Extend definition about risk per contract in MM method

This is a feature what I mentioned in the last coding session.

Development process in my custom project :

1. Develop robust strategies with fiexed one contract based on multiple markets, multiple time frames, multiple strategy types, multiple average # of bars.

2. Through manual selection or correlation test, the subset of alternative strategies in the potrfolio is selected.

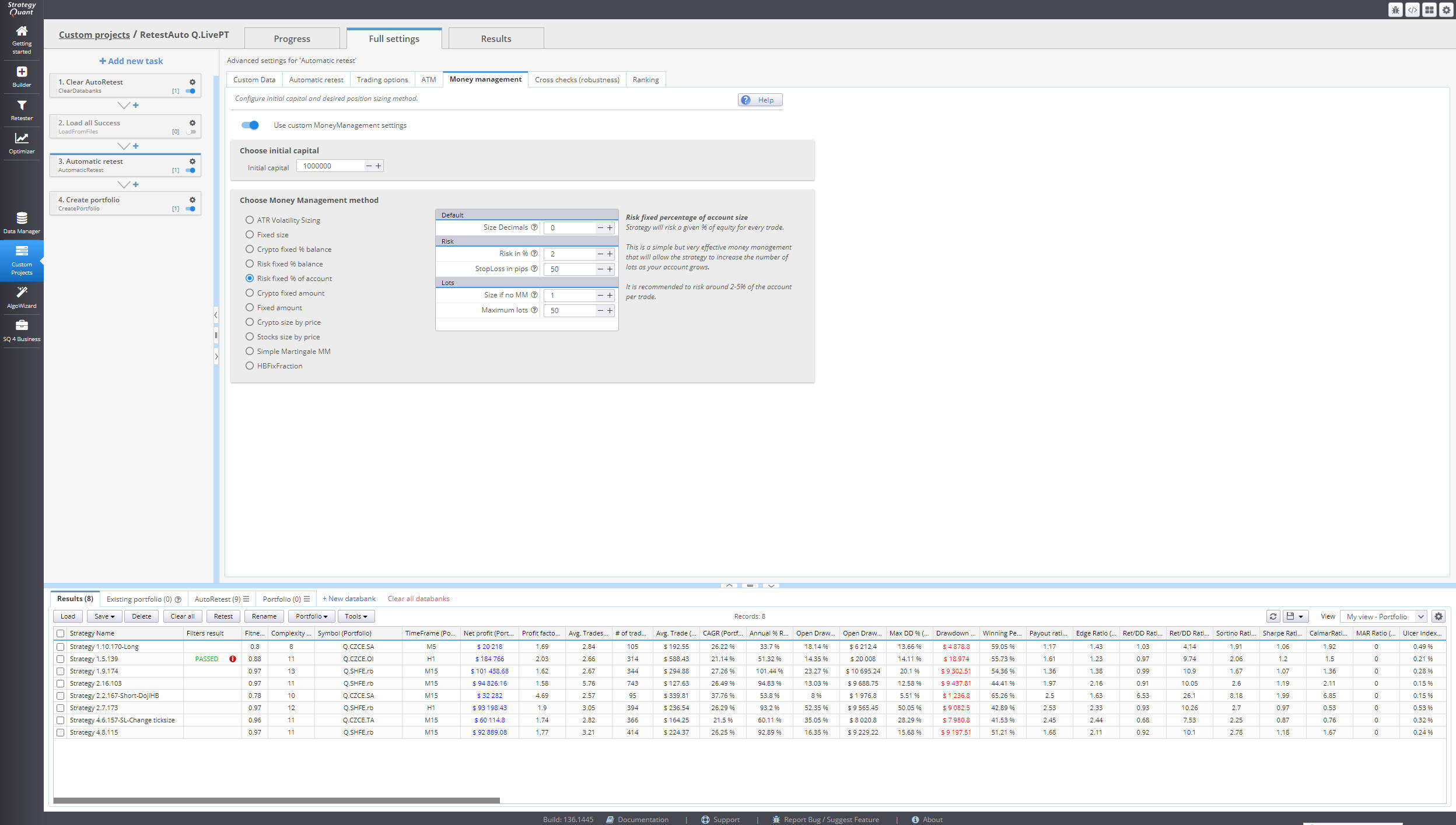

3. Use Automatic retest task, batch process to add money management backtest and Monte Carlo trade manipulation analysis for every individual strategy . Continuously adjust unified initial capital and MM method until it is in line with my risk control and profit requirement.

4. Merge portfolio through Createt portfolio task

In the Automatic retest task, SQ calculate risk per contract only according to built-in stoploss of strategy or mannual stoploss setting. Obviously, for 30 completely different kind of strategies, there are very different stoploss(maybe no built-in stoploss or based ATR), and Max history loss maybe lager than built-in stoploss. So I want to use a unified risk per contract which calculate based on order or strategy performance with fixed one contract. I don't want to set the risk per contract of every strategy one by one. So size of ervery strategy= percent/100*(initial capital+netprofit+openpositionProfit)/risk per contract of every strategy.

Then I want to try to expand the definition of risk per contrat. That can be such as Maximum historical loss , Maximum historical daily loss ,average of max 5 historic daily loss with fiexed one contract ,and so on. Note that the maximum historical daily loss must be calculated based on open profit/loss first. Sometimes i get this value from daily report of Multicharts. Could you please tell us the way to write these custom MM method. Or SQX directly builds in these money management method.

Why use unified MM method? Because for large portfolio, unity means simplicity.

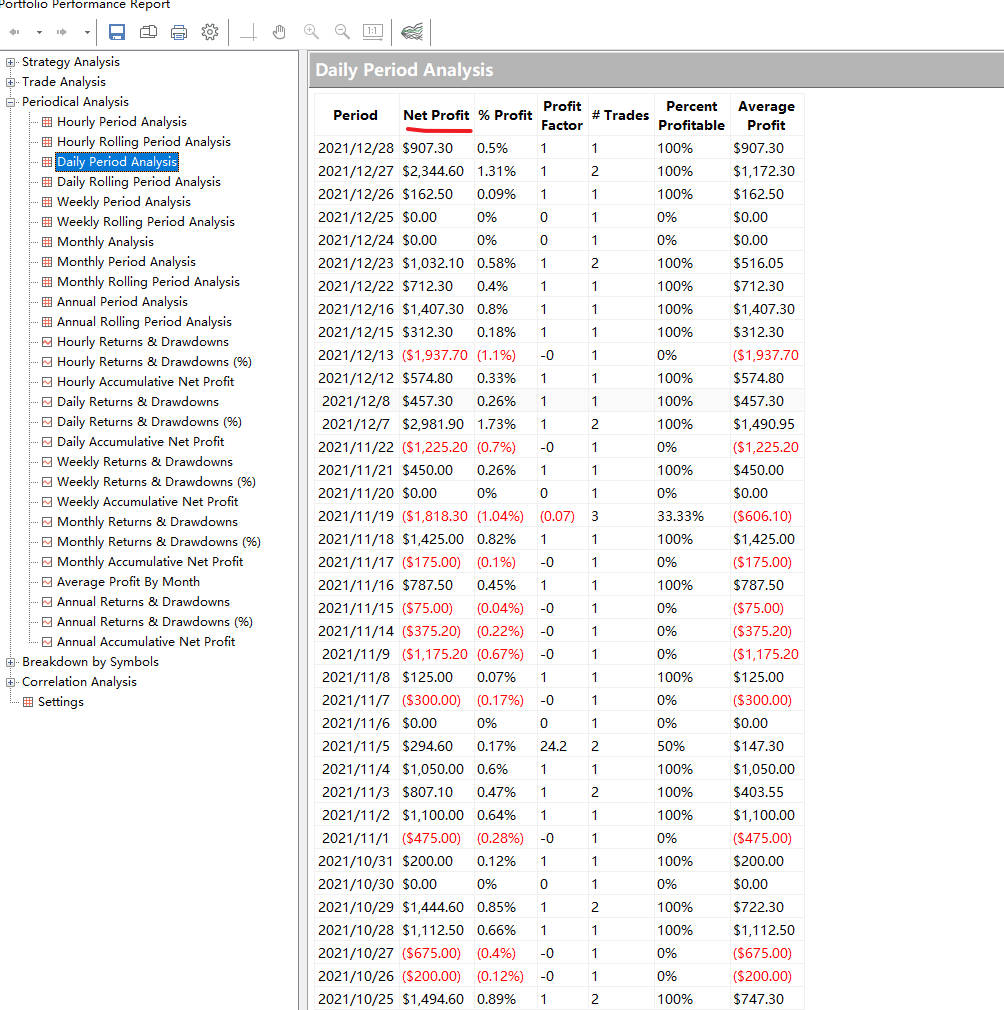

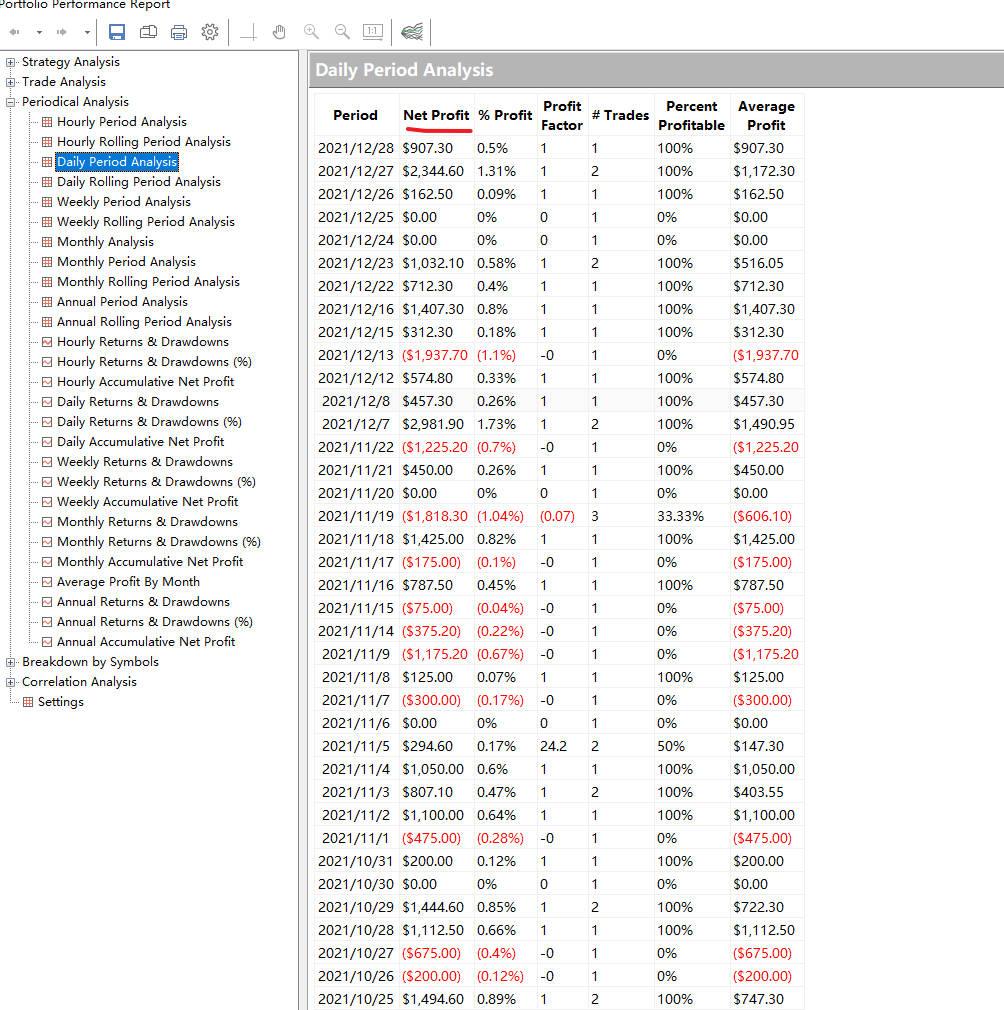

Why use max daily loss ? Because it contains more information about open positions than the max historic loss per trade. And the time-based definition about risk per contract is more standardized for the 30 strategies. Think about the portfolio of three strategies with 90pips, 250pips, 600pips of stoploss. If use stop loss as risk per contract,then create a portfolio. The psotion sizing of the three strategies after a long period of time will be very unbalanced.

By the way, this is not a portfolio approach to money management, this is simply batch money management for individual strategies. This means that each strategy gets an equal share of the money, the money available come from the profits of their own strategies, independent of other strategies. So it's not a team playing. And portfolio MM method is better than MM method in this task. Refer to the following two tasks.

-

Votes +5

-

Project StrategyQuant X

-

Type Feature

-

Status New

-

Priority Normal

History

Mark Fric

01.03.2023 14:11I still don't quite follow how you want to compute the size.

Could you perhaps make a simple example - just 2 strategies in portfolio, how you'd compute MM for them?

binhsir

05.03.2023 06:23

binhsir

05.03.2023 06:30I have sent email for a video and MM method tool with excel, please check it.

By the way, portfolio MM method is better than MM method in this task. referance :

binhsir

05.03.2023 06:32Description changed:

This is a feature what I mentioned in the last coding session.

Development process in my custom project :

1. Develop robust strategies with fiexed one contract based on multiple markets, multiple time frames, multiple strategy types, multiple average # of bars.

2. Through manual selection or correlation test, the subset of alternative strategies in the potrfolio is selected.

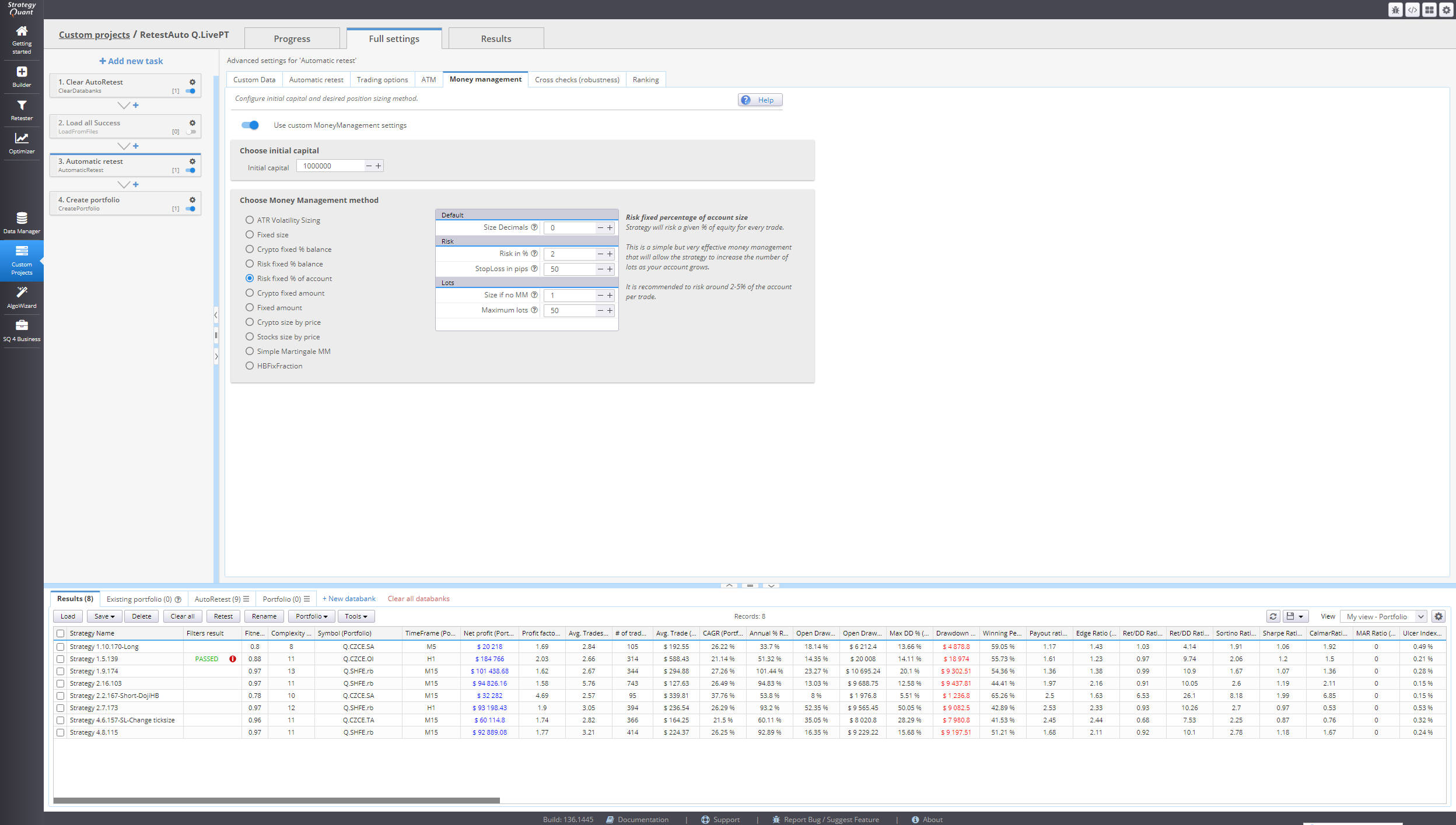

3. Use Automatic retest task, batch process to add money management backtest and Monte Carlo trade manipulation analysis for every individual strategy . Continuously adjust unified initial capital and MM method until it is in line with my risk control and profit requirement.

4. Merge portfolio through Createt portfolio task

In the Automatic retest task, SQ calculate risk per contract only according to built-in stoploss of strategy or mannual stoploss setting. Obviously, for 30 completely different kind of strategies, there are very different stoploss(maybe no built-in stoploss or based ATR), and Max history loss maybe lager than built-in stoploss. So I want to use a unified risk per contract which calculate based on order or strategy performance with fixed one contract. I don't want to set the risk per contract of every strategy one by one. So size of ervery strategy= percent/100*(initial capital+netprofit+openpositionProfit)/risk per contract of every strategy.

Then I want to try to expand the definition of risk per contrat. That can be such as Maximum historical loss , Maximum historical daily loss ,average of max 5 historic daily loss with fiexed one contract ,and so on. Note that the maximum historical daily loss must be calculated based on open profit/loss first. Sometimes i get this value from daily report of Multicharts. Could you please tell us the way to write these custom MM method. Or SQX directly builds in these money management method.

Why use unified MM method? Because for large portfolio, unity means simplicity.

Why use max daily loss ? Because it contains more information about open positions than the max historic loss per trade. And the time-based definition about risk per contract is more standardized for the 30 strategies. Think about the portfolio of three strategies with 90pips, 250pips, 600pips of stoploss. If use stop loss as risk per contract,then create a portfolio. The psotion sizing of the three strategies after a long period of time will be very unbalanced.

By the way, this is not a portfolio approach to money management, this is simply batch money management for individual strategies. This means that each strategy gets an equal share of the money, the money available come from the profits of their own strategies, independent of other strategies. So it's not a team playing. And portfolio MM method is better than MM method in this task. Refer to the following two tasks.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}

https://roadmap.strategyquant.com/tasks/sq4_9988

https://roadmap.strategyquant.com/tasks/sq4_9924