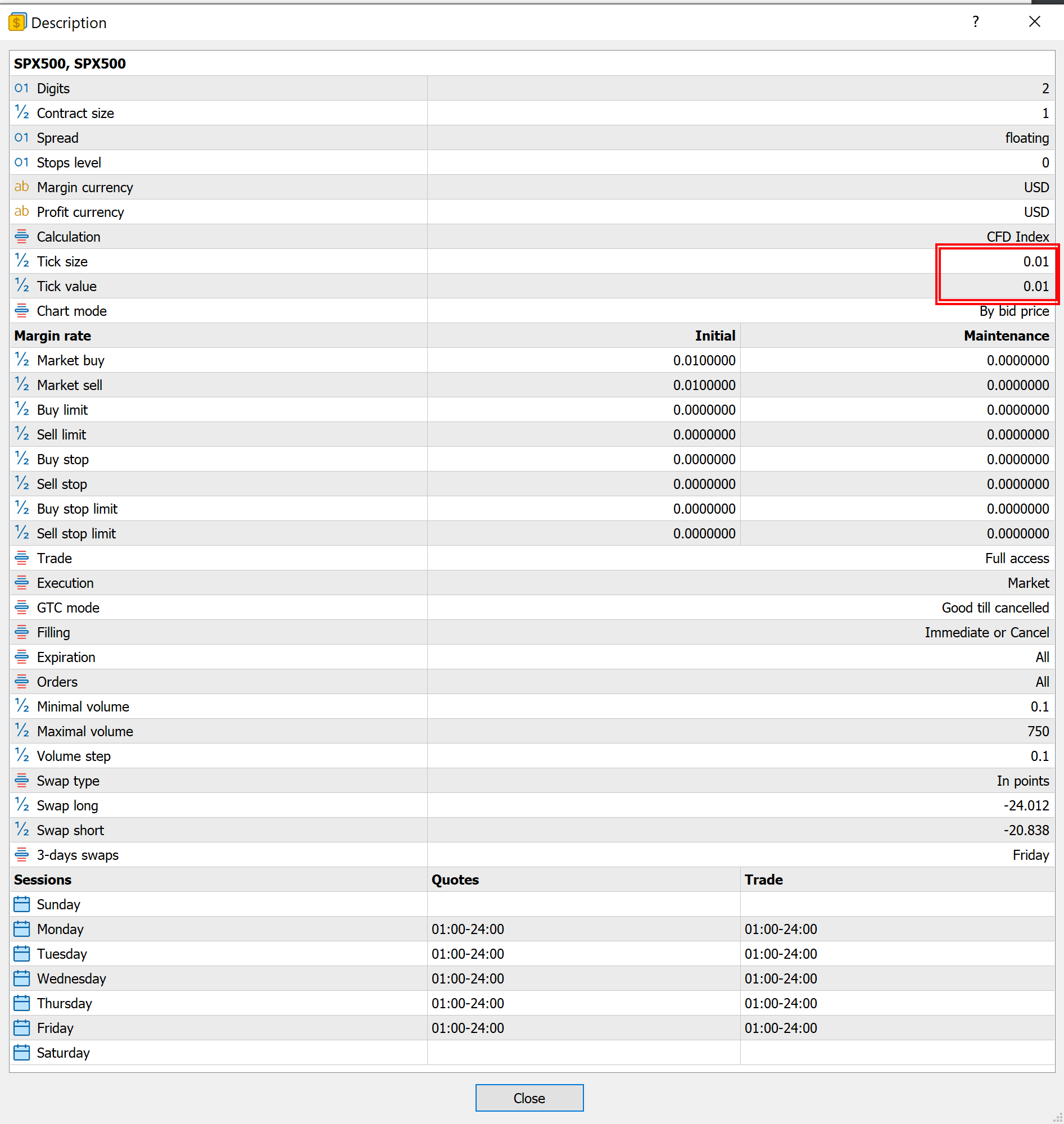

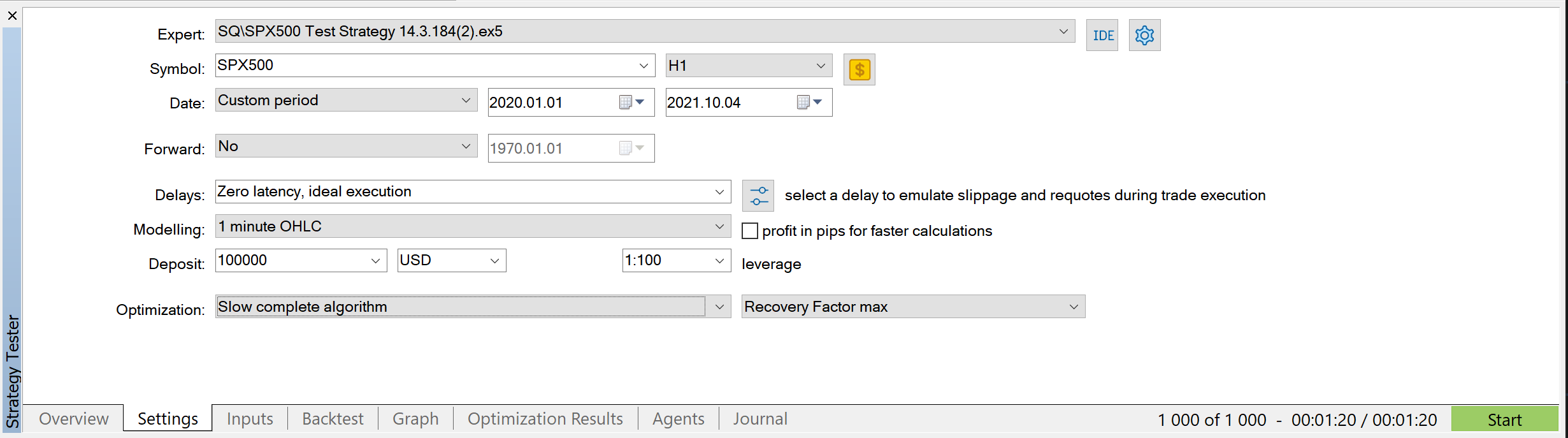

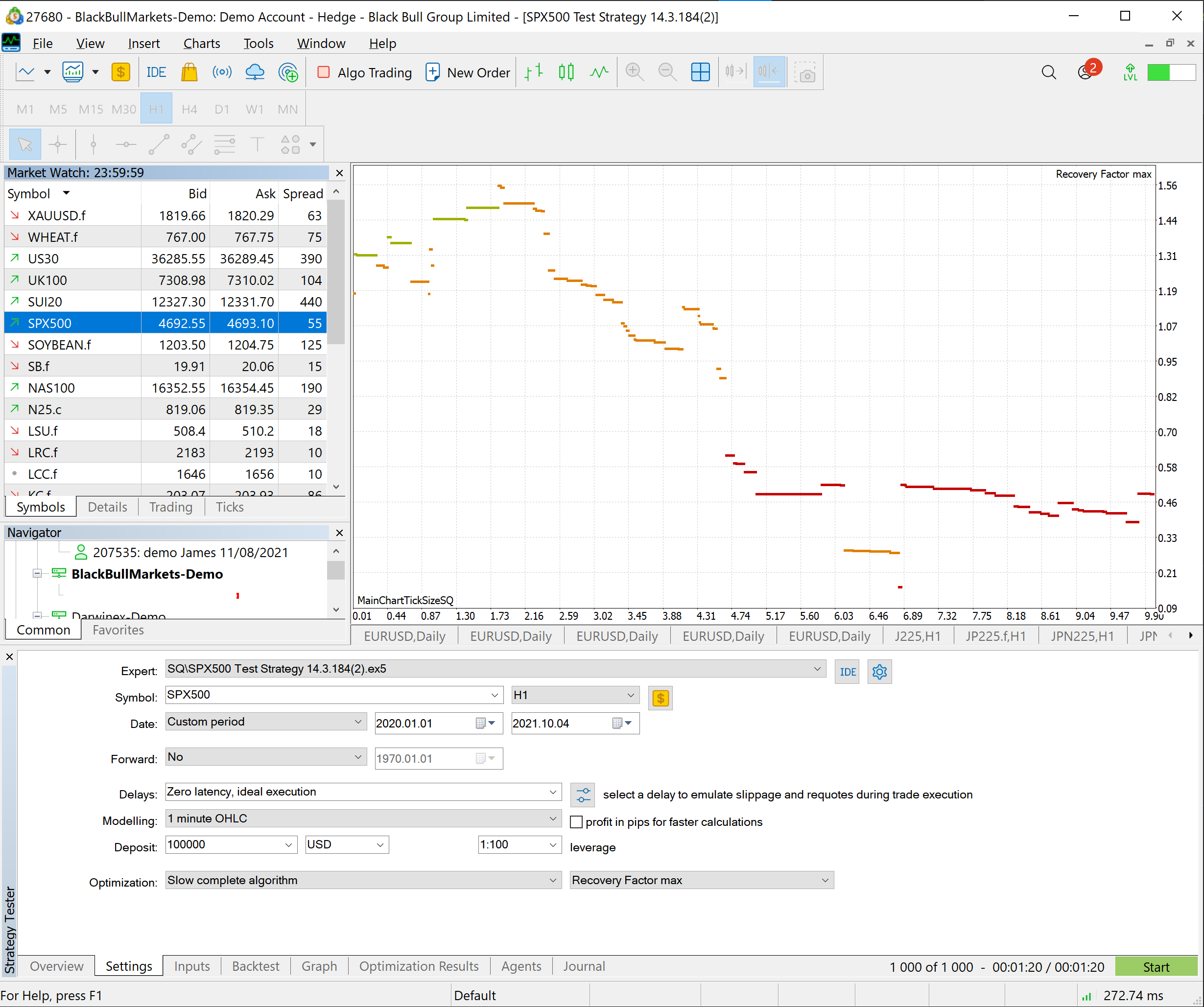

As you can see in the example image attached, the tick size under specification for SPX500 for Blackbull Markets Demo is 0.01, but as you can see from the optimization I ran with a range from 0.01 to 10 with a step of 0.01 (1000 tests) for the MainChartTickSizeSQ setting where UseSQTickSize = TRUE, I get results all over the place!!

What I would expect to see with the optimization is that "0.01" should be the ONLY correct answer where the strategy works properly and behaves similarly to backtests in SQ (I'm not expecting it to be 100% with different broker data, but for an H1 strategy it should be pretty close!)

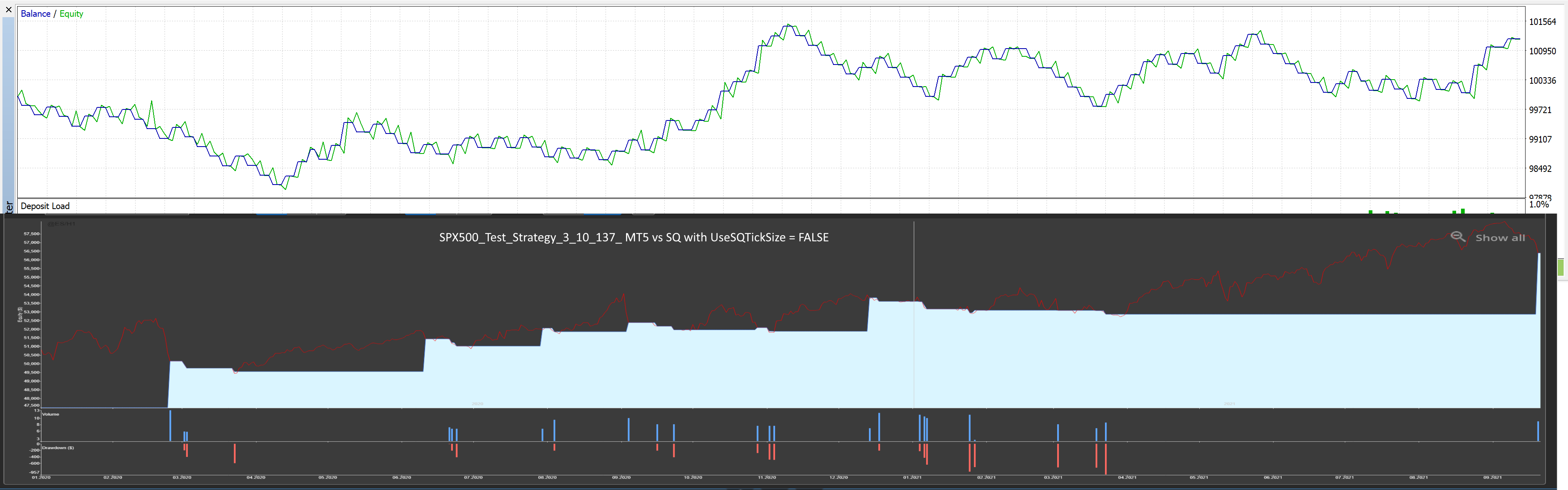

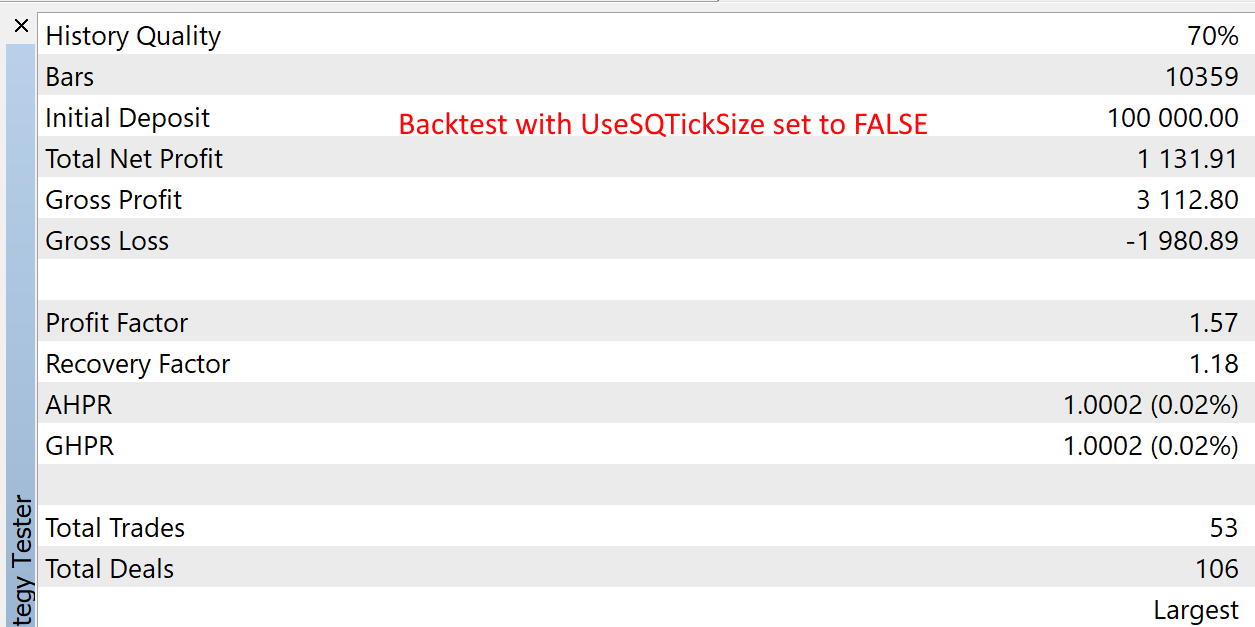

I've attached a second strategy that has even worse differences.

-

Votes +6

-

Project StrategyQuant X

-

Type Bug

-

Status Duplicate

-

Priority Normal

-

Assignee Lee Guan Chuan

-

Milestone Build 136 Dev 4

-

Category Backend

History

Tamas

09.09.2022 14:15Assignee changed from Lee Guan Chuan to Lee Guan Chuan

Status changed from New to Duplicate

Milestone changed from None to Build 136 Dev 4

Category changed from None to Backend

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}