b130 dev2 - randomize history data

in dev2 was made some changes, but how could this be right?

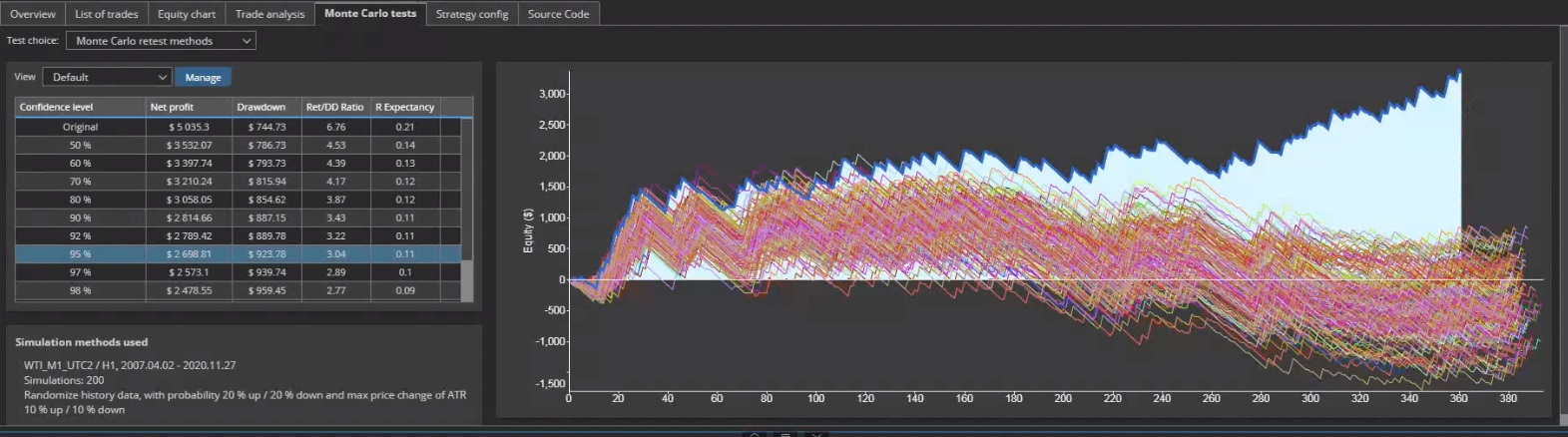

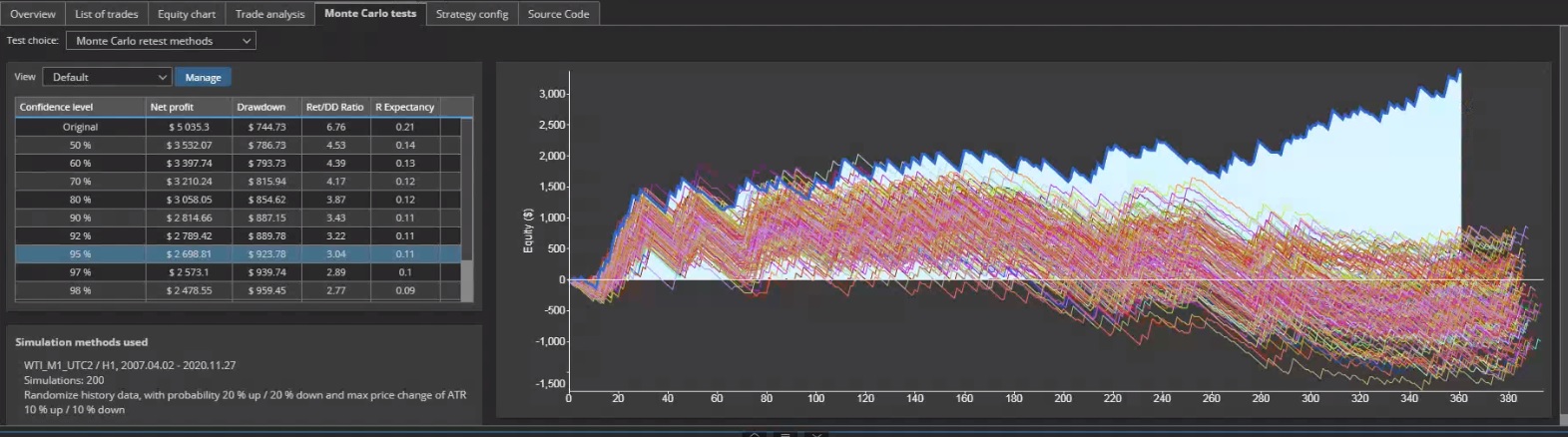

what exatly does this MC test doing, because by randomize params i imagine, that HIGH and LOW of the candles are shifted up or down in some probability and with some amount of pips

so the results should be different EQ curves, because the candle for every MC run should be different...but they are not

with original settings 20/10/20/10 from 216 strats everyone is passed

here is used 50/50/50/50

i really dont understand what we are seeing in this test...

-

Votes +4

-

Project StrategyQuant X

-

Type Bug

-

Status Refused

-

Priority Normal

History

hankeys

29.11.2020 19:08bentra

29.11.2020 19:30As Marc says this code is exposed.

public void modifyData(IRandomGenerator rng, TickEvent tickEvent, double globalATR) { double dblProbability = ((double) Probability/ 100.0d); if(rng.probability(dblProbability)) { // we should change this price double ask = tickEvent.getAsk(); double bid = tickEvent.getBid(); double spread = ask - bid; int change; if(relativeMaxChange <= 0) { change = rng.nextInt(MaxChange); } else { change = rng.nextInt(relativeMaxChange); } double dblChange = ((double) change)/ 100.0d; double priceChange = 2 * globalATR * dblChange; bid = (rng.nextInt(2) == 0 ? bid + priceChange : bid - priceChange); tickEvent.setBid(bid); tickEvent.setAsk(bid + spread); } }

something like:

On each tick

-Get bid and ask of original data

-Change bid randomly +/- based on % of a long term ATR.

-ask is now same as bid plus the spread

-return the new bid and ask for the rest of the functions.

This will create violent choppy ticks and increase volatility especially with numbers as high as 50% of ATR.

Bias for limit orders combined with tight TP and far away SL.

Bias against stop order entries and tight SL.

The code is exposed so we can change the algo.

Mark Fric

01.12.2020 13:26Status changed from In progress to Refused

When you change the data in MC tests the performance becomes much worse.

bentra

05.12.2020 02:06https://roadmap.strategyquant.com/tasks/sq4_7233

https://strategyquant.com/forum/topic/possible-new-way-to-randomize-data-with-change-instead-of-atr/

© Copyright. All rights reserved. ProjectPanel.com

{kind=link}