Swap coasts

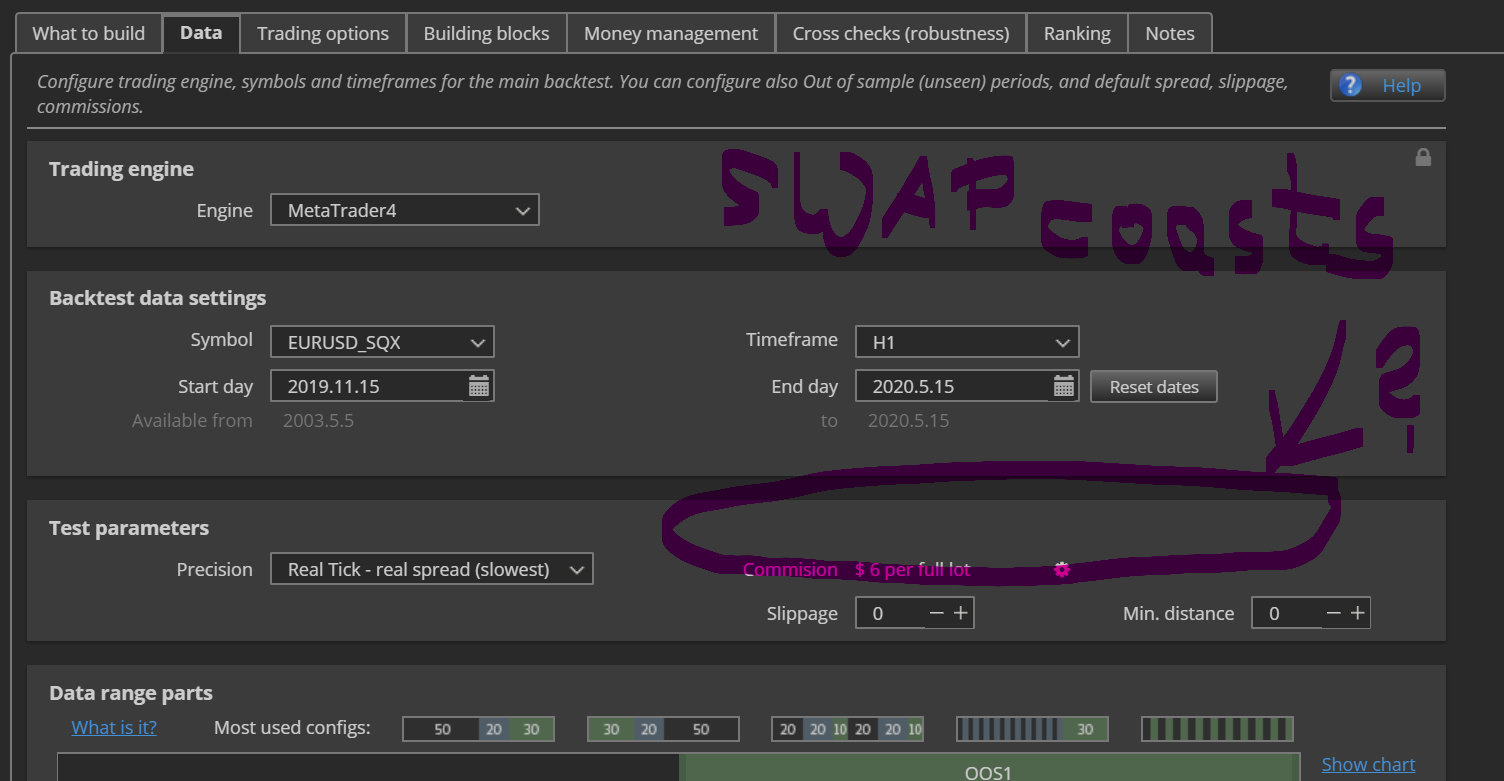

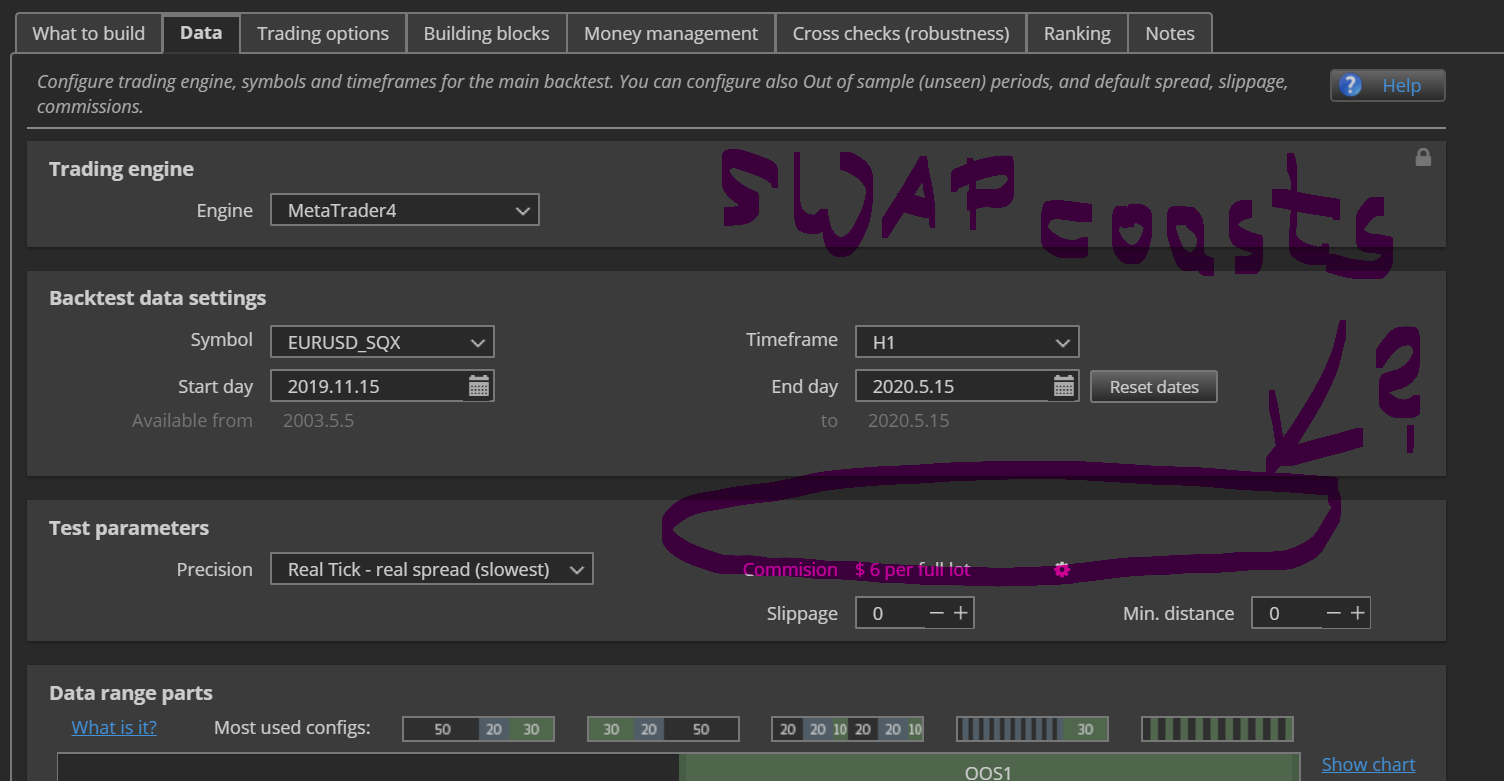

Would it be possible to take the daily SWAP coasts into account as additional trading costs in the calculations? Similar to the commissions as $ per LOT which are deducted from profit at the change of the day. This can be very important for many strategies and can very much determine the real success of a strategy. In the example, 1.1 shows profit, but in reality it is not. This contrasts with about $ 1.8 - $ 2 swap coasts and thus the profit is actually a loss. However, this is significant with many strategies found and their assessment as really profitable or not. When calculating and evaluating scalping strategies, this is a disaster and leads to total loss in real trading. Can you maybe add something like that? Maybe at the point in the settings where the coasts commissions are set? Please see my attachments.

-

Votes +4

-

Project Extending SQ

-

Type Feature

-

Status New

-

Priority Normal

History

SuperWutsch

17.05.2020 15:18hankeys

18.05.2020 08:50SuperWutsch

20.05.2020 20:25Attachment ME_SWAPS long and short formulas.mq4 added

Attachment SQX ME_Model 125 SWAP Idea.png added

The BrokerServerTime is generally determined by the format recorded in the DataManager when the tick data is downloaded. (GMT / DST)

The time when each broker calculates his swaps can be requested from the broker or read on his website. You can also display the SWAP rates for each symbol on the website of each broker. There you can also see whether the broker specifies the swaps in points or in currency. This makes it easy to fix the settings.

I use € as the account currency so my formulas convert the swaps into €. They may not be perfect and I am not a good coder, but in principle they work. I have attached these to you for a better understanding, which may also help. You can do that better than me, but it is my idea to maybe realize it or at least to take a path in the right direction.

in the appendix calculate my formulas for swap and calculate in my € currency for you for information.

Attention: in my formulas the functions for "..Total_Buy_Size" and so on, but you see what I mean and you can code this self

But please see my picture in attached I have designed there my ideas as best as I can in your SQX background. So you mean easy what I mean.

bentra

08.11.2020 02:57© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}