ATR based position sizing

Can you please add ATR based position sizing for money management?

Attachments

-

Votes +3

-

Project Extending SQ

-

Type Feature

-

Status New

-

Priority Normal

History

b

b

bentra

13.11.2020 09:30

Like a secondary option instead of using SL. such as:

Instead of risk % of equity per trade (per SL), it could be risk % of equity per ATR.

or

Instead of risk $100 per trade (per SL), we could choose to risk $100 per ATR.

This works nicely if we peg the ATR to ~10 Daily bar ATR. Holds steady but fluctuates a little. This way we have position sizing rule that is steady (so we do not curve fit to the larger position winning trade iterations when there is a volatile SL or exit rules) but yet is still volatility based and can be blanketed across multiple markets.

Instead of risk % of equity per trade (per SL), it could be risk % of equity per ATR.

or

Instead of risk $100 per trade (per SL), we could choose to risk $100 per ATR.

This works nicely if we peg the ATR to ~10 Daily bar ATR. Holds steady but fluctuates a little. This way we have position sizing rule that is steady (so we do not curve fit to the larger position winning trade iterations when there is a volatile SL or exit rules) but yet is still volatility based and can be blanketed across multiple markets.

m

t

tnickel

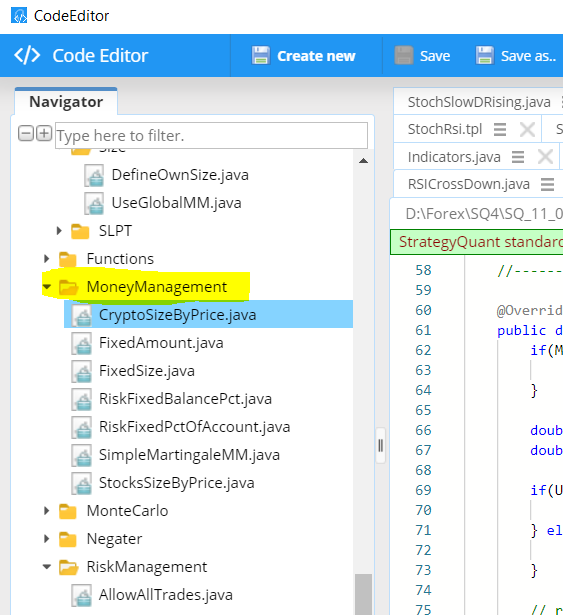

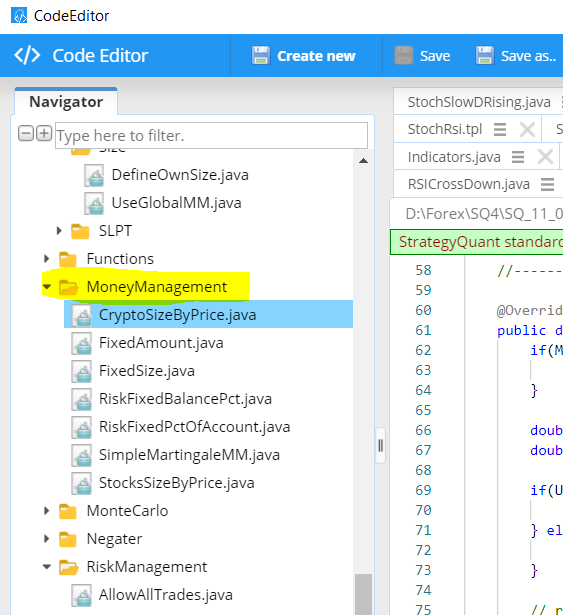

13.11.2020 09:30Attachment description moneymanagement.png added

Attachment money management expandable in code.png added

Make it sense to make the position sizing more flexible? the SQ can search for a formular for position sizing?

But more flexibility make more curvefitting.

About position sizing there is many in the web.

https://www.quantshare.com/sa-411-5-position-sizing-techniques-you-can-use-in-your-trading-system

I think the moneymanagement in SQ is expandable

At the moment there is no more explanation for this in the documentation.

We need a documentation for this. Better an example.

t

e

E

Votes: +3

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}

{kind=link}