SQ should support portfolio MM method

Background thinking:Position sizing is divided into time vertical management and horizontal multi-strategy management. Some experts believe that the position size should not change quickly over time. But for a very large portfolio (which is trading edge), horizontal money allocation for every strategy is especially important. Margin requirements, stop losses, max history loss, max history daily losses, average # of bars in trade, dollar volatility vary tremendously for each strategy. In any given time period of live trading, we should minimize the probability that a loss in a few individual strategy will result in a large loss for the entire portfolio, and this is where horizontal money management can come into play. And i think portfolio MM method feature is more important and higher priority in the futures market than in the foreign exchange market, more important in emerging countries futures market than USA futures market. Because there are large different insturments specs and volatility in emerging futures market.

.

Disadvantages of using SQX plus QA4 currently for portfolio MM method:

1. There are portfolio, MM method, Monte Carlo trade manipulation analysis module in QA4, but they work independently of each other.

2. The development time of the strategies in the portfolio is different. We usually need to add the latest sample data and carry out the test of the portfolio. But QA4 calculation is based on the order result of original strategy.

3. The correlation coefficient in the portfolio is dynamic. We need to recalculate the correlation in the portfolio periodically.

4. Every time we adjust MM method or parameters. We must first test and save the new strategy file in SQX , then importing it to QA4 for new simulation. The process is quite tedious.

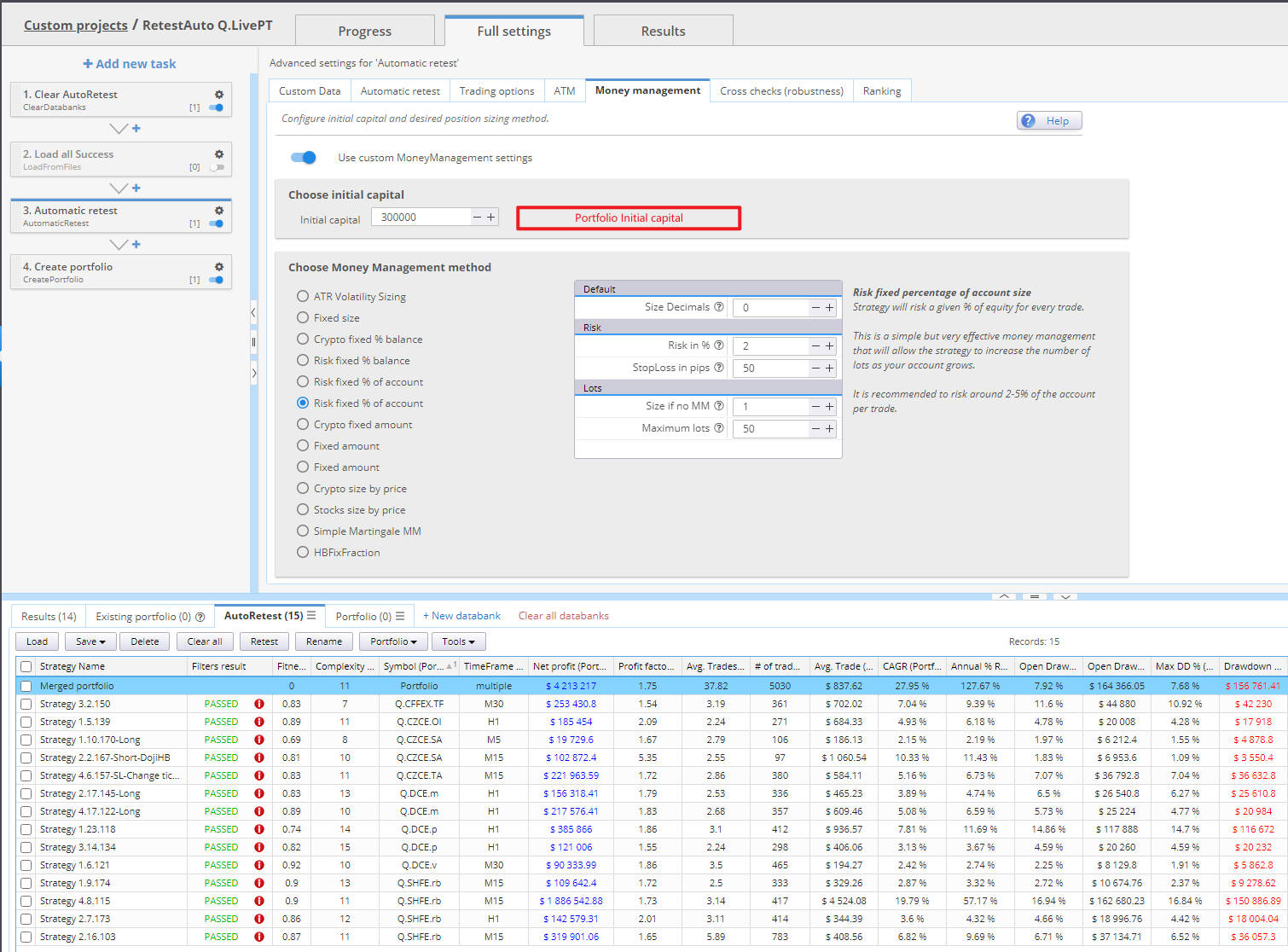

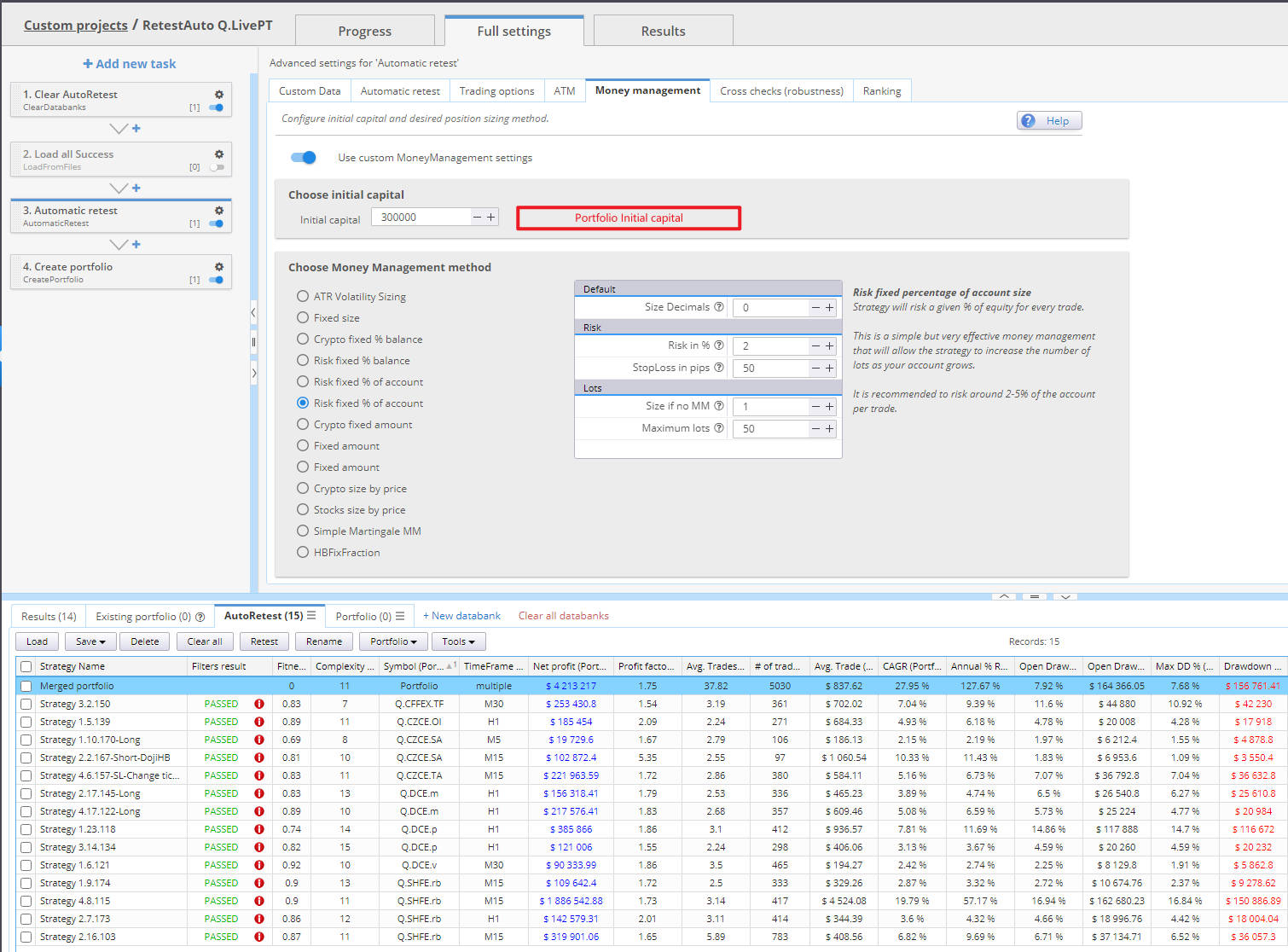

As you can see in the Automatic retest task of my custom project, money management calculations obviously are made for individual strategies. Intial capital in SQ is available capital for each individual strategy.

For the entire portfolio,we may risk overexposure on the individual strategies. For example, when we have a really performing strategy and it makes money, it keeps it to itself and increases its risk portion on the next trade. If we use new formula : size of every strategy = percent/100*(initial capital of portfolio+portfolio_netprofit+Portfolio_openpositionprofit)/risk per contract of every strategy. In addition to being more manageable, this is the method that

stays very true to the teamwork philosophy of portfolio management. This portfolio MM approach is different from sq4_9987.

It is highly recommended to add new portfolio money management in Create portfolio task and works with the task of Automatic retest together. Or It'a better to redesign a new portfolio management module in SQX.

1. Re-batch backtest the portfolio developed in the early stage after adding new sample data.

2. Re-batch backtest the portfolio after add portfolio MM method

3. Re-batch backtest the portfolio after add portfolio MM method and Monte Carlo trade manipulation analysis at the same

4. support unified MM method, automatic and batch calculate risk per contract of individual strategy, support more option of risk per contract. Such as more standardized risk: Max historic daily loss based on open profit/loss.

I usually use this method for backtesting. And the original strategy code with fixed n contract were deployed in live trading. Then modify the contract parameters on a weekly and monthly basis by mannual calculation. It is easy job, but somebody may use strategy code with portfolio MM method in Portfolio traders of Multicharts.

By the way, the two related tasks are as follows:

https://roadmap.strategyquant.com/tasks/sq4_9987

https://roadmap.strategyquant.com/tasks/sq4_9924

Once again, I sincerely ask the sq development team to seriously consider portfolio feature. This will help to better manage the risks and profit of our large portfolio. All forex and futures traders will benefit a lot. Thanks very much.

-

Votes +6

-

Project StrategyQuant X

-

Type Feature

-

Status New

-

Priority Normal

History

binhsir

28.02.2023 03:21Description changed:

Background thinking:Position sizing is divided into time vertical management and horizontal multi-strategy management. Some experts believe that the position size should not change quickly over time. But for a very large portfolio (which is trading edge), horizontal money allocation for every strategy is especially important. Margin requirements, stop losses, max history loss, max history daily losses, average # of bars in trade, dollar volatility vary tremendously for each strategy. In any given time period of live trading, we should minimize the probability that a loss in a few individual strategy will result in a large loss for the entire portfolio, and this is where horizontal money management can come into play. And i think portfolio MM method feature is more important and higher priority in the futures market than in the foreign exchange market, more important in emerging countries futures market than USA futures market. Because there are large different insturments specs and volatility in emerging futures market.

.

Disadvantages of using SQX plus QA4 currently for portfolio MM method:

1. There are portfolio, MM method, Monte Carlo trade manipulation analysis module in QA4, but they work independently of each other.

2. The development time of the strategies in the portfolio is different. We usually need to add the latest sample data and carry out the test of the portfolio. But QA4 calculation is based on the order result of original strategy.

3. The correlation coefficient in the portfolio is dynamic. We need to recalculate the correlation in the portfolio periodically.

4. Every time we adjust MM method or parameters. We must first test and save the new strategy file in SQX , then importing it to QA4 for new simulation. The process is quite tedious.

As you can see in the Automatic retest task of my custom project, money management calculations obviously are made for individual strategies. Intial capital in SQ is available capital for each individual strategy.

For the entire portfolio,we may risk overexposure on the individual strategies. For example, when we have a really performing strategy and it makes money, it keeps it to itself and increases its risk portion on the next trade. If we use new formula : size of every strategy = percent/100*(initial capital of portfolio+portfolio_netprofit+Portfolio_openpositionprofit)/risk per contract of every strategy. In addition to being more manageable, this is the method that

stays very true to the teamwork philosophy of portfolio management. This portfolio MM approach is different from sq4_9987.

It is highly recommended to add new portfolio money management in Create portfolio task and works with the task of Automatic retest together. Or It'a better to redesign a new portfolio management module in SQX.

1. Re-batch backtest the portfolio developed in the early stage after adding new sample data.

2. Re-batch backtest the portfolio after add portfolio MM method

3. Re-batch backtest the portfolio after add portfolio MM method and Monte Carlo trade manipulation analysis at the same

4. support unified MM method, automatic and batch calculate risk per contract of individual strategy, support more option of risk per contract. Such as more standardized risk: Max historic daily loss based on open profit/loss.

I usually use this method for backtesting. And the original strategy code with fixed n contract were deployed in live trading. Then modify the contract parameters on a weekly and monthly basis by mannual calculation. It is easy job, but somebody may use strategy code with portfolio MM method in Portfolio traders of Multicharts.

By the way, the two related tasks are as follows:

https://roadmap.strategyquant.com/tasks/sq4_9987

https://roadmap.strategyquant.com/tasks/sq4_9924

Once again, I sincerely ask the sq development team to seriously consider portfolio feature. This will help to better manage the risks and profit of our large portfolio. All forex and futures traders will benefit a lot. Thanks very much.

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}